Late yesterday afternoon the Minister of Finance issued a new Remit to the Reserve Bank Monetary Policy Committee (his statement is here, the new Remit itself is here). The Minister’s statement tends to minimise the entire thing (and nothing really about the inflation target changes), but – no doubt consciously and deliberately – gives not a mention to the most material addition to the Remit.

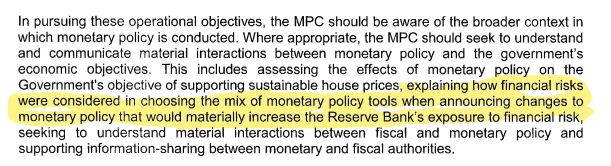

The lead-in to the more-specific targets section of the Remit is now as follows:

This was the backdrop to the additional words I’ve highlighted

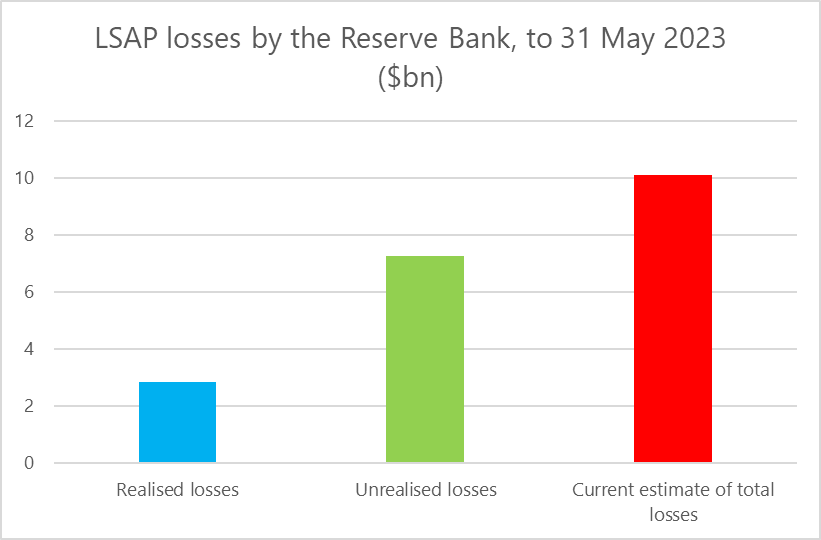

$10 billion of so of losses of taxpayers’ money as a result of Reserve Bank MPC choices around the LSAP programme, choices that had the imprimatur of the Minister of Finance (and apparently no objection from the Treasury). As the bonds are being sold back to The Treasury, the realised component of the losses is mounting significantly each month ($317m in indemnity payments were made to the Bank last month), but total estimated losses hang fairly steadily around $10 billion.

The addition to the Remit is welcome. Formally, it doesn’t bind the MPC to anything much (note that “where appropriate” at the start of the second sentence, which appears to conditions things in the third sentence too) but will add put pressure to a) do some advance analysis and b) disclose their thinking and analysis when next the MPC is tempted to throw caution to the wind and take huge risky punts in the financial markets (conventional monetary policy, by contrast, poses very little financial risk to the taxpayer). In 2020 there is no sign they ever did the risk analysis, they certainly never shared anything substantive with the public, they just took the plunge, and over the following months got the Minister to agree to up their gambling limit, still with no serious risk analysis, and no disclosure.

But think what it cost the taxpayer – you and me – to get here: it really is the $10 billion amendment.

MPC members have never made a serious attempt to defend either the alarmingly poor process or the wildy costly financial outcomes. The Governor has waved his hands and blustered about the (wider economic) gains being “multiples” of the losses, but has produced no serious analysis to support such claims (and in the unlikely event there was such a boost to aggregate demand, that would mean the LSAP programme had directly contributed to the high inflation looming recession mess we are in now), while the external MPC members have never said anything about anything they’ve been responsible for. And yet, having simply thrown away $10bn, on no good process or analysis, each of Orr and the three externals have been reappointed by…….Robertson, the man who signed off on the indemnity, not having himself demanded serious supporting analysis from the MPC or The Treasury.

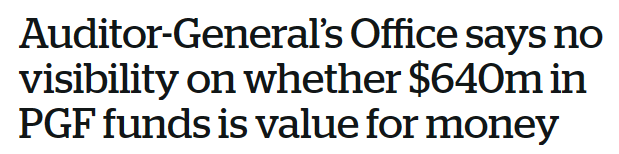

There was an article in the Herald the other day about the Auditor-General having reviewed aspects of that great Labour/New Zealand First boondoggle, the Provincial Growth Fund. This was the headline

The LSAP involved multiples of the amounts involved in the PGF, clear and documented losses, and no serious attempt to show whether there were any benefits at all. $10 billion is a lot of money. It would seem an obvious case for the Auditor-General to look into, given that none of those we should rely on as first line of defence (RB Board, Treasury, Minister of Finance, FEC) seem at all interested. Much easier to file it under experience, avoid even any serious expression of contrition (whether for these losses or the inflation debacle), reappoint all those involved, and just throw out bone with a slight (if welcome) amendment to the Remit.

[…] Michael Reddell, a fellow with an admirable track record as a blogger with expertise in this sort of thing, has posted his analysis under the heading The $10bn amendment. […]

LikeLike

Has this been released as a press release to media outlets especially independent ones like interest.co.nz and The Platform?

LikeLike

My blog tends to be read by many of the people writing for mainstream media on central banking and econ topics

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

I have read a number of these blog posts about the apparent losses from doing Q.E., or whatever you want to call it. I also know you will say that outsiders don’t know enough about the topic. But what I object to firstly is your continued claim that “taxpayers money” has been lost. If the public debt was bought with new cash, or what is misleadingly called printing money, it was not bought from tax funds, i.e. as part of a Budget appropriation. It is therefore not possible to lose a form of public money that was not (literally) used in the first place. You will no doubt say that I don’t understand the indemnity or whatever. The second part of this turns on your view that the bonds were issued into the debt market, and should return there to complete the operation. That might be an argument if RBNZ had bought corporate bonds. But they didn’t. And the operation surely saves a lot of interest payments going out of the public accounts. Ultimately the problem seems to be that RBNZ is not constitutionally independent if it remains owned by the State. I agree that there all sorts of accountability issues, but it is still misleading to say that the ‘taxpayer’ has taken a loss, when this is not logically possible, given that the subsequent transfers are within the public accounts.

LikeLike

The taxpayer has sustained a very substantial loss (not exactly the same as the RB losses reported in this post and my chart) but very substantial nonetheless. The loss arises because the RB’s action in effect swapped long-term fixed rate govt debt held by private participants for an equivalent amount of floating rate liabilities held by the private sector (settlement cash balances held by banks), It did this just at the bottom of the interest rate cycle, and is now – in effect – paying 5.5 per cent on deposits that arose from purchasing back bonds yielding about 1 per cent.

LikeLike

I don’t think the point of the interest cycle matters. If the long bond was correctly priced then it will have anticipated all the upcoming increases in floating rates. So the loss (or gain) on the transaction will be due to actual experience being different to what the market priced. Noting, of course, that all normal Treasury issues are subject to market experience in the same way as was this transaction.

LikeLike

We should add in the inflationary effect of these RB action as well

Inflation @ <7% is having a huge effect on the tradeable economy , and in fact is much higher for some individual parts of that economy.

Savings are not doing well either.

This Government is largely to blame with its profligate spending, which shows little sign of abating.

Will the RB continue with OCR increases as mandated?

Would the Government allow them to anyway?

It is election year, so any change is most unlikely!

LikeLike

Reading between the lines it seems the Stupidly incompetent was advising the incompetently stupid, you choose which was which.

LikeLike

“I don’t think the point of the interest cycle matters. If the long bond was correctly priced then it will have anticipated all the upcoming increases in floating rates”….actually it matters a lot from a risk perspective because when a long dated fixed rate interest rate asset is transformed into a floating-rate one when interest rates are low then there is a higher probability that the expectation component of a bond’s price doesn’t hold.

Central Banks who under took QE ( i.e did a fixed to floating swap) post the GFC did so when nominal bond yields were higher, and were able to post positive flows to the Government Treasury. Post Covid, and with short-term policy rates moving higher, to combat inflation, this position has now reversed quite significantly and those same central banks who undertook further QE at lower interest rates are either not making such remittances or now receiving funds from their Treasury.

LikeLike

Thanks for that comment John. I agree, and had meant to make similar points in response to Brigitte. Another example is large doses of fx intervention: at any point a random walk is probably the least-bad near term guide to the future exch rate (and all existing info is already priced) but the fact of the intervention opens up a risky position (deliberately) which could go for the taxpayer or against.

LikeLike