Late yesterday afternoon the Minister of Finance issued a new Remit to the Reserve Bank Monetary Policy Committee (his statement is here, the new Remit itself is here). The Minister’s statement tends to minimise the entire thing (and nothing really about the inflation target changes), but – no doubt consciously and deliberately – gives not a mention to the most material addition to the Remit.

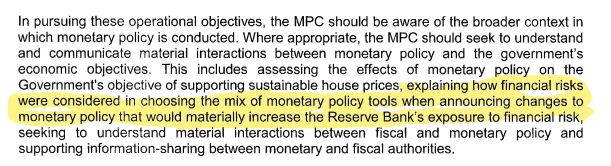

The lead-in to the more-specific targets section of the Remit is now as follows:

This was the backdrop to the additional words I’ve highlighted

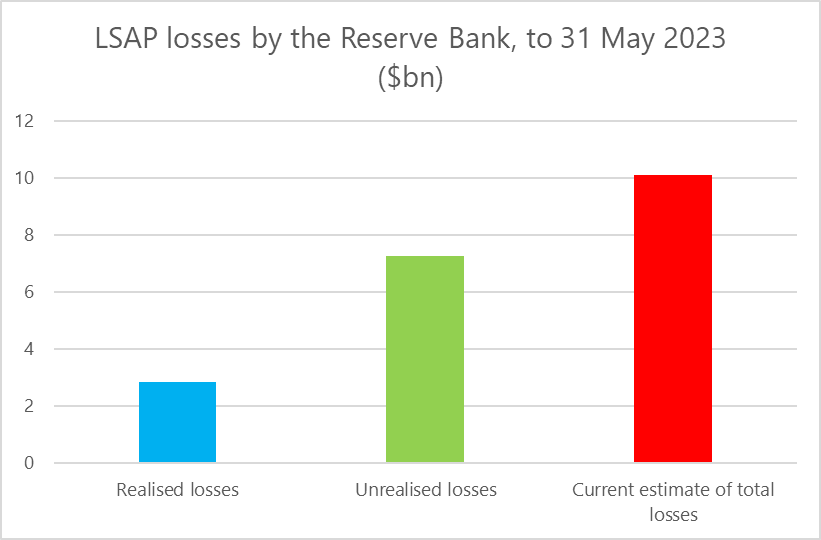

$10 billion of so of losses of taxpayers’ money as a result of Reserve Bank MPC choices around the LSAP programme, choices that had the imprimatur of the Minister of Finance (and apparently no objection from the Treasury). As the bonds are being sold back to The Treasury, the realised component of the losses is mounting significantly each month ($317m in indemnity payments were made to the Bank last month), but total estimated losses hang fairly steadily around $10 billion.

The addition to the Remit is welcome. Formally, it doesn’t bind the MPC to anything much (note that “where appropriate” at the start of the second sentence, which appears to conditions things in the third sentence too) but will add put pressure to a) do some advance analysis and b) disclose their thinking and analysis when next the MPC is tempted to throw caution to the wind and take huge risky punts in the financial markets (conventional monetary policy, by contrast, poses very little financial risk to the taxpayer). In 2020 there is no sign they ever did the risk analysis, they certainly never shared anything substantive with the public, they just took the plunge, and over the following months got the Minister to agree to up their gambling limit, still with no serious risk analysis, and no disclosure.

But think what it cost the taxpayer – you and me – to get here: it really is the $10 billion amendment.

MPC members have never made a serious attempt to defend either the alarmingly poor process or the wildy costly financial outcomes. The Governor has waved his hands and blustered about the (wider economic) gains being “multiples” of the losses, but has produced no serious analysis to support such claims (and in the unlikely event there was such a boost to aggregate demand, that would mean the LSAP programme had directly contributed to the high inflation looming recession mess we are in now), while the external MPC members have never said anything about anything they’ve been responsible for. And yet, having simply thrown away $10bn, on no good process or analysis, each of Orr and the three externals have been reappointed by…….Robertson, the man who signed off on the indemnity, not having himself demanded serious supporting analysis from the MPC or The Treasury.

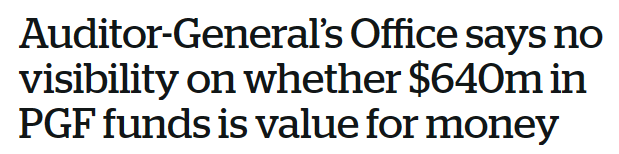

There was an article in the Herald the other day about the Auditor-General having reviewed aspects of that great Labour/New Zealand First boondoggle, the Provincial Growth Fund. This was the headline

The LSAP involved multiples of the amounts involved in the PGF, clear and documented losses, and no serious attempt to show whether there were any benefits at all. $10 billion is a lot of money. It would seem an obvious case for the Auditor-General to look into, given that none of those we should rely on as first line of defence (RB Board, Treasury, Minister of Finance, FEC) seem at all interested. Much easier to file it under experience, avoid even any serious expression of contrition (whether for these losses or the inflation debacle), reappoint all those involved, and just throw out bone with a slight (if welcome) amendment to the Remit.