Yes, that subject again/still.

Today, three main points:

- the comments by the Minister, including claims that she didn’t know why Orr had resigned

- the latest set of Quigley comments given to Newsroom’s Jonathan Milne, and

- (largely for the record) restating events around MPC appointments that are minimised by Milne but which reinforce the sense that Quigley is unfit for the office he holds.

But first, a reminder of history. In The Post this morning it is claimed that “a governor had never resigned out of the blue before”. There have only been four Governors in the modern (independent) era and two of them have resigned out of the blue. Don Brash did on 26 April 2002. His resignation was announced at 9:54am that morning, with a brief explanation (including that there had been no disputes with the government) and an announcement that there would be a press conference (off site) at 11 that morning. where Don answered all sorts of questions. There were no gagging provisions, no secrecy or active misleading. If as Reserve Bank Governor you are going to resign and go with no notice (which I don’t advocate), it was the way to do it. The Minister, Board, and Governor might usefully have refreshed their memory of that experience in the week or so they had to prepare for Orr’s departure (there is no mention of it in the documents released the other day), rather than setting out on months of (as yet not fully resolved) obfuscation and distraction.

Willis

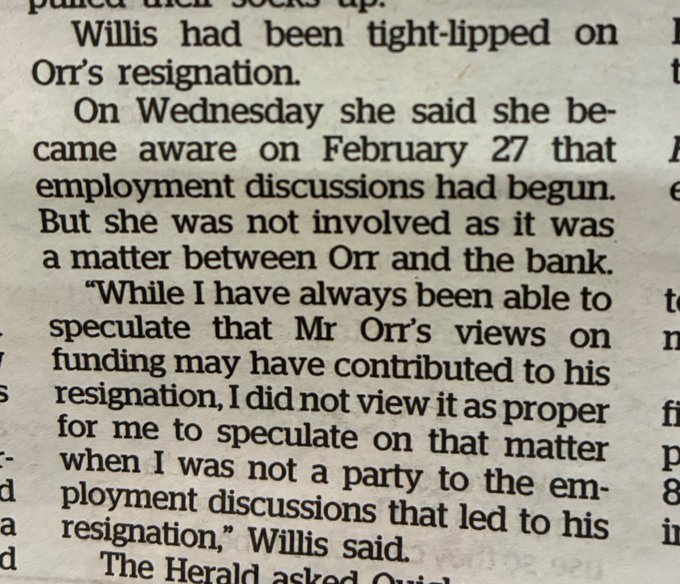

This snippet from an article in yesterday’s Herald caught my eye.

It crystallised something that had been playing on my mind for a while.

The Minister of Finance here seems to be saying that she did not know (at the time) why one of the most powerful officials in New Zealand, chief executive of a major agency in her portfolio, was resigning. The implication is that she never asked and was never told. If so, it would be quite extraordinary, and doesn’t seem at all likely. Decent answers to OIA requests might shed some light, but as I noted yesterday the Bank has so far simply ignored that part of my OIA request relating to communications with the Minister or her office.

The Minister has fairly consistently attempted to suggest that they were all matters only between the Board and the Governor. The Minister appoints the Governor, and while she does not set the terms and conditions of employment (the Remuneration Authority sets the salary and the Board the rest), the Act is quite clear about how a Governor resigns.

The Governor’s resignation is submitted to the Minister and is effective not before she receives it (the Bank gets a copy for information, and I guess to give effect).

Are we seriously expected to believe that the Minister of Finance was so little curious that she never enquired why, or what was going on, either when Iain Rennie first told her this was a possibility (earlier stories say this was 27 Feb, the day of the Bank’s Board meeting referred to in this week’s statement) or at any point in the following few days?

And if, as we are now told, Quigley (for the Board) went off and negotiated an exit agreement with Orr, on whose authority was that done? After all, the resignation itself was to the Minister. Wouldn’t an engaged senior minister, for example, have wanted to ensure that if there were any side deals done there were (a) no embarrassing severance payments, and b) no awkward gag restrictions, obstructing the public’s right to know (given that she now emphasises that the public should as far as possible have a right to know, and Quigley now cites the agreement he made with Orr as some sort of obstacle)? Perhaps Willis is a particularly disengaged minister, but….it doesn’t really seem likely, and especially in view of the balls that were in the air at the time (around both the Funding Agreement and bank capital issues). I guess it is just possible that she told her staff to tell Rennie and Quigley that she didn’t want to know anything (it might be politically convenient for her) but that would be a straight-out abdication of responsibility given her responsibility (including to Parliament and public) for this agency.

Put it together with the points I noted yesterday (did she ever object to the Bank setting a Funding- Agreement-blowing budget this time last year?, how did much higher than previous Funding Agreement numbers find their way into official HYEFU fiscal estimates?) and one senses that there are questions that should be asked of the Minister (journalists, Opposition MPs). And quite what was the character and tone of that meeting with her on 24 Feb, attended by Orr, Quigley (and Hawkesby and Treasury officials)?

I am left beginning to wonder quite what the balance was between Orr choosing to go and Orr being pushed. This seems to have come to a head between the meeting with Willis on the 24th and the Board meeting on the 27th. Orr had clearly engaged in something like an emotional over-reaction to coming funding cuts (“the matter was distressing for Mr Orr”). But why was there a need for an exit agreement if he was simply resigning entirely of his own volition (maybe with the exception of a one line agreement to waive notice requirements in his contract)? And why has the Bank deliberately – and it must have been deliberate – withheld anything about board engagement with the Governor or deliberations on his behavior, stance on funding, future etc?

They are questions not conclusions, but situation seems nowhere near as clear as the Bank might have liked us to believe with their press release (and was it a management position or one formally adopted/approved by the Board?) the other day.

As evidence, too, that the Minister had been part of the effort to mislead the public, I found this in a 5 March (day of the resignation) newspaper article

She too seemed to feed the line of “nothing much to see here”, while suggesting (contrary to the Act, see above) that the resignation was nothing to do with her, even though his resignation had been submitted to her.

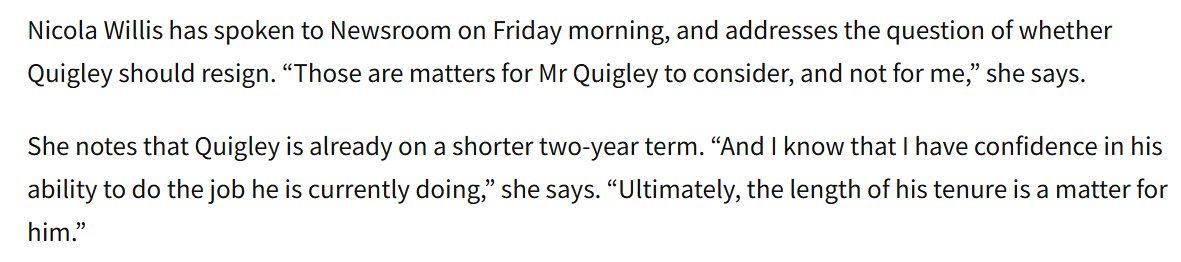

Coming forward, there were some comments reported from Willis in the Newsroom article yesterday on the position of the Board chair.

Hardly a ringing vote of confidence. More reminiscent of those old movies in which some officer’s conduct has disgraced the regiment and he is given a pistol and a bottle of whiskey and expected to do the decent thing.

Quigley

Jonathan Milne of Newsroom has an extensive article on Quigley, including reporting some of his conversation with Quigley on Thursday afternoon. The article still appears to be paywalled (usually Newsroom lifts the restriction after a day, so perhaps it will be freely available shortly) and so I won’t quote extensively from it.

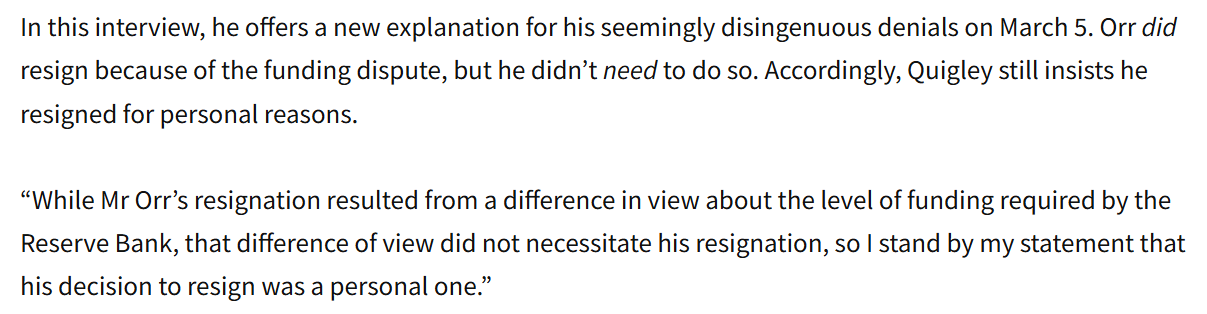

There are two sets of comments worth highlighting though. First, Quigley attempts to somewhat walk back his previous dismissive comments (to Dan Brunskill of interest.co.nz) and to justify his approach on 5 March (although not – not clear if it was asked – the three month wait for eventual partial answers). Little of it is at all convincing (and, for example, he never explains why he agreed to gagging restrictions he claims existed), but this was the most incredible (hard to take seriously) bit

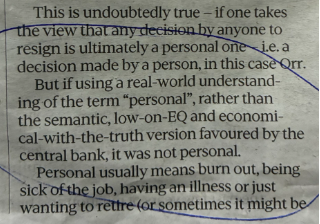

It brings to mind that excellent encapsulation of the point by Luke Malpass in Thursday’s Post

No one, but no one, thinks that a resignation over a major dispute with Board/Minister, involving conclusions that future working relationships would be deeply impaired (presumably because of Orr’s conduct), is what would reasonably be described as “personal” reasons. Except, it seems, Quigley.

He actively misled us.

The second set relates to the question of what gagging restrictions still do (or don’t) exist.

If there is genuine uncertainty (Milne seems to contacted Orr himself) it should be resolved now, and clarified (waiving previous gag provisions if necesssary) in favour of transparency and accountability (and, at this point, it is less about accountability for Orr, but of the Board (specifically its chair) and the Minister. Among other questions, how was this departure so badly handled? (And recall that Orr was planning to turn up at the conference the next day and discuss the news, suggesting any gagging may primarily have come from the Board chair, with the acquiescence (at least) of the Minister. But we don’t know.)

The MPC blackball

(As noted above, this is mostly for the record. There is little new material beyond this point.)

In his article, Milne includes this

This is a characterisation I object to fairly strongly, having provided chapter and verse (including through Reserve Bank documents, and reported interviews with the person who was Reserve Bank chief economist at the time and with the person who was Grant Robertson’s adviser at the time) over several years. And from the first hand account of an academic who in any sane system would have been seriously considered but who was explicitly blackballed.

There are two separate parts to this episode though, both extensively dealt with and documented here:

- the first related to decisions taken by the Board in 2018 about what sort of people to exclude from consideration for appointment to the new MPC (the Board recommends, the Minister decides)

- the second related to Quigley actively misleading Treasury, and in the process the public, in 2023 by claiming that there was no such restriction.

Of these, the first is indisputable and to almost all serious outsiders quite extraordinary. As one of my former colleagues reminded me recently, it was a standard so absurd that if applied anywhere else in the world people like Ben Bernanke and Janet Yellen would have been disqualified from appointment (both served on the board of governors before later becoming Fed chair).

As I have noted in repeated posts, my knowledge of this blackball never relied on “a Treasury statement”, although the published Treasury statement provided an external hook to hang concerns on. I had been told months earlier by an academic (see above) that he’d been blackballed. I have never named this person (at their request) and have sought to rely on published material, but this was the relevant section of said academic’s email to me in 2023 when the whole issue came to the fore again.

In addition to published comments from John McDermott and Craig Renney, the post I linked to above has extracts from OIA releases setting out the Board’s position that researchers (in macro/monetary fields) should, pretty much automatically, be considered as conflicted and thus ruled out of consideration. The claim that this was about “conflict of interest” was simply absurd (as the academic notes in the email, in light of abundant overseas precedent (not just in the UK but, eg, in Sweden and the US), and any potential issues readily dealt with through the MPC Code of Conduct).

But absurd as the 2018 policy and practice was, I guess it was a lawful (ie legally open to the Board) choice. And had the Minister at the time strongly objected, I guess he could have pushed back and insisted that the field for consideration include active researchers in macro-type fields. That it is what actually happened was confirmed to the Herald in 2023 by Chris Eichbaum (one of those Milne talked to, former Board member in 2018/19) who confirmed that the blackball had been in place. Eichbaum defends the approach, but does not dispute that it was the policy/practice then: experts were explicitly excluded (consistent with the academic above’s account).

Eichbaum got involved again because earlier in 2023 Quigley had on two separate occasions denied to The Treasury that there had ever been such a blackball, suggesting that a Treasury official (who had since left, and could conveniently be thrown under a bus) had simply gotten the wrong end of the stick and had misadvised the Minister. In the context of questions around whether the blackball was still in place by 2023 this (very ill-advisedly) led Treasury to make a public statement denying that there even had been such a restriction, and tossing their own former employee under a bus. This is all documented, in painstaking detail, in the link above (including the email recounting the views of one Treasury Deputy Secretary (now leaving) suggesting that perhaps there really hadn’t been an error (on the Treasury side of the street)).

Eichbaum then talked to the Herald (and later confirmed that he was happy with how his views were reported), saying in effect “I don’t know what Neil thought he was doing. Why didn’t he just say, yes we had a ban then, but we don’t now”. Indeed. There wasn’t a ban in 2023, and a respected macro academic (Prasanna Gai) was appointed last year to the MPC.

At the time (2023) I was half-inclined to make excuses for Quigley (busy man, demanding day job, several years ago, perhaps he really had forgotten). It wasn’t a very persuasive story but I didn’t really want to believe that such a high office holder would actively mislead Treasury (not just once), never even clarifying things after the Treasury statement went out and there was pushback (including here). But events of the last couple of months suggest that when it comes to the Bank, Quigley seems to have been willing to say almost anything, with a close alignment with the truth not apparently being a prerequisite.

I’ve included all this here partly because I am a little annoyed at how Milne treated the issue (granting that he had huge amounts of material, and when I finished talking to him at 8pm on Thursday he was about to start turning it into a story before 5am), but more importantly because I think what this episode – in the 2018/19 and 2023 parts – demonstrates is that Quigley had long since proved himself unfit to be chair of our central bank’s board. The last three months (last week too) have been a debacle, coming on top of (eg) the egregious budget setting last June, all of which proved the point again, but the latest actively misleading shambles does not exactly come after years and years of previously spotless service as Board chair.