That was the Minister of Finance’s chief press secretary responding on behalf of the Minister to an inquiry from Stuff journalists shortly after Neil Quigley’s ill-starred press conference late on the afternoon of 5 March, the day Adrian Orr’s resignation was announced. But I’ll come back to that.

The main problem for the Minister of Finance, in finally encouraging Neil Quigley to resign late last Friday afternoon, is that throwing him to the wolves (well overdue) left her exposed to the long-running questions about what she knew and when, and what part she had played – actively or passively – in the choice to deliberately mislead New Zealanders about what had gone on around the out-of-the-blue no-notice resignation of one of the most powerful unelected officials in New Zealand, one who had generated enormous controversy in his time and whose frosty relationship with Willis, dating back to Opposition days, was obvious to all.

I’ve been writing on this, and on Monday the Herald’s Jenee Tibshraeny had a powerful piece calling out the Minister and noting that – unlike the public – the Minister got no, or next to no, new information from the Ombudsman-led Reserve Bank release on Thursday. The title of her piece said it all really

but noting, importantly (and emphasis added), that “Both the Reserve Bank board and Willis have engaged in what looks like a cover-up of the circumstances surrounding Adrian Orr’s resignation as Governor in March”. offering chapter and verse. This wasn’t just Quigley’s doing (or that of his board and temporary Governor) but Willis’s too.

The Minister apparently claims to regard these criticisms as unfair to her. She was, we were supposed to believe, a helpless Karori mother, pleading in vain for Quigley to be upfront with the public about the loss of one of her key officials, holder of an office where she – as Minister – is personally responsible for any hiring and firing, the one to whom (as the law requires) Orr’s resignation was addressed. Tibshraeny had another piece yesterday afternoon reporting the Minister’s side of the story. This seems to be the essence of her case for the defence

Setting aside for now the question of how much money the Bank has spent trying to stop the public knowing, all this tells us is what we already knew: that the Minister realised rather sooner than the Bank – and Quigley specifically – that the coverup and active misleading was untenable and could not go on indefinitely, but (a) the resignation was in March, and her earliest such comments were in June, and b) she did nothing meaningful about it (until last Friday) when she could have insisted on transparency from day one, or any time onwards. She had (considerable) leverage. But it is pretty clear that she and her office were fully party to the strategy of deceiving New Zealanders, probably hoping interest would quickly die away.

At this point, it is probably helpful to step back and step through the timeline in February and early March. (My overall, and updated, timeline is here.)

In preparing yesterday for this post I went back and read quite a lot of the initial coverage (5/6 March) and some of the OIAs. It was in a BusinessDesk column, dated 5 March, by their highly-experienced and regarded Pattrick Smellie, that I noticed this

I don’t recall noticing it at the time, and it has had no apparent follow-up. Perhaps it seemed (like a number of other things) unimportant that day, when it appeared that Orr had simply tossed his toys and walked off, and if it was apparent that we weren’t getting the full story, there was no reason to think we were being outrightly lied to. I have no idea whether Smellie’s “it is understood” had substance – but he doesn’t seem like someone who just interviews his typewriter – and put no further reliance on it, but if there is anything to it (or to the suspicion of it), it is probably relevant context. Once again, on RNZ this morning, the Minister was claiming it was important that she had nothing to do with the hiring/firing (or facilitated resignation) of Reserve Bank Governors, even though her role is quite central and explicit in the carefully designed Reserve Bank Act (current version, and all its predecessors since 1989).

The story seems to have unfolded through February. On 5 February Orr, having become frustrated with Treasury, advises his board and senior management that he had told staff to “cease and desist” negotiating funding agreement issues with the Treasury, suggesting that it should now be a matter for the Board and Minister directly. That stance seems not to have lasted because 10 days later (14 Feb) Orr and Quigley were exchanging notes about agreeing a deal with Treasury the following week.

But in the meantime, the Minister had been trying to get meetings that month with Orr on both funding agreement and bank capital issues. One of the Herald’s various OIAs revealed that Orr had been stonewalling, using as an excuse the “sacrosanct” nature of MPC deliberations during mid-February, and suggesting that he couldn’t meet with the Minister then, even on quite separate matters (this of course didn’t stop him having his usual pre-MPS meeting with the Prime Minister and Minister of Finance the day before the MPS itself was released). The meeting between Orr, Quigley (and, for part of it, Hawkesby), the Secretary to the Treasury, and the Minister on the afternoon of Monday 24 February was the earliest date Orr appears to have agreed to. In the interim, Orr had once again lied to the Finance and Expenditure Committee and, that same day (20 Feb) he and Quigley held a Funding Agreement meeting with mid-level Treasury officials where, not only was there no meeting of minds or settlement, but Orr so completely lost his cool, and must have refused later to apologise, that Quigley chose to put in writing an apology to the official concerned. Just an extraordinary situation – a board chair helpless in the face of his chief executive’s misbehaviour, unable even to secure an apology from the chief executive himself.

We do not know whether the Minister was aware of this episode before the meeting on 24 February. There is no paper trail shedding light on that (one way or the other), but it would be surprising if she was not made aware of how combustible Orr had become over these issues (and would the mid-level official handling Funding Agreement negotiations not have told his own boss or Rennie himself what happened, would no one in Treasury have alerted the Treasury secondees in MoF’s office, or indeed her – ex Treasury – political adviser? Would Rennie not have mentioned it to Willis?) Phone calls and oral advice don’t easily get captured in OIA responses, unless it suits responders to do so.

And so we come to the 24 February meeting. The Treasury file note of that meeting – which so enraged Quigley when he learned about it as the OIAs rolled in – is here. I had previously defended Treasury, noting that the record – of a high level meeting on important outstanding issues – seemed both reasonable and moderately expressed. But, as it happens, Tibshraeny revealed that yesterday she had a OIA response from Willis (beyond the original deadline) making it clear that the Minister herself had been very keen to have the meeting properly documented, having staffers followup with Treasury to ensure that it was being done.

This was the meeting where the Governor distanced himself from the Board, bagged Treasury, and then (so it seems reasonable to deduce) stormed out.

One thing I hadn’t previously noticed about this file note is that it records comments from the Minister on the earlier agenda items (bank capital reviews she was seeking, and banking competition issues) but there is no comment from the Minister recorded on the Funding Agreement issues (either before or after Orr walked out). It also records no comments from Treasury. Is that really credible (was it really only Orr and then Quigley who made any comments of substance?) or did it suit the Minister not to have had anything she said on those issues documented (given that we now know she had an active interest in the file note)? I don’t know, but it seems a reasonable question.

Things must have escalated quite quickly from there. It just isn’t conceivable that after that performance by Orr, coming on top of the 20 February episode at Treasury, that there was no contact to reflect on what had gone on between Quigley and either the Minister herself or senior people in her office (the latter perhaps for plausible deniability?) Quigley had pro-actively apologised for Orr’s conduct to a mid level Treasury official, so how much more assiduous was he likely to have been around the Governor’s performance in front of the Minister (especially when so much – future Bank funding – depended on the Minister)? Perhaps it was a one on one after the meeting, perhaps a phone call or two, but surely something?

At very least we know (from the RB’s June release) that within 24 hours or so – and before the board itself had met – various top RB officials independently became aware that exit was possible and established an ad hoc to manage the situation if it escalated. I happened to be listening yesterday to the recording of the Minister’s estimates hearing in June and there she states (three times) that it was on 24 February itself that she was told by the Secretary to the Treasury that “employment discussions” were underway between the Board and the Governor. (Other material suggests she may have had that date wrong and that the advice was on the 27th, but she did repeat the 24th a couple of times, in a hearing for which she will have been extensively prepared.)

And if, and the Minister now claims, she had next to no involvement in what came next, that must have been wholly and solely a tactical choice by her. She was, after all, one of the government’s senior ministers, the person concerned was one of her most senior officials (and by far the most prominent) and, by contrast, the Bank’s board then was almost entirely made of underwhelming Grant Robertson appointees, and Quigley had an established track record of not being a safe pair of hands in front of journalists etc under scrutiny. The Minister may have wanted to establish a “look, no hands [of mine] in this” but not only can she not credibly disclaim responsibility, but if there were concerns the board had – about things not visible to her – surely (as the hirer and firer) she had an obligation (to Orr, if no one else) to check them out. It might just have been an aggrieved, out of their depth, board. But, of course, Willis was aware throughout that that 24 February meeting – in her office – had been the final catalyst for the ouster. (And to be clear, I am not in the slightest critical of the ousting itself – Orr should never have been reappointed, and he appears to have acted recently in ways that handed those with power his own head on a platter.)

The Board and Orr met, and then exchange emails, including notably the Board’s statement of concerns for which they sought a response from Orr. (The Bank’s release last week only explicitly mentions recent issues, although my – generally reliable – inside source told me that it included concerns dating back several years.)

Through these days the Minister chose to up the ante, by providing quite specific comments to the Herald’s Thomas Coughlan for this article on Reserve Bank funding he published on 27 February. At the time, I thought nothing particularly of it, except of course to welcome comments suggesting cuts were likely to be required, because I/we then knew nothing of the backdrop. But the Minister did, and it is probable that she chose to respond to Herald inquiries, and to be as specific as she was, after the 24 February meeting, and knowing that a showdown with Orr was underway, knowing indeed that the Board would be meeting – and Funding Agreements issues would be on the table – on the 27th.

It was on the 27th that the statement of concerns was sent to Orr, and also when he got board approval for him stepping aside, remaining out of the office until the situation was resolved, with Christian Hawkesby to act as Governor. The Minister has since said she was aware that Orr had stepped aside earlier (before 5 March), and we must presume she was advised of it that day (there are – content redacted – texts involving Rennie and MoF that day). Are we really supposed to be believe that a highly political senior minister didn’t ask what was going on, or gave no guidance? If so, it can only have been because she did not want to be fixed with knowledge, but that does not change the fact that the evolving situation was her responsibility (she hires and fires, she is accountable to Parliament, the Board is accountable to her). At any point, she could have intervened and taken control (and probably should have, most especially around exit agreement issues).

By this point it appears that both sides (Orr and the Quigley, the latter for the board) had resorted to “senior counsel” to negotiate terms. By Monday afternoon (3 March) the ad hoc management committee had heard that agreement had been reached – although presumably formally documenting it means it wasn’t signed until 5 March. The plan at this point was for an announcement on either the Friday (7th) or the following Monday (10th), although at the last minute this is brought forward to 1:30pm on 5 March after Orr alerted people to concerns about leaks.

The Minister says, and I guess we must believe her, that she did not see, and has not since seen, either the letter of concerns or the exit agreement. But, again, this does not absolve her of responsibility. They were her board, Orr was her responsibility, and she was the one who was going to have to face parliamentary scrutiny. Did she not seek any assurances about lump sum termination payments, or things that resembled them? Did she not raise any issues about what would be said, by whom, when, let alone what sort of NDAs Quigley and the Board might be signing up to? The paper trail does not tell us, but it seems utterly inconceivable that there was no communication about what the story was going to be or how it would be told. And, again, if the Minister just sat back and let Quigley get on with it, she made herself part of such a strategy, if only by acts by omission. She was not a helpless victim (of Quigley here) but a powerful player making deliberate choices.

The paper trail suggests that the Minister had the planned Reserve Bank press release by late morning on 5 March (sent across by Quigley). This statement, which had been lawyered by both sides, represented the first attempt to spin the story. Recall that the Minister was not an innocent bystander here – it was her to whom Orr was actually resigning. The press release was full of “good job, well done, time to step aside” fluff, and there is no sign that either the Minister or anyone in her office raised any objections (to the text, or to the Bank-attached note which indicated that there was no plans to say anything further “if” there were questions). Willis knew that the statement was intentionally misleading – she has since told us she knew about the “employment discussions”, she’d been in the 24 Feb meeting, she knew Orr had been gone for a week, and yet she raised no objections. She doesn’t even seem to have asked what commitments had been made, by either side, under an NDA. But those were her choices; she went along.

OIAs reveal that she instructed her staff not to reveal to journalists what the 24 Feb meeting had been about, briefing notes (backpocket Q&As) prepared by her staff (and provided to PMO) were actively deceptive (“Did you have confidence in Adrian Orr as Reserve Bank Governor? Yes, I’m confident he discharged his obligations under the Act and that is consistent with the advice I received from the Board”, “Is Adrian Orr’s resignation linked to the funding agreement? Not that I am aware of.”), and her office encouraged her to use the “personal reasons” story (which wasn’t in the first press release), although it seems that she didn’t quite go that far herself on the day. Her own press secretary conflated – no doubt to Quigley’s annoyance – “personal reasons” and a “personal decision”, and when mid-afternoon the office was advised that Quigley was releasing another brief (and known to be misleading) comment (“Adrian’s decision to resign as RBNZ Governor was a personal decision. He has conveyed that with consumer price inflation within its target band, this time was right for him to step down.”) there is no sign that the Minister or her advisers raised any concerns whatever, not even to wonder how tenable such a position would prove over time.

But it goes on. Reserve Bank releases, my insider leaker, and the Minister’s own OIA releases suggest that Quigley had not wanted to do a press conference, but that he and the Bank were pressured by the Minister and her office to do so. And so he did. No one thinks he handled it well. And what were the Minister and office expecting or hoping he was going to say? Not the truth surely? They were fully complicit in the Bank’s approach.

I’ve had a automatically-generated transcript of the audio for some months but it was hard to read. Yesterday, I found the video of the press conference in a Stuff article from the time. With that, I completed a full readable transcript.

To assist readers, here I have inserted – in red – comments on the truthfulness (or otherwise) and straightforwardness of Quigley’s answers.

Quigley press conference on Orr resignation 5 March 2025 WITH ANNOTATIONS

It really should serve as a case study for future crisis management communications courses and exercises in how utterly not to do it.

Much of the ground I’ve covered before so I won’t requote here in detail. It was obstructive, it was deliberately and knowingly misleading, and on occasion it was just outright false. As just one small example – which we have only known was false since last Thursday but the Minister says she knew all along – was his claim that there had only been an acting Governor since lunchtime that day.

It was utterly deceptive and misleading.

And yet, shortly thereafter a Post journalist emails the Minister’s chief press secretary and asks “is the minister satisfied that the Reserve Bank Board chair has given a sufficient explanation for why Adrian Orr suddenly resigned from his job.” An hour later Venter replies with a simple “Yes”. That was, as I noted above, reported in The Post at the time, but it didn’t seem very important, since we had no idea we were being lied to, apparently with the Minister’s knowledge and approval.

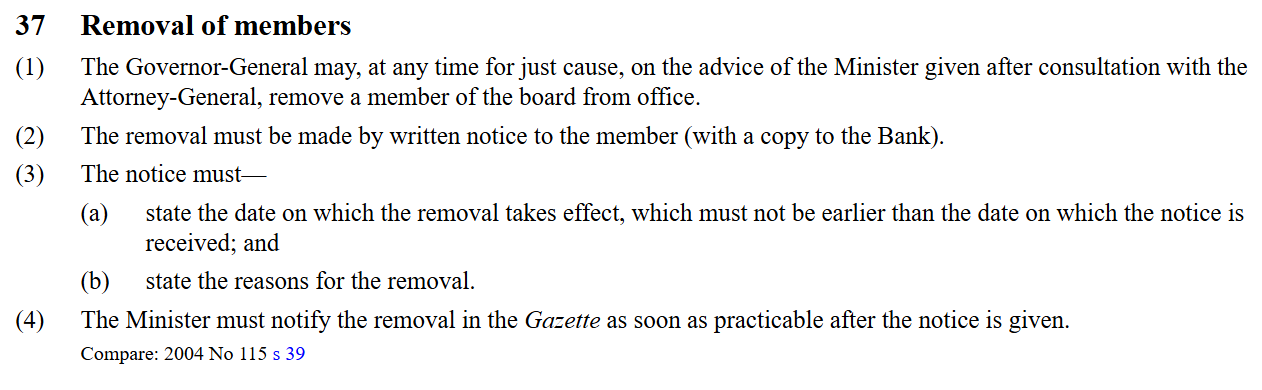

Willis has continued, to yesterday, to claim that, even thereafter, she was helpless, apparently an innocent victim of a board chair who ran amok. It is a story that doesn’t stand even a moment’s scrutiny. Not only could she have (threatened to) remove Quigley any time she liked (at will, not for cause), but (as she has confirmed) she was not party to any NDAs, and she (and Treasury) knew quite enough that she could have insisted on transparency at any time she chose. She and Treasury could have released the 24 Feb file note months ago, or the Quigley email apologising for Orr at the 20 Feb meeting. She could have insisted we were told “employment discussions” had been underway between the board and Orr, with her knowledge, she could have been open about the stark difference of view (she was aware of) on Funding Agreement issues, and by April she could have insisted on the release of that extraordinary Quigley email protesting that Treasury had written a file note of the 24 Feb meeting and might release it. She could have insisted, without overriding the RB on specific OIAs, on an early statement – or made it herself – on the lines on “Following employment discussions initiated by the Board, and brought to a head by differences between Orr and the board over funding agreement issues and Orr’s behaviour in several recent outside meetings, it was agreed that Orr would resign.” There would still have been follow-up OIAs, but we’d have been starting from a truthful statement, not from false and/or misleading statements exposed only by OIA upon painful OIA, a leaker, and some (limited) support from the Ombudsman.

The Minister of Finance was, therefore, an active participant in choices about what was done and what was said about what was done. That was so before the announcement on the afternoon of 5 March, before the Quigley press conference, and then for months afterwards. She knew the truth and she chose repeatedly and persistently, to keep it from New Zealanders. That is pretty extraordinary, pretty inexcusable.

One is left wondering how they (Board, Hawkesby, Willis, her advisers) ever thought they were going to get away with it. No one seems to have stress-tested a comms plan, which is extraordinary in itself, for an event of such significance and inevitable public and commentator and (belatedly) political interest. I guess it is good that Willis realised before the Bank that the game was up and that something closer to the truth would have to come out, but even then for too long her response was feeble, possibly concerned that doing more would – as it has done – expose her involvement and support for the approach more fully.

The fault was not in helping to engineer Orr’s exit – that is to her and Quigley’s credit, given the glaring behavioural record, come to a head in late February – but in the choice to obstruct and to mislead New Zealanders. And people wonder why trust in our institutions and politicians is in decline……

UPDATE: Forgot to include here that press release of MoF’s last Friday afternoon announcing Quigley’s resignation, with all the spin about “good job, well done, time to go”. Perhaps she never even read it before it went out, and she did back away moments later in a radio interview, but….