It was in mid-August that this particular bit of shameless Reserve Bank spin got going. From a post in late August

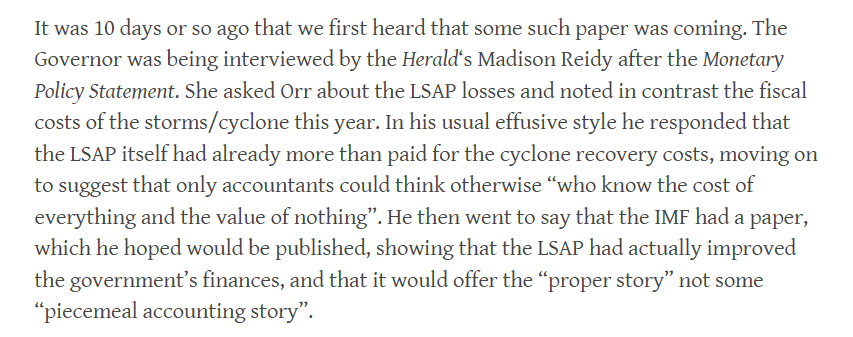

It proved to be nonsense of course. Once we had access to the short little IMF piece, published at the back of the Fund’s Article IV review, it was clear that it all amounted to a case of “if you assume big beneficial economic effects from the LSAP, then you get material tax revenue gains”, which might be set against the actual losses on the trade.

But the IMF’s picture bore not the slightest relationship to New Zealand reality through the LSAP period.

But none of that stops the Bank.

Here was their Annual Report, which will have been signed off by the Bank’s Board – the ones with little or no subject expertise.

And then this week their deputy chief executive responsible for monetary policy and markets – the one with no subject expertise at all – was at it in a speech given to investors etc in Sydney.

Now I have not seen any analyst endorse that little IMF exercise. And you can sort of tell that even the Bank knows it is shonky (but convenient). Note that both in the Annual Report and Silk’s speech they are careful not themselves to claim that the LSAP was profitable for the taxpayer, just to report (what is factually accurate) that the IMF – or at least a couple of back office researchers, given a couple of hours to play with a toy model – said it was. Silk herself only claims that the losses (they aren’t just “accounting losses” but real ones for taxpayers) are offset “to some extent” by other fiscal benefits to the Crown (and there might be even some very slight extent to which that is so, but it is by no means guaranteed). And the Annual Report text takes a similar approach – citing the IMF, without actually endorsing its work, but leading the casual reader to assume they did. The Bank knows better and simply choose egregious spin – the sort of dishonesty we might have got used to from politicians, but shouldn’t have to put up with from independent technocrats.

But here we are dealing with Quigley and Orr, who know better but seem to have a tenuous relationship with truth and serious analysis whenever something otherwise suits. And Silk, who may know no better – but can surely read, if she were at all curious – who is the senior manager with overall responsibility for the Bank’s macro and monetary policy analysis.

None of them should be in their roles (Silk should simply never have been appointed to hers). But will the new government care enough to do anything about this situation, or will spin and dishonesty continue to characterise our central bank, while those with the power to do anything about the situation get on with simply holding office?

The LSAP is related to the RBNZ buying NZ Govt Bonds. If Treasury had bought back the bonds and cancelled them, we’d be in the same position (financially as a country) although I’m not sure we’d be discussing losses. And these losses are actually that the bonds were bought at market value, which hindsight has shown to be overpriced.

Which got me thinking about 100 year bonds. Even Argentina managed to sell some at the low in yields (when many countries had negative yields, even out to 30 years). But we didn’t and I’d suggest that the failure to do so has cost the country. Possibly more than the LSAP losses detailed in the missive above.

So why aren’t we holding Treasury to the same standards?

LikeLike

Fair comment. If I was defending Treasury (and actually I’m critical of them for endorsing the LSAP and advising MOF accordingly), I’d note that it wouldn’t have made much sense for one arm of the NZ govt to have been selling more really long dated govt bonds even as the RB was buying longdated bonds back.

LikeLike

This isn’t exact, as I’m only focusing on nominal bonds, not bills or ILBs, and the period from the 1st April 2020 to 1st July 2020: over that period the NZDMO issued about NZ$10.55bio of bonds through tenders, whilst the RBNZ bought NZ$17.754bio of bonds. Matching off issuance against QE purchases looks like this

Bond Maturity NZDMO issuance ($m) RBNZ Purchases Net

15-Apr-2023 3,050 1,980 (1,070)

15-Apr-2025 1,850 2,790 941

15-Apr-2027 1,300 2,570 1,270

20-Apr-2029 2,150 2,790 640

14-Apr-2033 800 2,000 1,200

15-Apr-2037 1,400 1,913 513

Total 10,550 14,044 3,494

You can see the from the NZDMO’s website that the Weighted Average Maturity of their liabilities fell over that period due to the short/intermediate issuance, probably driven by domestic bank’s regulatory capital holding requirements.

Now to be fair to the NZDMO, initially they was an initial need to get cash in the door, so this would have been a more efficient way of doing this that trying to syndicate a new ( long dated) bond. Although not quite a revolving door (the RBNZ bought more than was issued by the NZDMO -and this is off course is a requirement for QE to work) it was pretty close.

Why didn’t they issue a 100Year bond? Well, two things: (1) I’ve touched on that above- less cash in the door. (2) the Argentine bond was a US$ bond, and there would have been plenty of US$ based Asset/Liability matchers who would have been happy to look at a 100 year bond ( accepting the credit risk on the asset ) or fund managers who would have liked the duration – same as a 10 year bond with less cash utilized, maybe not the convexity…and definitively not the eventual default…but that’s another story.

The cross currency asset swap market in NZD is almost non existent past 10 years, so that’s a problem for those ALM buyers who would need to swap NZ$ cash flows to US$s. As for the offshore fund managers, contrary to the RBNZ’s stated aim of LSAPs which was to get the offshore fund managers to sell their bonds (leading to a lower the NZD nominal exchange rate), they didn’t (and the NZTWI went up) – those institutions just didn’t buy anymore long dated bonds until late 2021, by which time bond term premia had started to climb back up, changing the attractiveness of those bonds.

In summary, LSAP’s did absolutely nothing via the portfolio channel mechanism to increase NZ inc’s long term issuance profile.

https://www.linkedin.com/posts/john-young-1192a425_jam-charts-activity-7039429882585518081-FLNi?utm_source=share&utm_medium=member_desktop

LikeLike

The goal during COVID was to lower medium-long term interest rates after the OCR had reached 0.25%. The LSAP was simply the method. There has been little discussion as to whether that was the correct method to achieve the goal. My argument is that LSAP was not required. Market forces would have carried NZ rates down in an environment where European rates were negative, US 10-year rate was 0.50%, Australian 3-year rate was 0.1%. The RBNZ should have just stood on the sidelines, perhaps with a minor kick along every now and then (certainly not a $50 billion kick….)

LikeLike

While I largely agree, I think the RB would argue that even if the LSAP made little difference to long term rates it may have delivered them at a lower exchange rate than otherwise,

LikeLike

But wasn’t the lower exchange rate caused by lower bond rates? If so, the lower bond rates could have been achieved without LSAP (by relying on global forces to do the heavy lifting, given the long-standing high correlation between US and NZ bond rates……)

LikeLike

The Bank nonetheless do argue for a material exch rate effect. The argument would run along these lines: had we not done LSAPS and other countries had, our bond rates would still have come down at the margin the additional (foreign) buying to narrow the spreads fully would have tended to raise the exchange rate. Like all their arguments in this area, there is probably a little bit too it, but not much. They massively overclaim the effects (I guess to attempt to justify the scale of the financial risk they took).

LikeLike

A supposed quote by Herr Goebbels, whilst probably not actually made by him, nonetheless captures perfectly the rationale for Mr. Orr’s consistent lying, and indeed explains the current neo-Marxist zeitgeist in “Aotearoa.”

“If you tell a lie big enough and keep repeating it, people will eventually come to believe it. The lie can be maintained only for such time as the State can shield the people from the political, economic and/or military consequences of the lie. It thus becomes vitally important for the State to use all of its powers to repress dissent, for the truth is the mortal enemy of the lie, and thus by extension, the truth is the greatest enemy of the State.”

The previous government incompetently spent up more than any other in history. They received value-for-money for just one area. For the cost of a comparative paltry amount of $125mn per year (over half a billion in total over six years), they bought “advertising” from the media, which was essentially the buying of fawning State propaganda. These bribes were supplemented with further millions from the PIJF. Over 90% of the mainstream media are neo-Marxist fanatics or “useful idiots”, as Lenin was alleged to call these clueless leftist collaborators. Propaganda for the Covid Cult, the Climate Cult, and various other Ponzi’s enabled looting, mooching and grifting on a truly unprecedented scale.

Mr. Orr is the poster boy for neo-Marxist grifting, looting and mooching. He enabled the Covid Cult, which resulted in New Zealand having the worst response to the pandemic in the Western world.

However, the fact that Mr. Orr has been grossly incompetent is the least of the crimes he has committed over his tenure. Prancing around the world babbling about the Climate Cult, when he has abjectly failed in his core job to tame inflation for years, was negligent and annoying, but no where near his worst failure.

You might forgive a public official for their incompetence, if they are at least honest.

Mr. Orr, in my view, has shown himself time and time again to be deeply dishonest. Doubling down on the lie that his $12bn of losses printing money increased GDP, when there was little or no output gap, is unforgivable in my mind. I expect an apology. Or I want my money back. This is $2,400 losses for every man, woman and child in the country.

Is there hope? I suspect that MMP is now working as it should be. The minor parties are finally getting a say in how the country should be run. This could be bad news for Mr. Orr.

In my opinion, Mr. Seymour desperately needs to make an example of some of the egregious looters, moochers and grifters from the neo-Marxist period. As Adam Smith in the Wealth of Nations argues, incentives are the reason why market economics works. The new government need to show the fanatical left that we are moving to a new age of accountability and responsibility. The best signal I can think of for achieving this change in approach would be to unceremoniously fire Mr. Orr.

Hopefully Mr. Seymour adds this requirement to the coalition agreement.

LikeLike

hmmmm……I wouldn’t call Adrian Orr “grossly incompetent” because he knows exactly what he’s doing i.e. trying to pull the wool over our eyes after the LSAP lumbered taxpayers with a massive loss. As for the LSAP pulling down the exchange rate, history shows that, to the extent interest rate differentials have an impact, it is the differential at the short end that counts. I think it’s grasping at straws to suggest activity in the long end of the curve had much effect. Besides, history also suggests the Kiwi is more susceptible to “risk on/risk off” considerations than rate differentials when they are small. And it was undoubtedly “risk off” during the COVID period.

LikeLike