Three months ago I wrote a short post here using some new data the Reserve Bank had started to publish on the monthly payments Treasury was making to the Reserve Bank as the losses were gradually realised on the huge portfolio of bonds the Bank and MPC had run up in 2020 and 2021 (the LSAP). It was to the Bank’s credit that they have started making the data available, and although there have been a few glitches since then, when I have got in touch they have been very helpful.

I can remember the days when I and a few others used to jeer at them for having lost $7 billion (and these numbers are a proxy – albeit an imperfect one – for big and very real losses for the taxpayer from the asset swap programme, executed at probably the single most inopportune time since interest rates were liberalised 40 years ago). Last year, the Taxpayers’ Union gave the Governor a lifetime achievement award for waste, citing then estimates of $8.5 billion of losses.

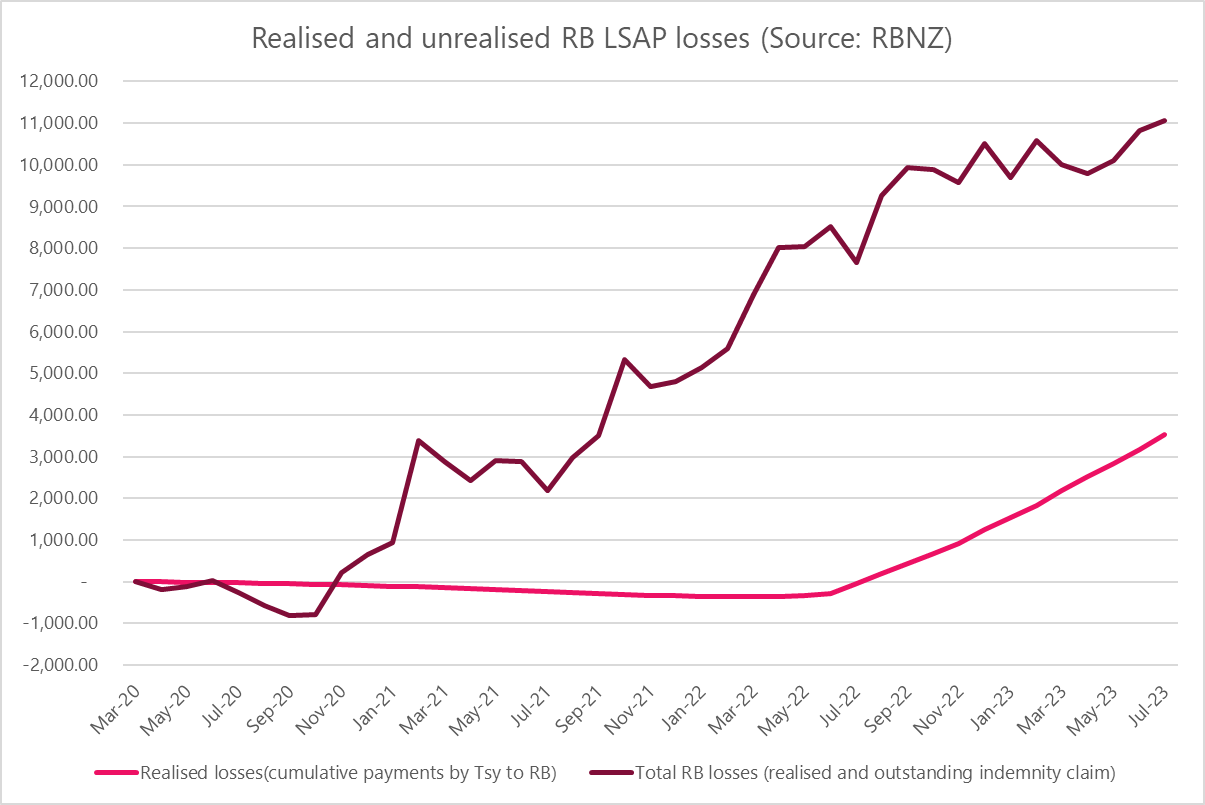

That was then. When I ran the first post in May total RB losses (now properly measured, with the indemnity payment data) had been bobbling just either side of $10 billion. With today’s update by the Bank of the relevant spreadsheet, here is the position to the end of July.

Yes, total RB losses from this grossly overblown under-analysed programme have now reached $11 billion (which was also the last total estimate from The Treasury I’d seen).

But, again, that was then, and in August to date bond yields appear to have risen another 20 basis points or so. As the portfolio slowly shrinks and the longest bonds are sold off first, the extent of further losses should diminish, but there is no sign we’ve yet reached the limit.

I’ve tended to focus in on the Governor as responsible, and there is little doubt that he is the dominant figure on the MPC.

But we shouldn’t forget the other internal MPC members who shared in the decisions to accumulate the risk:

Then Deputy Governor, Geoff Bascand

Then Assistant (now Deputy) Governor, Christian Hawkesby

Then Chief Economist, Yuong Ha

One has since been promoted and two have moved on, although with no hint that sharing responsibility for absolutely huge taxpayer losses was a part of either move.

More recently, Karen Silk and Paul Conway have joined the MPC. They weren’t there when the risk was taken on, but they have been part of the decision not to close it out quickly, and thus to continue to expose taxpayers to further losses.

And then of course, there are the three externals, all reappointed since the LSAP folly: Bob Buckle, Peter Harris, and Caroline Saunders.

And who reappointed them and Orr? Well, that would be the Minister of Finance and the Bank’s Board, the latter chaired by Neil Quigley, who has just proved you can apparently just make up stuff to Treasury, lead Treasury to lie to the press, and still carry right on as chair of a government board. In this country new depths of poor governance seem to be plumbed almost every week.

Finally, we shouldn’t completely exclude the Secretary to the Treasury from responsibility. She sits as a non-voting member of the MPC and she advises the Minister on things like indemnities and Bank performance. There is not even a hint (eg in the MPC minutes or OIAed papers) that she has ever dissented from the highly risky and costly LSAP intervention.

That is quite a list of people who share responsibility for losses that have now reached $2000 per man, woman and child in this country. Readers will reflect on just what nice-to-haves that politicians are now competing to bribe us with (with borrowed money) might have been considerably more affordable had the Bank stuck to the OCR which, boring as it may be, tends not to make or lose taxpayers much money at all.

I suppose one way of looking at that list of the responsible men and women is that if we averaged it out, the loss was a bit under $1 billion per responsible public figure. There wasn’t even a good party (as Mr Leauanae enjoyed on leaving MPP) just reckless waste and losses on a scale not seen in New Zealand public finances for a very long time.

And no one paid any personal price. There was no personal accountability at all. Most of these people still hold their high, and highly paid, offices. While you and I are covering the losses they so carelessly racked up. It is some slim consolation that one of them is up for election in a few weeks.

It’s a back of the envelope calculation, but if the RBNZ had used Yield Curve Control (YCC) at the outset as a reinforcement to their time dependent forward guidance and bought every outstanding bond of the NZGB April 2023 & May 2024 issues( total NZ$29.345bio)at the policy rate of 25bps*, to date that would have cost the Crown about NZ$816mio in interest payments.

Granted, research by the NY Fed demonstrated that the RBA’s YCC impact outside of the three year targeted bond was limited**, but given the structure of NZ’s Capital Market apart from the signalling channel the other transmission channels of QE were probably very constrained.

Arguably NZ QE did little to alleviate any domestic market dysfunction in March/Early April 2020, and potentially exacerbated government bond market fragilities later on:

https://www.linkedin.com/posts/john-young-1192a425_warning-only-if-youre-interested-in-esoteric-activity-7033999851960885248-BRiO?utm_source=share&utm_medium=member_desktop

*As part of the LSAP programme NZ$7.471bio of the NZGB 2023 were purchased at a weighted average yield of 20.3bps and NZ$5.13bio of the NZGB 2024 were purchased at a Weighted Average Yield of 28.9bps.

** https://www.newyorkfed.org/research/staff_reports/sr1013

LikeLike

Did you see the film currently/recently showing in the film festival, “Billion Dollar Heist”, about the central back of Bangladesh being targeted in a $1b attempted cyber attack, (and actually loosing $100m or so IIRC)?. The bank was potentially exposed to the risk of the $1b loss for a couple of days after it was first detected at the bank. It wasn’t stated, but that exposure is potentially why the central bank governor lost his job.

From my experience in IT, the film has some small inaccuracies and hype (I guess typical for that medium). But overall a nice overview of cyber crime.

Perhaps Bangladesh loosing US$1b is more impactful than NZ loosing NZ$11b. Probably cyber crime is more film-worthy than a bank choosing the wrong monetary policy instruments. But I think the 11b issue would also make a good film. (A film by the publicly subsidized NZ film industry of course. 🙂

LikeLike

The film is worthwhile for people to see I would say, and I’d be interested in comments from anyone else who has seen it.

LikeLike

Yes I did see, and had much the same reactions. Even as a poor country, Bangladesh’s total GDP is about 50% higher than NZ’s, and of course the actual loss there was “only” USD$81m. Realistically, the Bangladesh Governor was a scapegoat (reasonably enough someone had to pay a price, but he was a very highly regarded figure), but in NZ even with direct responsibility sheeting home to the Governor there is no responsibility at all.

As my wife said of the film, it could as easily just have been a podcast (the visuals were limited and didn’t add a lot), and prob the same could be said for the LSAP challenges. The challenge – which the film makers met pretty well – is translating what happened, and what it means, into terms that make sense to the intelligent layperson.

LikeLike

Well written ,but highly concerning. Go through the Ranks of the admin people involved,and don’t be surprised that not ONE of them has run a personal business of means. Our present govt. admin appears to be brimming with non-accountable but highly paid Infrastructure that were never ever briefed on RISK Recognition. Just WHO will take over when there is nothing left ? Will they just “Dum-de-doo” walk away ? I don’t expect a serious reply.

LikeLike