Just a few things caught my eye flicking through yesterday’s HYEFU summary tables – if you don’t count points like the fact that The Treasury projects we will have had five successive years of operating deficits (in a period of a high terms of trade and an overheated economy), and that net debt as a per cent of GDP (even excluding NZSF) is still increasing, notwithstanding the big inflation surprise the government has benefited (materially) from.

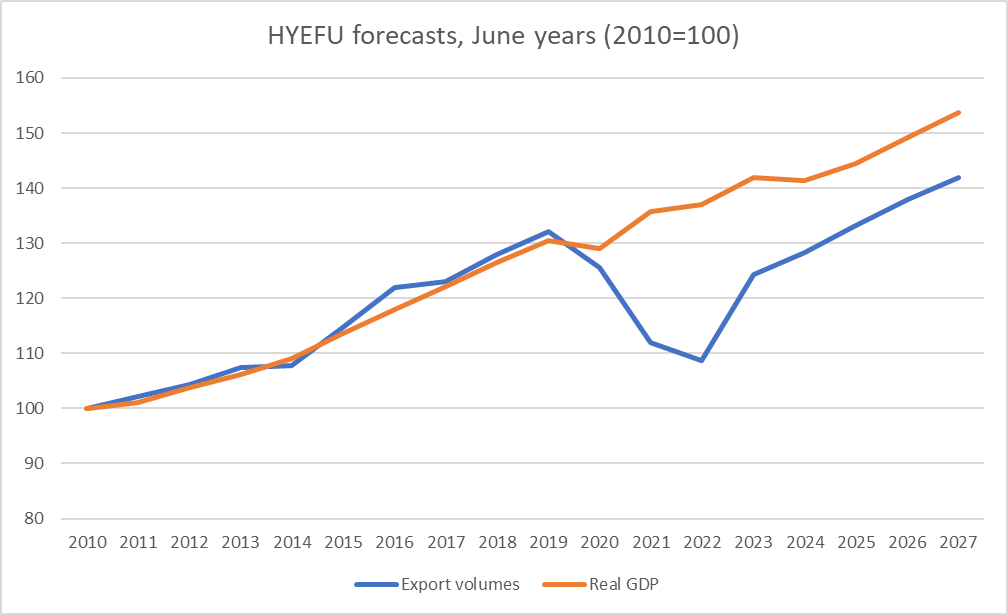

This chart captures one of the things that surprised me. It shows export volumes and real GDP, actual and Treasury projections. Exports dipped sharply over the Covid period (closed borders and all that), but even by the year to June 2027 Treasury does not expect export volumes to have returned either to the pre-Covid trend, or to the relationship with real GDP growth that had prevailed over the pre-Covid decade.

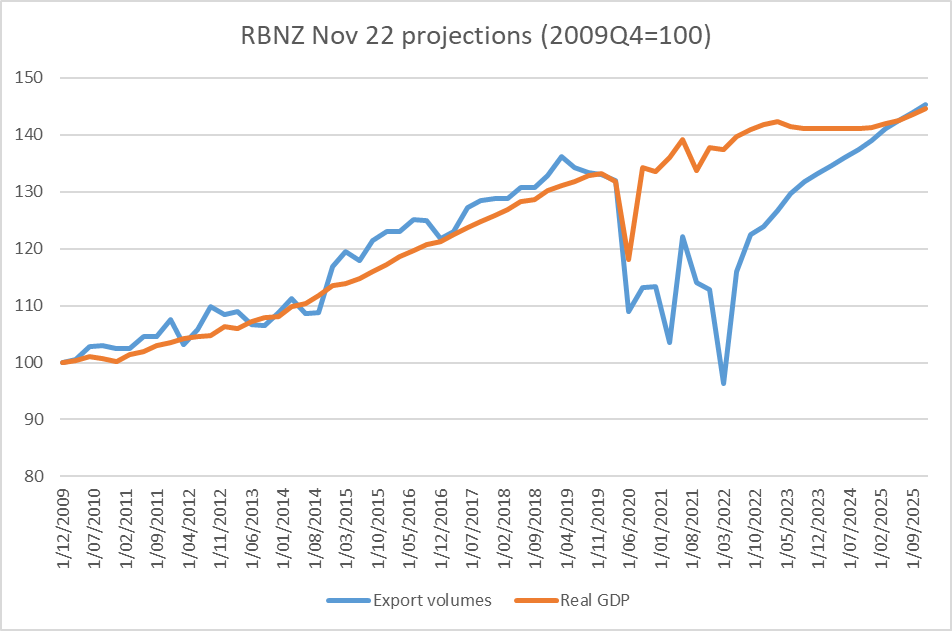

The Reserve Bank does not forecast as far ahead as the Treasury but has quarterly projections for these two variables out to the end of 2025. Here is a chart of their most recent projections

It is a quite dramatically different story.

The issue is here is not so much who is right – given the vagaries of medium-term macro forecasting there is a fair chance that none of those four lines will end up closely resembling reality – as that the government’s principal macroeconomic advisers (The Treasury) have such a gloomy view on the outward orientation of the New Zealand economy. One of the hallmarks of successful economies, and especially small ones, tends to be a growing number of firms footing it successfully in the world market. Earnings from abroad, after all, underpin over time our ability to consume what the rest of the world has to offer. Quite why The Treasury is that pessimistic isn’t clear from their documents – one could guess at various possibilities in aspects of government economic policy – but it does tend to stand rather at odds with the puffery and empty rhetoric the PM and Minister of Trade are given to.

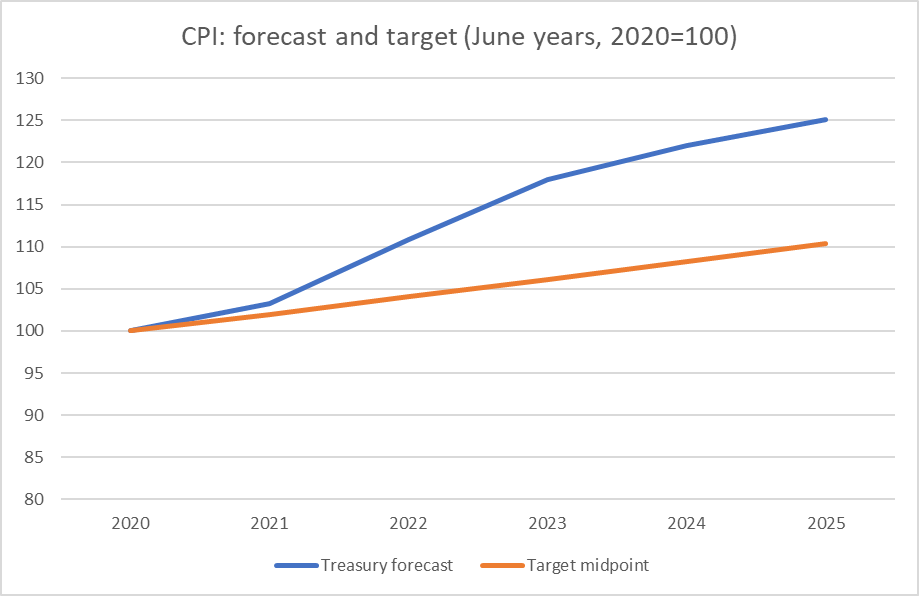

Then there was this

On Treasury forecasts the CPI in 2025 will have been 13.3 per cent higher than if the Reserve Bank had simply done its core job and delivered inflation on average at 2 per cent per annum (the Reserve Bank’s own projections are very similar). It is a staggering policy failure – especially when you recall that the Governor used to insist that public inflation expectations were securely anchored at around 2 per cent. It is an entirely arbitrary redistribution of wealth that no one voted one, few seem to comment on, and no one seems to be held to account for, even though avoiding such arbitrary redistributions (benefiting the indebted at the expense of depositors and bondholders) was a core element of the Reserve Bank’s job. We don’t – and probably shouldn’t – run price level targets, but let’s not lose sight of what policy failures of this order actually mean to individuals.

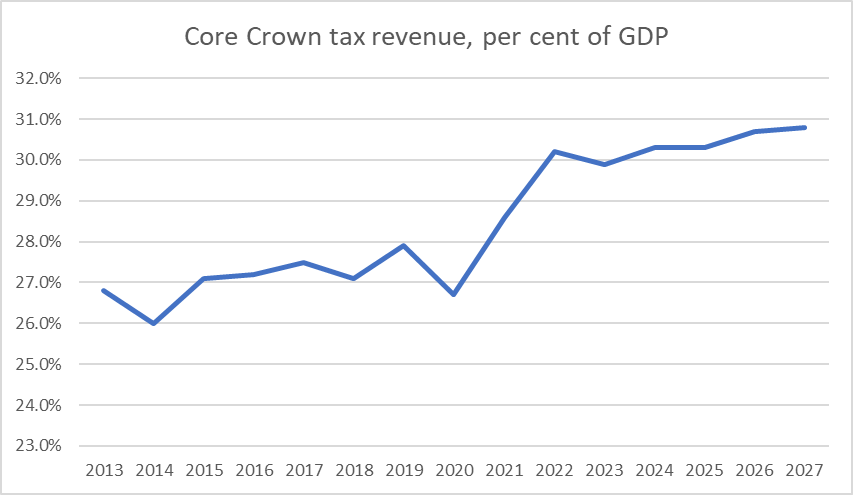

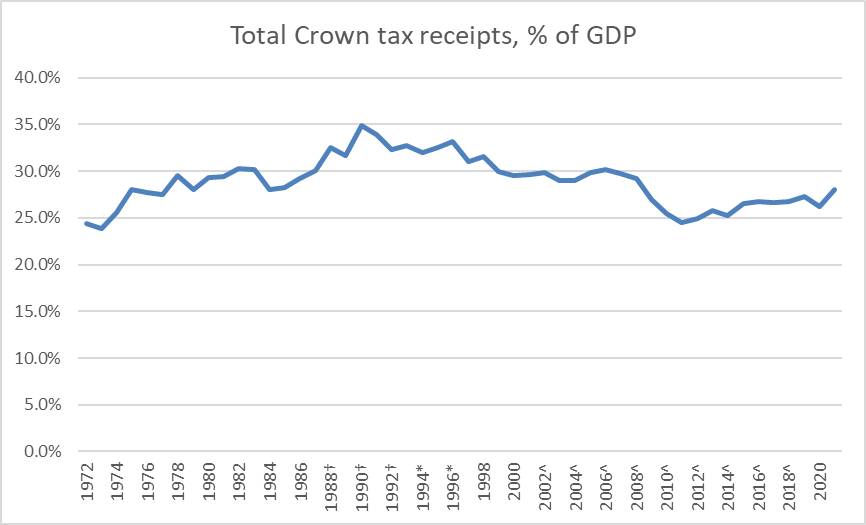

And the third line that caught my eye was this

A good question for the National Party might be to ask how much of this 3.5 percentage point increase in tax/GDP they intend to reverse, and how, or would any new National government simply be content to leave little changed what Labour has bequeathed them?

As longer-term context (slightly different measure to get back to the 70s) the only similarly large increases in tax/GDP seem to have been under the 1972-75 and 1984-90 Labour governments.

I love the second graph, showing projected export volumes and real GDP by the RBNZ.

Export volumes are at about 95, but are going to leap in an almost vertical line straight up to 145 or circa 50%, in a few short years. I would be interested in their justifications for such a bullish forecast?

With a current account deficit of virtually 8% of GDP, let’s hope that the magical thinking of the RBNZ is correct.

Alas, it all looks absurd to me.

LikeLike

[…] Source link […]

LikeLike