Last week the Reserve Bank of Australia hosted a conference on Central Bank Frameworks: Evolution or Revolution. I wrote last week about the paper by Reserve Bank Assistant Governor John McDermott, which was given at the conference.

But when the RBA yesterday released most of the rest of the conference papers, I noticed one that really should be relevant to the current New Zealand work underway reviewing and revising the Reserve Bank Act. Unfortunately, it isn’t a fully worked-up paper, but the slides on “Robust Design Principles for Monetary Policy Committees” have plenty of content (and no equations, for those wary of what they might offer in such contexts), and should offer food for thought for the Minister of Finance and his Treasury officials as they pull together the new legislation. Unfortunately, as far as I can see, the proposed New Zealand model is mostly quite inconsistent with the arguments of the conference paper.

The authors of the paper/presentation have plenty of central banking experience. Andrew Levin is now a professor at Dartmouth, but spent most of his career in research and policy roles on the staff of the Federal Reserve in Washington. And David Archer was formerly head of financial markets and then head of economics at the Reserve Bank of New Zealand, and is now head of central banking studies at the Bank for International Settlements (perhaps somewhat ironic in that David was once known internally for his advocacy – not entirely in jest – of staffing the Reserve Bank of New Zealand with no more than 20 people, including (if memory serves) a cook). David was also one of the peer reviewers for Iain Rennie’s review of monetary policy governance here.

Levin and Archer set out what they are trying to achieve:

- Formulate a set of robust design principles for monetary policy committees (MPCs), that is, the decision-making body delegated with setting the course of monetary policy.

- These principles are intended to mitigate the risk of severe policy errorsarising from two sources: (1) political interference and (2) excessive insularity (“group-think”).

As they note,

- The operational independence of the MPC fundamentally rests on the degree of public confidence in the legitimacy of the institution.

- These considerations provide a crucial rationale for ensuring the transparency and public accountability of the MPC.

As they further note, committee-based decisionmaking for monetary policy is now standard practice around the world, but

However, the benefits of having a committee can be severely undermined by group-think:

- homogeneity of committee members

- consensus-based decisions

- lack of external reviews

In light of those considerations, the MPC should comprise a diverse group of experts who are individually accountable for their policy decisions.

I’m not totally persuaded by the “experts” line myself – one needs lots of expert input/advice to policy, but when it comes to decisionmaking, soundness is at least as important as cleverness. But, for now, I’m mostly telling the Archer/Levin story.

They present some material illustrating the point that legislative independence can (a) be readily taken away if the central bank oversteps badly, or can (b) be of little effect. In the latter camp, they include the effective subservience of the Federal Reserve to the US Administration from 1933 to 1951, but – as they were presenting in Sydney – they could as readily have used the example of the Reserve Bank of Australia, which had legislative independence from its creation in 1959, but no effective policy operational autonomy. Since the RBA still operates under the same legislation, perhaps it would have been undiplomatic to the hosts to make that point?

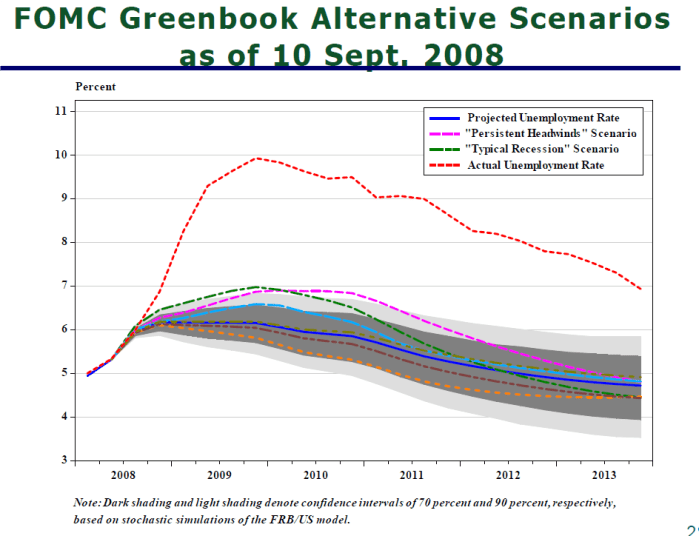

One of their big concerns is “groupthink” – the risk that people within an institution (MPC or more generally) will all come to see the world the same way and in the process miss something really important. They use as an example the Federal Reserve heading into the 2008/09 crisis.

- During 2005-06, officials at the Federal Reserve and other agencies overlooked warning signs regarding the risk of a collapse in house prices.

- During autumn 2007 and early 2008, Fed officials misattributed the widening of interbank spreads to liquidity factors rather than counterparty risk.

- The FOMC met on Tues. 16 Sept. 2008, two days after Lehman’s failure, but still did not perceive that the U.S. might be heading into a financial crisis and a severe economic downturn.

And they illustrate the point with this chart

It is a pretty staggering failure. But, to be honest, I’m not sure it is very enlightening on the question of the best possible design and structuring of monetary policy committees. For example, I’m not sure there is evidence that central banks with governance and decisionmaking processes more consistent with the Archer/Levin preferences did less badly, in recognising emerging issues and risks, than others. And, in many (although not all) respects, the US system fits better with their principles and preferences than those of many other countries.

But I’m jumping ahead. What are the principles Archer and Levin lay out? First

The MPC should be a fully public institution whose members are accountable to elected officials and the general public.

Quite a few central banks – including several in the euro-area, Switzerland, South Africa, and the regional Feds in the US – still have private shareholders. That hasn’t been an issue here since 1936. In most countries, the private shareholders have no real influence, but in the US they do still play a role through the appointment of heads of regional Feds, who in turn sit (in rotation) on the FOMC. That should be fixed, and may even be unlawful – an issue Peter Conti-Brown covered in his book I wrote about here.

The second principle is

The selection of MPC members should ensure diverse perspectives and forms of expertise.

- Earlier studies of MPCs were mostly focused on hetereogeneouspreferences (hawks/doves) or the hetereogeneity of anecdotal information.

- In contrast, this principle combats group-think by appointing experts with diverse educational backgrounds and professional experiences.

- Geographical diversity may also be crucial for fostering & maintaining public legitimacy.

And the third is

The process of selecting MPC members should be systematic, transparent, and consistent with democratic legitimacy.

- The process should have “checks and balances”, i.e., multiple steps involving different sets of decision-makers.

- Transparency mitigates the risk of undue influence by special interests.

- The process should foster public confidence in the integrity of the institution.

In general I agree with this, but this is an area where the US does reasonably well, at least for the core members of the FOMC, the Fed Board of Governors. They are nominated by the President, and subject to confirmation by the Senate, one of the most open processes anywhere. By contrast, the proposed New Zealand system will have the Governor and the Reserve Bank Board – neither with any direct democratic legitimacy or accountability – driving the appointment of MPC members, with the Minister of Finance having no ability to interpose his or her own candidates. And there is no public or parliamentary scrutiny of individual members proposed, either before taking office or afterwards.

The MPC’s size and voting rules should foster genuine engagement among members and diminish the influence of any single individual.

- This principle mitigates the risks of autocracy, which has pitfalls like those of group-think.

- Previous analysis prescribed a fairly small size as optimal for engagement (e.g., 5 members), but a somewhat larger size may be needed to encompass sufficiently diverse perspectives.

In principle, the US system does well on this score. No one on the FOMC owes or her appointment to anyone else on the committee, and many of the members are based outside Washington.

And they propose

Terms should be staggered, non-renewable, and last longer than the political cycle, with removal only in cases of malfeasance.

The non-renewability point is about limiting the risk of inappropriate political interference. I have some sympathy with that point – Archer elsewhere argues for single seven year terms. Then again, non-renewability even more severely restricts the possibility of holding MPC members to account for their contribution or performance. For my tastes, Archer/Levin lean a bit too much on the side of protecting against political interference, and bit too little on the imperative on ensuring that the appointees actually do the job they have a mandate for.

Principle 6 is a very important one in my view, and one which our Minister of Finance appears to have totally discounted.

Each MPC member should be individually accountable to elected officials and the public.

- Individual accountability is crucial for mitigating the risk of group-think.

- Such accountability should occur through MPC communications, speeches & interviews, and hearings before elected officials.

- To avoid cacophony, the MPC must clearly explain the rationale for its decisions as well as elucidating the range of individual views.

By contrast, our Minister of Finance has plumped for consensus as far as possible, and no individual identification of the range of views. That conduces not just to groupthink, but to free-riding (by minority external members). There is much stronger individual accountability in the Swedish, UK, and US systems. That said, as the example Levin and Archer used shows, no system of governance guarantees against policy mistakes.

The MPC should be subject to periodic external reviews of its strategy and operations, but not its specific policy decisions.

- External reviews can be invaluable in identifying and mitigating group-think.

- Such reviews should occur on a regular schedule rather than triggered by political motives or idiosyncratic factors.

- These reviews should focus on assessing past & prospective performance, not on evaluating individual policy decisions.

It would seem highly desirable to build such external reviews into the system, perhaps every five years. They should be commissioned by the Minister and Treasury, and should complement any reviews the MPC undertakes, or commissions, of its own performance.

In addition to any statutory goals, they argue

The MPC’s medium-term policy framework should be approved or endorsed by elected officials roughly once every 5 years.

- This framework should provide a quantitative description of the MPC’s objectives, priorities, intermediate targets & operating procedures.

- The approval or endorsement of elected officials is crucial for the legitimacy and credibility of the policy framework.

In a New Zealand context, it might be desirable to have the document that replaces the Policy Targets Agreement be subject to parliamentary ratification (as the – much less important – Funding Agreement is).

I’m less convinced of their next principle

The MPC should formulate a systematic and transparent strategy that guides its specific policy decisions over the coming year or so.

Easy enough to write down, but hard to make it mean anything particularly specific.

And their final principle is

The MPC should regularly publish reports explaining the rationale for its specific decisions in terms of its policy framework and strategy.

These reports should explain the rationale for the majority’s decision along with concurring and dissenting opinions that clearly convey the range of individual views.

I agree. A good comparison is with the decisions made by higher courts, which in effect sit as a committee. Majority and minority opinions are published, and groups of members may come together in support of a particular written opinion, rather than all penning one each.

Perhaps they were running out of time, but the last slide only has headings

Insiders & Outsiders on the MPC

- Full-Time vs. Part-Time

- Executive vs. Policymaking Roles

- Differential Terms of Office

Fortunately, we know from David Archer’s comments on Iain Rennie’s draft report what he thinks on the insiders vs outsiders issue.

Turning first to the balance of internals and externals. The tendency to groupthink, with the most powerful member of the group being the “seed” of the group view, is the biggest impediment to harnessing diversity. The probability of groupthink increases with the presence of hierarchy.

F. The law should restrict the proportion of executive insiders to below half, by a big enough margin that these tendencies have a chance to be offset.

Sadly, our Minister of Finance has chosen a model – a permanent majority of insiders, the Governor having significant influence on other appointments, and no freedom to speak externally – which will entrench hierarchy, create a strong likelihood of groupthink.

And here, from Archer’s earlier comments, are his thoughts on publication of minutes, and openness about the range of views and perspectives.

Turning now to the public presentation of committee decisions, claimed improvements in policy transmission mechanisms flowing from singular official views about future policy are ephemeral. Apparent unanimity is quickly shown to be untrustworthy spin.

The essential reason is that the future is largely unknowable, and it is foolish to pretend otherwise. Consider the records of the few central banks – including the RBNZ – that publish forward policy interest rate paths. Forecast paths are almost always poor predictors of reality, even in the RBNZ case where unanimity about the outlook exists by construction. Being honest about the limited predictive powers of even highly paid specialists is likely eventually to increase their trustworthiness, at least relative to the results of repeated false marketing of ostensible consensus. With unknowable future shocks, the real predictability problem relates to how policy will react to new events. To predict that, one has to know policy preferences and the mental frameworks used to process new information (as well as forming a view on what new information might arrive). Given clear legal objectives supplemented by PTAs, the range of policy preferences in play should be constrained. The main thing then is to allow people to observe the variety of analytical frameworks being deployed. That is not helped by delaying the publication of minutes. Gains in withholding minutes are thus small, if they exist at all. At the same time, requiring members to withhold from expressing their true views in public, at least for non-trivial periods around policy decisions, may damage their ability or willingness to articulate alternative perspectives.

How can cacophony in communications be avoided without some formal constraint? One approach would be focus members’ attention on agreeing minutes that accurately reflect their individual contributions. Fairly full minutes, with attributed reasoning, can provide a better public platform for dissenters’ subsequent public utterances than can the soundbites of “managed” disclosures about policy decisions. If such minutes will be available soon, members are more likely to refrain from immediate but partial expressions of their views.

As I hope is clear, I don’t agree with everything in the Archer and Levin presentation but there is plenty of material here that really should be thought about by our Minister and Treasury officials, to a much greater extent than was evident in the papers published to date. It isn’t too late to rethink these details, and doing so would be likely to lead to a better central bank – better on substance, and more accountable and thus more enduringly legitimate.

As it happens, the Herald this morning has a first “interview” with the new Governor Adrian Orr. It is a typical Herald piece as regards the Reserve Bank: giving the Governor a platform to speak, rather than showing signs of any searching or awkward questions. I thought it was interesting for three things:

- all the focus appeared to be on monetary policy, even though more of the Bank’s staff now work on the financial system regulatory and supervisory roles,

- there was no mention of the scathing feedback on the Reserve Bank, regarding those same regulatory/supervisory activities, in the New Zealand Initiative report, and

- while there was plenty of talk about broader perspectives etc, there wasn’t much (any) talk about doing the basics better.

Thus Orr talks grandly of leading the world

“We need a broader view of the what the central bank is really about. We’ve got an enormous amount of grey matter in here — that can be used more effectively,” Orr said.

“So what is global leadership in managing a small, open economy, what is global leadership in ensuring a sound financial system, what is global leadership in the delivery of the means of exchange?”

But not at all of the miles he – and the Bank – have to go just to catch up and come closer to doing excellently the basics Parliament has charged them with: keeping inflation near target, and supervising the financial system in a way where the analysis and regulatory actions consistently command confidence. There was a lot of talk of “leading the world” back in the 1990s, and in some small areas, almost inadvertently, we did. But I’m not sure it is a goal New Zealand taxpayers should be actively seeking to fund, and especially not when the domestic basics leave quite a bit to be desired.

(It is the school holidays, and my 11 year old daughter wants to tell people that instead of reading “all the boring stuff my Dad writes you should listen to Ed Sheeran instead”. Personally, I’ll take Mozart or Handel over monetary policy – let alone Ed Sheeran – any day.)

Or Mahler

LikeLike

Bit modern for my tastes, but yes…..

LikeLike

All three wrote music that has lasted for generations, as indeed did Gershwin, Puccini, Irving Berlin, but Sheeran! Nah.

LikeLike

That is exactly the conversation I have with the child in question, but I guess at 11 – even with quite a fascination with history as she has – it is hard to get your head around the test of time, and the possibility that her current favourite might not pass it.

LikeLike

Reblogged this on The Inquiring Mind and commented:

For a government trumpeting openness and transparency, this seems a strange way to proceed.

LikeLike

No mention of multi-tasking: reading and listening simultaneously. When you are young it is quite possible. If the music is challenging with the anticipated note replaced by a much better one then concentration suffers. The ultimate for preventing any other thought processing is Art Tatum.

LikeLike

[…] written various posts on aspects of the detailed design issues. And in a post last week, I dealt with a recent conference presentation on these and related issues by two former […]

LikeLike