As I outlined in my post on Friday, it now seems that much the most likely explanation for the sudden no-notice departure of the Governor of the Reserve Bank is that he was ousted; not formally sacked by the Minister of Finance (as she might well have had grounds to do, but it could have got messy), but – having left himself vulnerable by his record of questionable conduct – engineered out by the Bank’s Board (more specifically its chair), almost certainly with the foreknowledge and acquiescence, and possibly the direct encouragement, of the Minister of Finance herself. If so, well done them on that count. But the subsequent and ongoing active deception of the public (and of the Bank’s own staff), and the apparent defiance of the Official Information Act, is simply inexcusable, and it would seem that the Board (especially the chair), the Minister, and the temporary Governor share responsibility, to one degree or another, for that.

Looking back now, it is puzzling that this hadn’t seemed the most likely explanation pretty much ever since Orr left on 5 March, or at very least since the Bank’s big release, and statement, on 11 June. I guess that is what comes of treating words out of the mouth of the Bank, and especially its chair, as having any degree of trustworthiness whatsoever. More fool me.

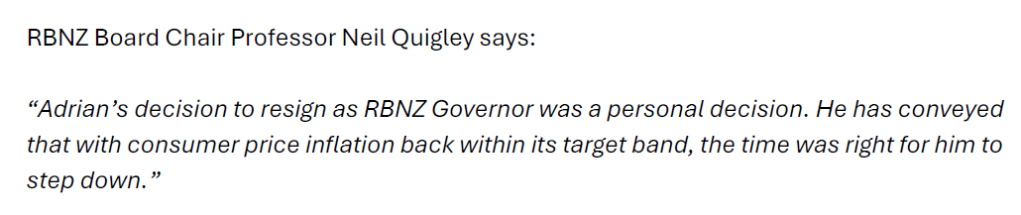

Recall that the first set of statements and Board chair comments on 5 March was clearly intended to lead us to believe there was nothing to see here. It was just a “personal decision”, there were no conduct, performance or policy issues at the heart of it, and really….when a big job was done, why wouldn’t an impressive leader take the opportunity to hand over the reigns. I won’t repeat all the things Quigley said that day, but this statement, issued by the Bank mid-afternoon on 5 March, after many questions had already arisen, rather captures the tone

Cincinnatus and all that. A couple of hours later he told the hastily-called press conference that he personally had still had confidence in Orr, and answered a direct question thus

The Bank spent the next three months blocking OIA requests and refusing to add anything, until the great reveal on 11 June. There was a set of carefully selected papers released (while avoiding anything on whole chunks of what must have gone on) and an official statement, presumably owned by both the Board and the temporary Governor and probably carefully vetted by lawyers (including ones for Orr?).

Having abandoned the 5 March story, this was all now carefully crafted to focus us on (a) that board meeting on 27 February, and b) a policy difference between the Board and the Governor which Orr, somewhat oddly, took so strongly to heart (“caused distress”) that he felt it would be better for him to simply go.

If you go back and read my posts when this release came out, you’ll see I never really bought the framing (which the Bank must have been pleased that much of the media followed) that this was a dispute over the Funding Agreement per se. As I have noted several times, many or most public service chief executives have suffered budgetary disappointment in the last couple of years, and none of them stormed off with no notice. But we were still clearly supposed to believe that whatever really happened, Orr had real agency (it was he who decided to leave, of his own accord, with no notice).

But there were still plenty of clues that it wasn’t the real story. There was, for example, the strident and repeated insistence by the Minister of Finance that it was all nothing to do with her, she knew little or nothing etc (even though she was the person responsible for the Governor, and to whom any resignation actually had to be addressed).

And there was the near-final version of the 11 June statement, which they’d sent out in error to OIA requesters shortly before the official general release time.

The shift from one (near-final) to the other (final) being clearly designed to remove any references to a meeting with the Minister and Treasury, and to draw attention away from them generally (and the earlier wording wasn’t going to have got into a near-final document of this magnitude by accident or the whims and failings of a junior staffer).

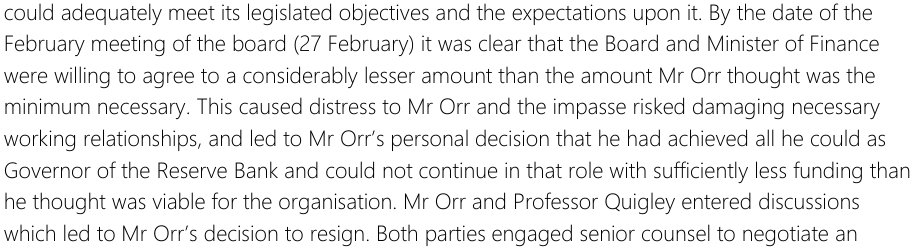

And there was the exit agreement itself, and negotiations being undertaken by “senior counsel” – interesting that that term was explicitly chosen by the Bank when they could easily just have used “lawyers” – for both sides. For an amicable departure, surely a quick chat with HR could have sorted out the application of Orr’s standard resignation terms, and any waivers of notice that might be sought or granted? And there was this summary (from the 11 June statement) of the exit agreement

Who typically has negotiated exit agreements? People being forced out (but not specifically fired). And Quigley has repeatedly referred to legal constraints on his ability to explain things, which can really only have arisen from the terms of this exit agreement, where Orr will have had some negotiating leverage (and were it all Cincinnatus-like there would be nothing for either side to want to hide – and no reason for Orr to have left the office the very day of the resignation, and yet be paid for several more weeks).

But things hung in limbo – hamstrung in part by the Bank’s obstructiveness over various OIA requests now having been appealed to the Ombudsman – until the account provided to me by someone who was clearly fairly close to events, and reported here. That person’s account was that (a) Orr’s behaviour had been very bad in a meeting with The Treasury on the Funding Agreement issues and then on 24 February in a meeting with both Treasury and the Minister of Finance, and that b) on the 27th, the day of the Bank’s board meeting, Quigley had emailed Orr a Statement of Concerns raising conduct issues stretching back several years and inviting a response. So the story went, at that point Orr decided to resign.

Treasury then disclosed an email sent by Quigley to a mid-level Treasury staffer after a meeting on 20 February apologising to that person that Orr had lost his cool in the meeting, in response to a perfectly reasonable question that Quigley acknowledged should have been anticipated and for which Bank management should have had a dispassionate answer. At a time when negotiations on the Bank’s future five-year funding were approaching climax Orr, in the presence of his chair, had (a) lost it with Treasury, and b) neither then nor later been willing to apologise himself (why otherwise was Quigley doing so, and not even on Orr’s behalf).

Then the Minister confirmed that “emotions were running high” in that meeting on 24 February too (around Funding Agreement disputes), while seeming to confirm that “employment negotiations” had been underway between Orr and the board in the days leading up to the resignation. And while the Bank has refused any further comment, they have also not chosen to deny any of it (including the alleged 27 February email, for which there is still no independent confirmation of its existence). Had there been no substance to any of this, they’d surely have owed it to both Orr and Quigley to (however briefly and tersely) set the record straight. They seem now to be hoping to wait out the Ombudsman.

And so the “engineered” ousting came to seem like the best working hypothesis for what had gone on. Perhaps on the spur of the moment, or perhaps lying in wait for some months, Orr’s conduct seems to have crossed the line (again – perhaps he’d been warned) and they had the leverage to get him to go. No doubt he was disheartened that he was going to lose the Funding Agreement fight and perhaps that made him readier than otherwise to go without much of a fight?

Anyway, having got to that point I decided to go back and reread that package of material the Bank had put out on 11 June, and see if any of it read differently in light of what we had since come to know.

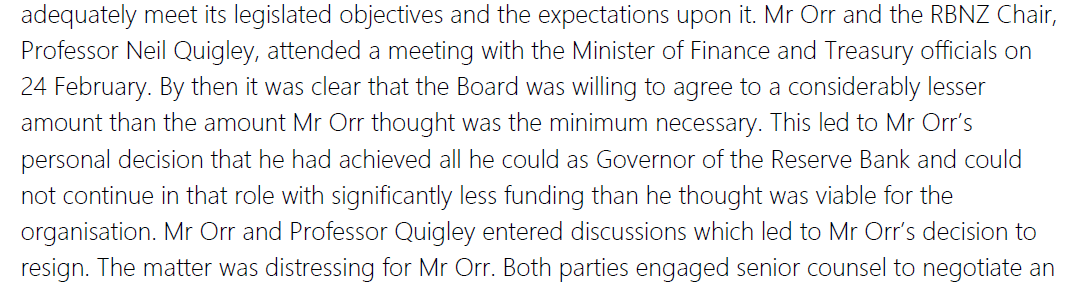

I’d assumed – I think understandably enough – that the Bank’s Board meeting of Thursday 27 February might have been decisive. The 11 June statement seemed to point that way, as did my source’s report that the (apparently) decisive email had been sent to Orr on 27 February, and the fact that the only indications of advice to Treasury or the Minister had dated from then (I’ve now asked the Ombudsman to review the extensive withholdings in that release).

And perhaps there was some sort of final showdown then and a final decision made (to call in the “senior counsel” to negotiate exit terms). But the Bank’s information release pack included this (read from the bottom)

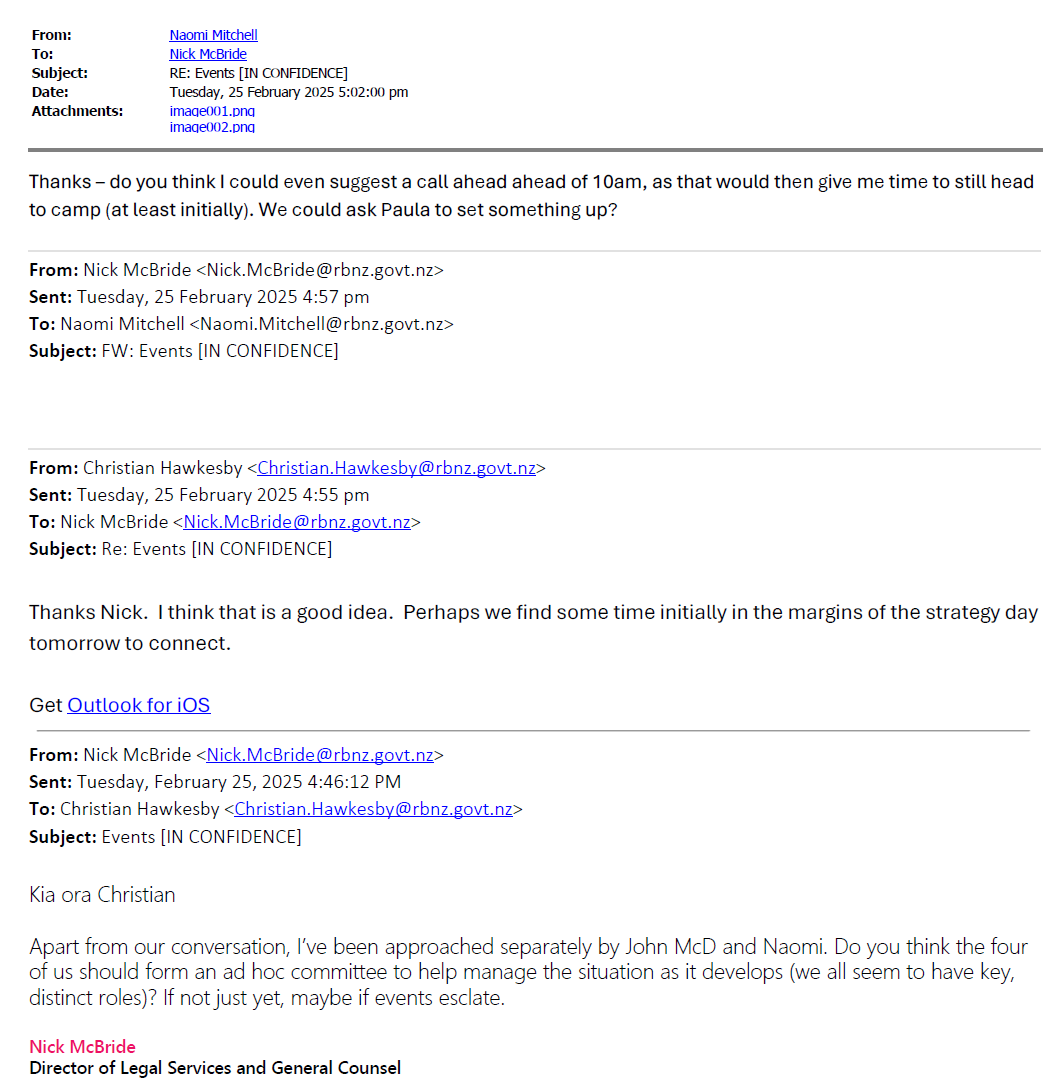

Who are the characters here? Hawkesby was (then) the Deputy Governor, McBride was (and is) the Bank’s General Counsel (but a third tier person, under an Assistant Governor who was also a lawyer), John McDermott was the Assistant Governor responsible for HR matters, and Naomi Mitchell was the (third tier) Director of Communications. And before 4:46pm on Tuesday 25 February [UPDATE: as it turns out, less than 24 hours after Quigley got out of that 24 Feb meeting] they already knew that something was afoot and agreed to the establishment of an “ad hoc committee” to help manage the situation. It seems clear that decisions had not yet been made (“If not just yet, maybe if events escalate.”) but this was two days before the Board meeting and just the day after that (“emotions were running high”) meeting with the Minister and Treasury. Was it Orr who told this group of his managers, or was it Quigley (Board chair)? We don’t know, but whatever had already unfolded – a serious risk of the Governor going presumably – was material enough for a range of key managers, not all direct reports to the CE, to have been brought into the picture (apparently separately/individually) this early. (This group then meets or exchanges messages over the remaining period pre and post resignation that was covered by the release.)

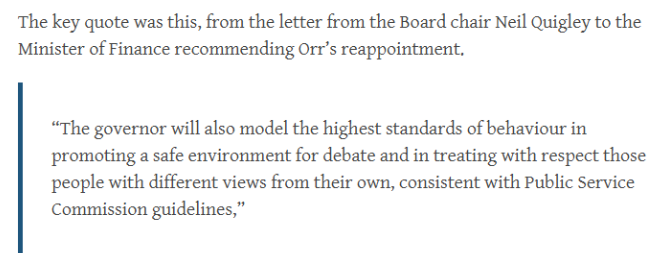

We don’t know what events were on the Statement of Concerns list Quigley is claimed to have sent Orr. As I noted last week, it isn’t as if he would have been short of examples just from material that had found its way into the public domain by then. But I wondered what other events might have been salient for the Minister and/or the Board.

I noted last week that when (with spectacularly poor judgement) Quigley and the Board had recommended Orr’s reappointment in late 2022 there had been this.

When this was first released some time back it seemed like little more than make-believe stuff. But perhaps it had been the basis for conversations with Orr at the time? After all, the Board (and Quigley) can hardly have been oblivious to the long list of concerns and issues, so perhaps there was some attempt at insistence on better behaviour in a second term?

If so, it didn’t go well. Even externally, Orr continued to mislead (or worse) FEC and media. As the Minister noted last week, she’d last year passed a complaint about Orr’s behaviour to a New Zealand Initiative employee to the board to address.

And we learned just yesterday that it seems that the Bank never told the Minister of Finance that they were going to budget in 24/25 for operational spending far in excess of even what Grant Robertson had allowed them for that year (although, to be clear, responsibility for that must lie with both Quigley – as board chair – and Orr, as CEO). Perhaps when Willis finally realised she had been had, she was (and I would hope she was) really annoyed and perhaps, as regards Orr, steel entered her soul (belatedly) at that point. Of itself, not quite dismissal material perhaps (after all, Quigley was responsible too and she’d just reappointed him) but enough to put you on watch.

Who knows if Orr’s conduct at and after those two February meetings was itself enough to lay him open to pressure to go. As yet, we have only quite sanitised comments on how those meetings went down (including the Orr/Wood exchange, where they were both trying to settle things down after the event) but it was repeated behaviour from a very senior figure within days, at a time when the Bank really need to maintain good relationships. If it wasn’t enough in itself, there was other stuff going on at the very same time.

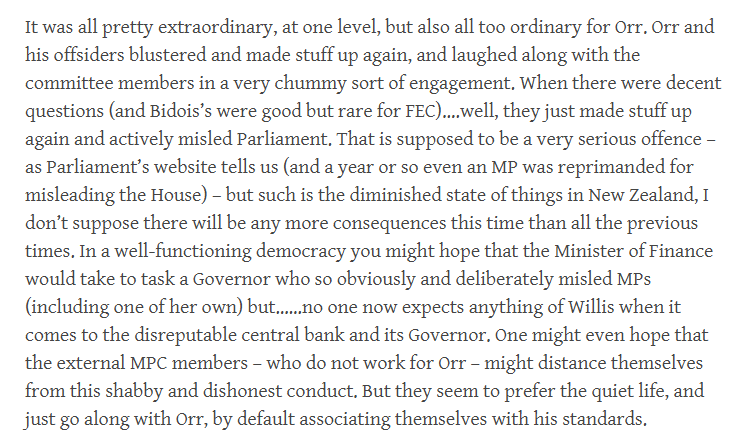

Going back to that period, I realised that it had been on the very morning of 20 February – the day of that unapologetic blow up at Treasury – that Orr had been telling demonstrable untruths again to Parliament’s Finance and Expenditure Committee (at his appearance on the February Monetary Policy Statement). I wrote about it in a post on 21 February, “Orr at it again”. I went back through that post the other day, and listened again to the video of the hearing to check that I’d heard and recorded things correctly. It was, as it turned out, probably his last public appearance as Governor and I counted five outright misrepresentations (two I would go so far as to call worse than that), all on matters where the Governor was either well aware of the truth, or should reasonably have been expected to have known the truth. (And just to be clear that responsibility is shared: at the table with him were his deputy responsible for monetary policy, Karen Silk, and the chief economist Paul Conway. In the row behind Orr you can see Christian Hawkesby, MPC member and Deputy Governor, Naomi Mitchell (Director of Communications), and one of the external MPC members. Not one of them made any attempt to correct Orr on any of these points.

The most egregious of Orr’s claims that day – although not necessarily particularly consequential, just the easiest to unambiguously refute – was the (repeated) claim that the Reserve Bank had been among the first central banks to tighten (when inflation took off a few years previously) and the new, and even more out of step with reality, claim that the Reserve Bank had then been among the first central banks to cut rates.

In my post that day I observed

As I noted, he’d done this sort of thing often enough before, but when I checked my records it seemed to have been the first time since the change of government that he’d been caught in such flagrant attempts to mislead a parliamentary committee (there are plenty documented in the years previously). Had he been less bad for a while, or had I not been paying so much attention? I ended up raising this episode with the Finance and Expenditure Committee the following week (before Orr’s resignation), in time with full chapter and verse – as I recall, I thought it was pointless to raise it with Willis, but the FEC chair was new.

I don’t suppose this particular episode of egregious behaviour – which his senior team seemed to walk by – had anything particularly to do with Orr’s ouster, underway just a few days later. My point is only that if for whatever reason you think what we know of those two private meetings mightn’t really have been serious enough to use as a lever to oust Orr, there was plenty more behaviour that could have, this one visible to anyone who chose to watch/read. If Willis helped engineer the ousting of the Governor, she did us – and standards of public life in New Zealand – a service.

None of which – not NDAs, not nothing – warrants participation in active and repeated, ongoing now, attempts to mislead New Zealanders and obstruct scrutiny. And if – as the Minister suggests – she isn’t overly happy with how the Bank is now handing things, the Board chair serves at her pleasure. If she wants different standards, a good way to signal that would be to replace the chair, now.

If something like what I’ve hypothesised here is what happened back in late February and early March, perhaps the Board and Minister should have insisted on a terse statement along the lines of “Following discussions initiated by the Board, the Governor has resigned and has left office today” and said nothing more that day. It wouldn’t have stopped the questions, or the OIAs. Perhaps it wouldn’t have proved tenable, or Orr wouldn’t have agreed. But there is just no excuse for the deliberate repeated ongoing effort to mislead us.

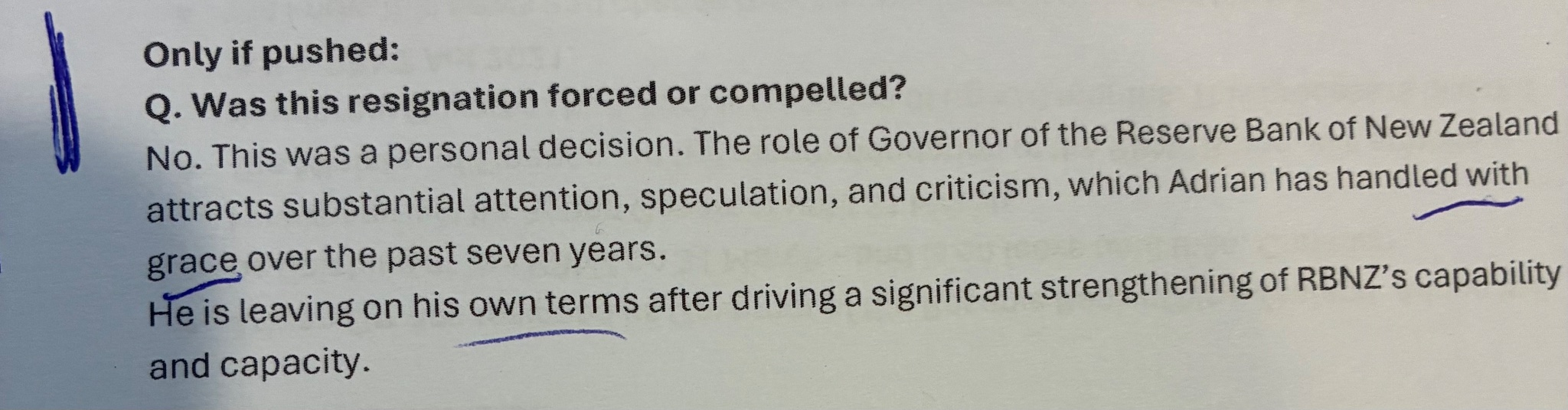

Or their staff. This was from the package of Q&As sent out by Naomi Mitchell to the entire Bank second and third tier mamagement group first thing in the morning the day after the resignation, for use with staff.

Yeah right.

I must say I’ve always figured they forced him out. When people were complaining about Willis not immediately sacking him, I regularly pointed out that sacking him would get expensive, but simply riding him to do his job properly until he gives up and leaves is how you normally get rid of people who aren’t aligned with your objectives.

On that reading, the sequence of events is:

LikeLike

Quite sympathetic to a fair bit of that (and like you I often made the point incl before the election – that a new govt could not just sack him), but I think you give far too much credit/grace to Quigley. I’d be really surprised if there was any reluctance by the board to reappoint in 2022, or if Robertson had to take the lead in encouraging them, plus Quigley is fully as responsible as Orr for last year’s budget blow out (and, as per my post yesterday, the failure to alert MoF that this is what they were doing. Also not sure she has much confidence in him going forward – she has twice now openly lamented how they’ve handled the comms – but maybe she just feels lumbered with him, and won’t want to open another front for critics of the med school.

LikeLike

Yes, more than possible.

It also may be as simple has having no other suitable candidates, and not wanting to change too much all at once. They’ve had enormous difficulty filling the Health NZ board given how they treated the last Health NZ board, how much they pay, and how much they expect. Not to mention who they’ve chosen to make chair.

I can easily imagine that the pool of people willing to be chair of what is also becoming a quite politicised board may be pretty small. Perhaps better the devil you know.

LikeLike

Of course, this is a v well paid chair role ($200K or so, higher than the usual govt board scale even with this week’s increases). I think she made a mistake in her first few months in office in not then finding a strong and credible potential new chair and being ready to have that person in place from 30/6/24 when Quigley’s term expired and ensuring all the vacancies were filled. Of course, working with Adrian was always going to be a pain, but there is still some prestige around a central bank board role (well, would be if it weren’t for the current mess)

LikeLike

Thanks Michael.

Wonder if you’d care to speculate on how the replacement process is proceeding ?

im curious. There must be scuttlebut in Wellington.

LikeLike

No idea, altho I think they were supposed to be getting close to being able to make a recommendation to MoF fairly soon (even then the process may be quite slow because other political parties need to be consulted and an appointment would need to go through Cabinet. But anyone who is not just driven to want the job at any price must be looking at the mess and wondering “do I really want this”, including “am I comfortable working under a chair so ready to actively mislead people”.

LikeLike