A couple of nights ago, shortly after the Minister and Treasury finally released the suite of texts between Willis and Rennie, ZB featured interviewer Heather du Plessis-Allan talking to Herald journalist Jenee Tibshraeny (who has been over the Orr/Quigley/Willis saga issue from day one). There wasn’t anything concrete that was new in the conversation but it was the ending that struck me.

Tibshraeny: In this instance I’m disappointed by the lot of them. I can’t even distinguish who is most culpable and feel like as a member of the public I’ve been misled and it is disappointing.

Du Plessis-Allan: It just looks like a giant cover-up doesn’t it?

Neither of them seem like zealots, let alone anti-government zealots with an agenda. So what a sad state of affairs we’ve come to in this country.

But the Minister has clearly found herself some supporters in The Post (their journalists have also been a bit sympathetic to Orr) with an article this morning where they claim – it must have been music to Willis’s ear – that “overall, Willis appears to have helped rather than hindered the fuller facts going on record while not at any point seeming to defend the Reserve Bank’s own miscommunications”. Which would be an extraordinary claim anyway, but it was belied by the fact that a few paragraphs earlier they had reminded readers that on 5 March, after the deeply problematic Quigley press conference, Willis told The Post journalists that she was satisfied with the explanation Quigley had given for the Governor’s departure. And, of course, none of the explanations given that day (and there were several, mostly designed to have us accept something like “inflation is in the target range, time to do something different, nothing to see here”) were at all convincing, and the Minister – who had urged Quigley to do the press conference – knew that the public had been actively misled then. And if perhaps she coulddn’t predict quite how badly Quigley was going to do when she got him to go out there, there is no sign – not the slightest – that she either expected or wanted him to tell the truth. And, of course, over the subsequent months she did occasionally wring her hands in public, regretting eventually that the Bank wasn’t being a bit more open. But…..she is the Minister of Finance, with knowledge and leverage, not “helpless mother from Karori” putting her thoughts in Letters to the Editor of The Post. She could have acted, she chose not to do so, and if it hadn’t been for the Ombudsman we might still have been dealing with official denial and avoidance, enabled by her. That she enabled the obstruction and coverup for months is nicely captured in this exchange with Heather du Plessis-Allan just six weeks or so ago.

Of course as I noted last Friday there are still material unanswered questions about how the choices – big picture and detailed – of communication of the Governor’s departure (and supportive messaging etc) came together. Statements of that sort don’t emerge in half an hour, and there were material choices to be made. It is hard to believe that no one in the Minister’s office had any involvement, or that they and the Minister were not actively thinking through the issues and risks and options pretty much from the time the Minister got that text from Rennie on the evening of 27 Feb suggesting things would now come to a head fairly quickly. I’ve lodged one more OIA on those matters this morning.

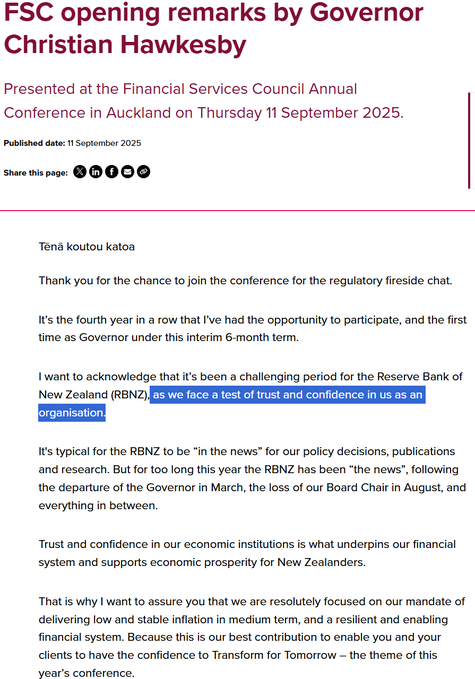

And then of course there is the Reserve Bank itself. The temporary Governor turned up yesterday to speak at the Financial Services Council and began this way

I suppose we should give him a little credit for even mentioning the “test of trust and confidence in us as an organisation”, except that….having giving it a passing mention he went on to talk about inflation.

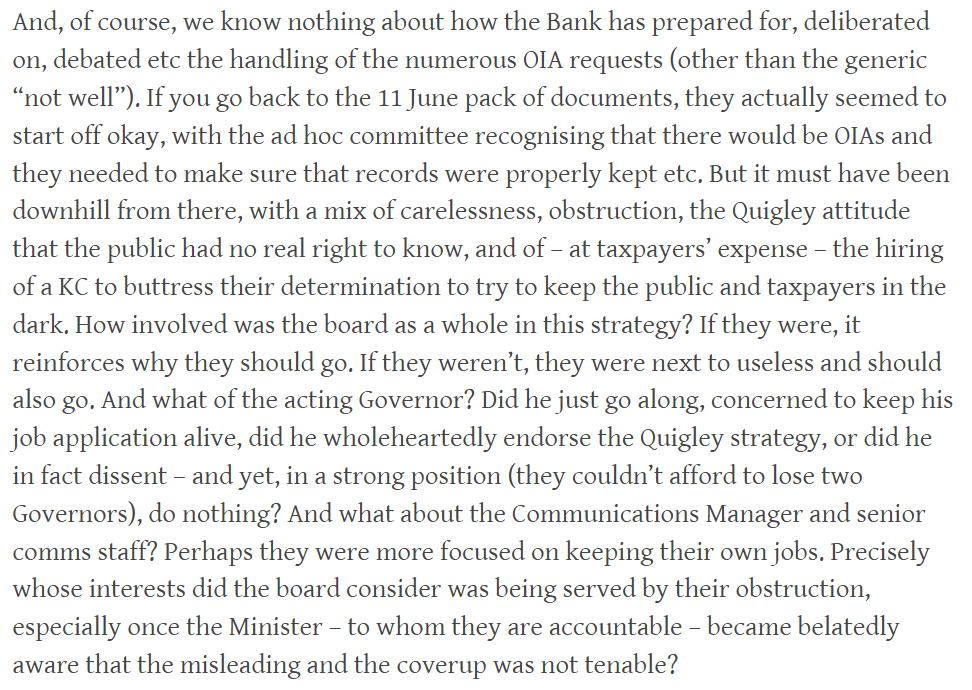

There are still serious questions for all those involved at the top level of the Bank (temporary Governor, board members, key communications staff etc). Rather than write it all again here is a paragraph from last Friday

I’ve also lodged an OIA on those issues those issues this morning. But the wider questions for the Board become even more pointed now that we know they were so intent on getting Orr out that they were likely to recommend the Minister to dismiss him just a few days after their formal process had begun (predetermination and all that?). And yet they still apparently thought it just fine to deceive the public – approving Quigley’s actions presumably – and to go on doing so for months. People of integrity would resign at this point.

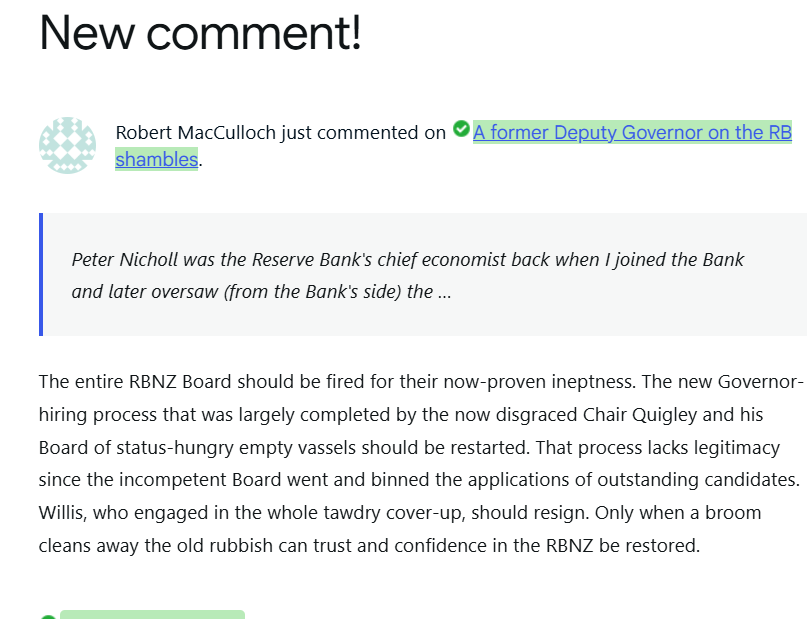

Late yesterday after my short post with former Deputy Governor Peter Nicholl’s article on the Reserve Bank shambles (and specifically the governance failures), Auckland university professor of economics Robert MacCulloch left this comment

Taking his point about the questionable legitimacy of the Quigley-led (and rest of Board) process for selecting a nominee, I’m not sure I’d go quite as far as he does. Time is moving on, and there is a pressing need to have permanent new management in place. On the other hand, quality really matters. So my stance is probably that the Minister (and the wider Cabinet) need to ask themselves very seriously whether any nominee they have settled on really reaches the standard needed now: a first rate independent highly credible person of gravitas, management capability, and some intellectual stature. If they have, well and good. If not, then there would be a case to reopen the process (preferably after sorting out the board members themselves). Rumour hath it (well, a journalist told me) that the nomination has already gone out to the other political parties for consultation. Here the role of Barbara Edmonds becomes really quite important. If she can really be persuaded that a nominee is not just “any warm body, because the job needs filling” but a serious credible and respected figure, then that could be quite persuasive (and recall that the legislative provision Labour introduced requiring consultation with other parties was presumably done in the spirit of the notion that a person appointed as Governor really should command at least grudging respect across the spectrum). But if Edmonds isn’t convinced – and the situation has deteriorated further in the last couple of weeks – she and her leader need to be willing to take Willis aside and say so.

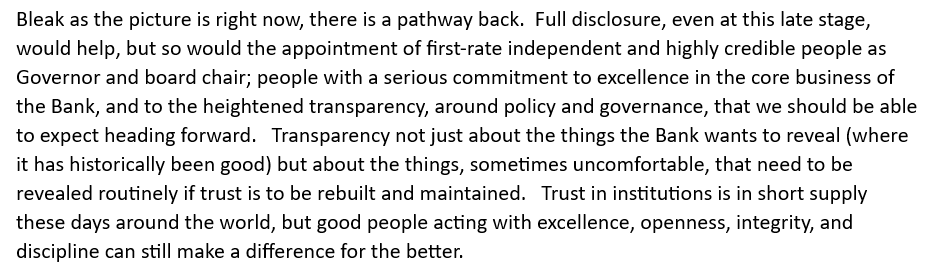

And finally for now on this issue, this is the closing paragraph of a piece I wrote earlier this week on the whole grim saga.

And is that for a while. My wife are heading off on a month’s holiday tonight so it will be at least a month before there is anything more from me here. By then, one hopes, there might have been announcements of strong credible independent people to take up the two key roles, Governor and board chair (and, actually, a new MPC member too). Perhaps some new commitments to greater monetary policy transparency too, along the lines Kelly Eckhold at Westpac suggested last week. But we’ll see.

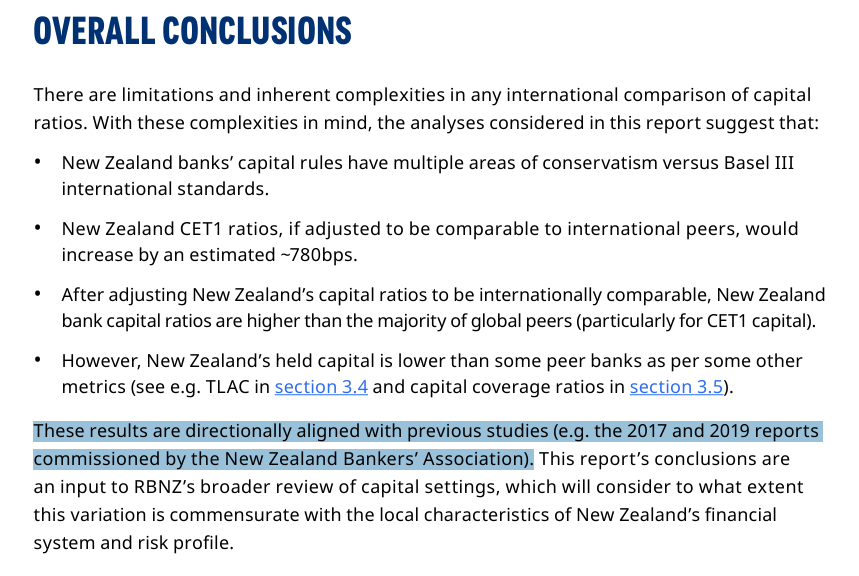

And that means that among the various other things I just never got to in recent weeks was making a submission and a substantive post on the Reserve Bank’s consultation on the capital requirements review that the Minister prompted them to initiate once Orr had gone. As it happens, I don’t have much problem with what they are proposing, and I really strongly welcome the fact that the interim guard (Hawkesby/Quigley) did go to the effort of commissioning a decent external consultant to review bank capital levels in New Zealand and those in a bunch of other somewhat comparable advanced economies (a measurement exercise rather than a policy one). Orr refused to commission anything of the sort when he was still unilaterally in charge in 2019. This was the conclusion of that new report.

My own issue with the entire framework – 2019 (eg here and here) and now – is that it is built on assumptions about the (GDP) cost of banking crises (themselves, the bits able to be ameliorated by capital buffers) that bare no relationship to reality in advanced economies, no matter many decades one looks back. The Bank now justifies sticking with this assumption – which is crucial to any serious cost-benefit analysis – on the grounds that it is “internationally conventional” in such work. No doubt “Internationally conventional” provides a safe harbour for bureaucrats, but it is no substitute for serious thought and critical review.

It is arguable that this unsafe assumption may not matter unduly at present, if market demands (shareholders, bondholders) mean that banks would choose to hold quite high capital ratios even if regulatory requirements were set lower. And of course – another thing not mentioned in the consultation – is that for our largest banks it would be APRA rules that would still be binding even if the Reserve Bank were to adopt an even less demanding model. But we really should be able to expect a higher standard of analysis – including such basics as the ability to distinguish the costs of misallocating credit and real investment in the preceding boom from those narrowly from actual bank failures or near-failures themselves – from our financial stability and bank regulatory agency.

I plan to blog the OW report. Three key points:

These differences should prompt the Reserve Bank to invest in high-quality staff who understand these nuances.

Best wishes for the holiday. I hope you’ll return acknowledging that our Minister of Finance has overseen the removal of two officials who showed little respect for those outside 2 The Terrace. Maybe not the most streamlined way of dealing with the two, but hey, these are chaps with large egos who can draw on legal support as well as support from political parties. That should give pause for thought.

LikeLike

Will look forward to your post.

I’ve been consistent in saying “well done” for getting rid of Orr, really the first opportunity he presented them. Not giving her any credit for Neil tho: first, she reappointed him (with all his known faults, and being as responsible for Adrian’s reappointment as anyone), then she worked with him to lie to NZers for months, and did no more than handwaving when she realised the coverup couldn’t go on. And, of course, she refused a couple of chances you and/or I gave her for getting rid of Neil (apart from anything else it should have been done a week after Adrian left, to leave a new broom driving the selection process).

LikeLike

It must have taken time for her to recognise she was dealing with not so good-faith actors. Moving from the typical academic/bureaucratic mindset—”let’s commission another report,” “wait and see,” “this will blow over”—to acknowledging an uncomfortable reality that not all of us are do-gooders. Here’s a nice example of such selective attention: https://youtu.be/6GMgvfNAFQs

She was facing an organisation displaying characteristics found in organised crime: believing certain rules don’t apply to them.

LikeLike

Which is where I think Tsy is quite culpable. They weren’t watching the Bank closely despite years of dealing with Adrian and Neil and seem not to have been assertive in advising the new MoF. She of course had a fair idea of Adrian’s character – and would have had more of one if she had been open to engaging with a range of views/people.

LikeLike

The other thing I meant to add to my brief comments on the capital stuff is, just as in 2019, how much better if they had tabled all this stuff, including views of the external experts, in a workshop/conference with presenters, discussants, comments/questions from the floor etc. instead it seems we will only get the externals’ take after decisions – made by a board with little legitimacy at present – are taken.

LikeLike

Agree that would have been great. I already hear complaints from the bank that the RB went at it alone without discussing the revision with banks. I fear that a lack of confidence plays a role.

LikeLike

The only function of this government bank is to launder the government debt.

The production of endless reports and fluffery around modelling is something the army of econometric whizz kids could surely do on a sunday afternoon at their own own expense. The entire saga reinforces yet again that another institution is nothing more than the replaying of the movie. “Look the Emporer has no clothes”

LikeLike

Well Michael, I really admire your tenacity in dealing with this, BUT: Expecting Barbara Edmonds to approve this governor after being instrumental in appointing the previous disastrous one, is really expecting the lunatics to run the asylum.

Excuse my cynicism!

I’ve just attended the BizNews Investors Conference in a place called Hermanus in the Western Cape of SA, and the overall consensus by people in the know is that the SARB is a well-run and professional machine.

It seems to me NZ is slipping into turd-world status at an alarming rate. I hope I’m wrong!

Regards, Jan

LikeLike

Bit unfair to blame Edmonds for the reappointment of Orr. She wasn’t in Cabinet at the time.

LikeLike