The results of the Reserve Bank’s quarterly survey of expectations were released yesterday (in a curious change of timing, the Bank now collects the data before the Monetary Policy Statement, but doesn’t release it until a few days afterwards).

There wasn’t a great deal of interest in the headline numbers, except perhaps for a pretty large increase in the extent to which respondents (all 56 of them) think that monetary conditions are very easy at present: a net 64.3 per cent think conditions are more relaxed than neutral (45.7 per cent three months ago), more than at any point in the 30+ years the question has been asked. There was also a pretty big change, in the looser direction, in expectations about future monetary conditions. I’m not quite sure what led to that reassessment. One obvious candidate might have been the surprise in the most recent CPI but, as it happens, there isn’t much change in the headline inflation expectation numbers. Perhaps the answer doesn’t really matter that much, but it would still be interesting to know why a bunch of able people have change their assessment quite that much this quarter.

Once upon a time the Reserve Bank’s two-year ahead measure of average inflation expectations lined up pretty well with trends in core inflation. In this chart, I’ve shown it plotted against the sectoral factor model measure of core inflation, the Reserve Bank’s preferred indicator.

Notice that I used the term “lined up”. In this chart I’ve simply shown expectations as surveyed in a particular quarter (but about outcomes two years ahead) and core inflation outcomes in that particular quarter. If one does the chart with the expectations numbers shifted two years ahead (to tie up with the date the survey actually asks about) the relationship is a bit weaker.

The Reserve Bank used to use this two year ahead measure as a proxy for how wage and price setters – and, at least notionally, borrowers and lenders – took account of inflation: these numbers directly influenced the base inflation forecasts. They’ve since moved away from that. But my interest today isn’t so much the Bank’s own forecasts, but the answers to the expectations questions themselves. Why, for example, have so many otherwise able people gone on predicting that (core) inflation would be around 2 per cent when it has actually kept on coming in at 1.3 to 1.5 per cent? Perhaps part of the story is “laziness” – if the Reserve Bank, with all its analytical resources, keeps telling the public core inflation will be getting back to 2 per cent perhaps respondents (mostly busy people) just take them at their word? If so, perhaps there is a troubling possibility that we might be a little better off if the Bank didn’t publish (consistently wrong) projections. Perhaps the answer is more ‘ideological’ – the deep conviction, shared by so many, that current conditions are ‘abnormal’, must soon “normalise”, and therefore (almost by construction) inflation must soon get back to target? Whatever the answer, at present the results of the survey seem to tell us more about the respondents than about the actual outlook for inflation.

The focus of analysis is on the mean (average) expectation, because that is the data the Reserve Bank makes readily available. But there is a richer array of data behind the headline, some of which the Bank sends out in a quarterly report to the respondents to the survey (of whom I’ve been one for the last couple of years). There is a median expectation – in some ways, in principle, a more useful measure than the mean, although over the last few years there have not been any interesting differences. But they also provide information on the highest single expectation, the lowest single expectation, and the upper and lower quartiles. I only have the data for the period since I’ve been a respondent (but it would be good if the Bank would make the data, for this and other questions, more generally available on their website).

Typically, there has been a range of about 1.5 percentage points between the highest and lowest individual expectations. If one looks at the actual variance in the core inflation series (chart above) that doesn’t unreasonable: economists (on average) never successfully forecast recessions, and probably don’t do that well on the surges or slumps in core inflation either. For what it is worth, here is a chart showing the highest and lowest two-year ahead inflation expectations, and I’ve shown my own survey responses as well.

I was a little surprised at how much the minimum expectations had increased (and perhaps at how low they got in 2016), but there has also been a visible step up in the maximum expectations. As for my expectations, I was a bit surprised to find that my expectations were the lowest of all 50 respondents in two of the last three surveys. It doesn’t greatly trouble me – my forecast methodology at present is that after seven years of very low and stable core inflation it needs something out of the blue (eg the Reserve Bank finally getting the right model, and attitude) to make me think things will be very much different two years from now than they’ve been for the past seven – but it is an interesting reflection of where crowd opinion (the semi-expert) version has moved to. If we end up with core inflation still hovering around 1.3 to 1.5 per cent, almost every single respondent to this survey (which includes many of the prominent market economists) will have been surprised. In fact, right now even the lower quartile response is 2.0 per cent – a (core) inflation number the Reserve Bank hasn’t managed to achieve for eight years now. Perhaps respondents will be proved right – there is certainly a growing tide of sentiment globally picking a return of inflation (and really reckless fiscal stimulus in the US will help, for now, in the world’s largest economy) – but it would be a turn up for the books if they were.

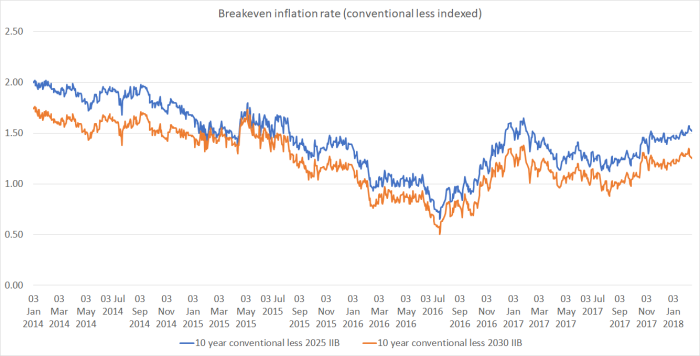

And I’m at least a little comforted in my own random walk (core inflation will be – best guess – what it has been) expectation, by the numbers thrown up by people actually putting money on these things. I showed this chart a few weeks ago – the gap between our 10 year conventional government bond and the two closest inflation-indexed bonds.

Nothing in those implied expectations suggests we are about to see a material change from the sorts of outcomes over this decade to date. Half-way between those two lines, and the latest breakeven inflation number is about 1.4 per cent – coincidentally (or perhaps not entirely) the current sectoral core factor model inflation rate).

Here is the same chart for the United States, from the St Louis Fed’s FRED database.

The short-term patterns are pretty similar – as you might expect, since there clearly are some common global forces at work – but the levels are now quite different. The market seems to expect US CPI inflation (not the variable the Fed targets) to average around 2 per cent over the next decade.

But not here.

If the RBNZ relaxes the current Bank licencing restriction on all the giant Chinese banks to operate with their respective parent groups trillion dollar balance sheets rather than restrict their lending to their local subsidiary company capital of a meagre $200 million plus whatever NZ local savings that they can gather then we would see some real competition in lending interest rates. The current relaxation of those restrictions on China Construction bank raises the prospect that this will be extended to the rest of the Chinese banks.

Our Australian owned banks currently has a monopoly advantage with $166 billion cash deposit savings on their balance sheets to lend with.

LikeLike

“Our Australian owned banks currently has a monopoly advantage with $166 billion cash deposit savings on their balance sheets to lend with.”

Deposits are a liability of banks, customers might withdraw them and the customer expectation is usually that the bank will just hand over their money when they do that.

LikeLike

And lending is an asset on a banks books.

When the GFC event hit NZ shores, the Government very quickly put in place a Deposit Guarantee Insurance scheme forced onto the banks which gave depositors confidence and reassurance at this critical time.

The RBNZ also has recourse under the OBR to freeze a banks operations and to trim depositors liabilities to rebalance a banks balance sheet if needed.

LikeLike

Of the 56 respondents, how many are coal-face operatives, in businesses that have to assess and re-asses price settings 1 and 2 years out, and how many of those respondents have 2 and 3 degrees of separation between themselves and the coal-face

LikeLike

Not sure these days, although I suspect that something like a majority are economists (sometimes working in commercial organisations, and even perhaps sitting on ALCOs in banks), and there are other people who run eg sector groups. So it is genuinely a survey about macroeconomic expectations, not about firm level pricing behaviour (QSBo does that) – and it is an open empirical question whether those macro expectations capture something also relevant to the way firms and households actually behave, in price-setting , wage bargaining, and in assessing nominal interest rates. The Bank’s research these days suggests generally not.

LikeLike

Surveyees who are consistently wide of the mark should be removed from future surveys I should think. If ones cares about gathering useful data that is, rather than just going through the motions.

LikeLike

I can see the argument, but recall that it is a survey of what people think (in many case people who are advising others), and the median respondent in the survey has been no more wrong than the Reserve Bank (actually charged with delivering inflation around 2%).

What might be interesting for the Bank would be a research exercise to see how various respondents have done over time, and whether there is any useful information in that. Some respondents will have done better than others in particular periods, but there is always the question of whether that is just by chance. (For example, I’ll lay claim to having been less wrong than the median, but I’ve only been in the survey for 2.5 years – altho my internal advice in 2013 and 14 was along similar lines – and might well miss when inflation actually does pick up strongly, and have been persistently wrong at times previously). They could do it anonymised for the non-specialists (eg, respondents 1,2,3…..27) but for the specialists who publish numbers could even do it on a named basis (they already track the individual forecasts of prominent forecasters as one input to their own deliberations)

LikeLike

It’s always hard to argue for gathering less data. Breaking out an anonymised subset of those who predicted best in the past would perhaps be better, along with mean, median, and quartiles.

LikeLike

Isn’t there a kind of circularit/reflexivity going on here?: expectations of the “experts” are influenced by what the Reserve Bank says is going to happen with inflation and the Reserve Bank is influenced by the experts’ stated expectations….. and they can both be continually reinforcing each other’s views – and continually be wrong?

LikeLike

There is a risk of that – but perhaps esp from the RB which often tells us that inflation expectations (measured by such surveys) are just fine. But that shouldn’t comfort them, or anyone else, if those reported expectations don’t influence actual market behaviour, and if they are persistently wrong.

If anything, I suspect market economists (most) and the RB share a broadly similar “model”, which has now been wrong for several years.

LikeLike

I still struggle with your seeming crusade for higher CPI inflation. I don’t see how it helps anything or anyone other than create distortions. Most grievously it reduces my real income and consequently my purchasing power. It potentially makes my business less competitive.

If after running a very loose monetary policy for a few years, inflation is still low, then great. The target range is not sacrosanct. Change it to something more fitting for the environment we are in and the problem is gone! My understanding, which may be wrong, is that inflation targeting is primarily concerned with preventing high inflation and the manifold problems it brings, whereas low stable inflation (excluding deflation) is relatively harmless in the scheme of things.

LikeLike

Generally, higher inflation won’t undermine real incomes or make businesses less competitive (wage-setting and the exchange rate adjust).

I guess i have two real concerns. One is that the RB hasn’t, on its own accounting, given up the game. They keep picking inflation to get back to 2%, setting policy accordingly, and keep getting it wrong. Since our elected leaders have set that goal, and empowered the Bank to achieve it, that failure disconcerts me as a matter of good governance.

But perhaps my biggest concern – globally – is how badly placed countries are going to be when the next recession happens, and the OCR simply can’t be cut much. it would be distinctly preferable to be acting now and getting inflation up from around 1.4% to say 2.2 or 2.3%, and in the process create another almost a percentage point of room to cut when that next recession comes.

Oh, and I’m also concerned for the people who are unemployed who needn’t have been if monetary policy had been run a bit more aggressively to deliver inflation around 2 per cent.

Re the target, it wouldn’t entirely surprise me – on the basis of a comment from Robertson late last year – if the new PTA deletes the specific ref to the 2% target midpoint. If that happened, it would deal (largely) with my first concern, but would leave the others standing.

LikeLike

I’m surprised by your opening remark, since it would seem to imply you feel inflation is not harmful but “generally” nets out by various adjustment mechanisms? Maybe in the longer term wages might adjust over some kind of average, but for that does still imply loss an immediate loss for some. There can be numerous other specific factors at play in wage setting, not to mention long lags before an adjustment occurs. Likewise with the exchange rate.

I’m trying to think this through in an intuitive way – so say the OCR has been cut, investment has increased a little but also, as intended, inflation is now a little higher relative to our trading partners, and the exchange rate has adjusted down restoring competitiveness. If I happen to be an exporter at best that might restore my export income to the place it was before inflation made me less competitive. However, if my product uses imported components then probably I am still going to be worse off. Furthermore, I am also a consumer of imported goods so my purchasing power is adversely affected by the lower exchange rate. And probably I am less inclined to give my workers a compensating pay rise. On top of this, if I happen to be a depositor the real return on my fixed income is lower (not only is the deposit rate lower, inflation is higher). So at this point I still fail to see how any of this helps me or the country. Using monetary policy to drive up inflation just seems to me to be counter intuitive (unless there is some real risk of deflation which there certainly isn’t).

Your point about the Reserve Bank publicly asserting itself to still “being in the game” I accept. But if inflation outcomes over a long period of time point to the possibility that mid-point is no longer appropriate or helpful to the economy (as seems apparent to me), maybe the emphasis should be on amending the policy target.

Your next point, lowering interest rates now to generate inflation that will subsequently require interest rates to be raised again, just so we can have more headroom in a future financial crisis just seems topsy turvy to me. I can only think I misunderstand.

For the point about unemployment… in a situation where we have low and reasonably stable inflation – is higher inflation, albeit with slightly higher investment, really going to help the employer or the unemployed get a job? I suspect a better, more direct policy lever for helping the unemployed would be to cut the level of immigration.

LikeLike

Inflation itself has modest real costs (incl from the interaction with a nominal tax system) but society – well, our elected representatives – have decided that something centred on 2% inflation is as close to optimal as we’ll get (nominal downward rigidities meaning there are costs to extremely low inflation).

On your second para, it looks a bit as tho you are conflating reals and nominals (perhaps not). The process of getting from the current core 1.4% to 2% core inflation could be expected to involve some temporary undershooting of the real interest and exchange rates, and on the other hand a temporary boost to activity and employment. So in the transition there are distributional effects: some win, some lose. But when inflation settles back to 2 per cent we can expect that nominal interest rates will have adjusted to the higher inflation, and the nominal exchange rate will have done the same thing and nominal wages too), leaving no one persistently better or worse off from the higher (stable, expected) inflation rate.

On your para about changing the target, if anything i would consider raising the target (again, to cope with zero lower bound issues). Recall that the unemployment rate has been above the Bank’s own estimate of NAIRU for almost all of the last 9 years, which isn’t an obvious point from which to say, “oh, no worries, lets just lower the inflation target”. We could have had a bit more prosperity, and a bit less unemployment a bit sooner, and had inflation on target.

On the “cut interest rates to raise them more later” argument, recall that the strongest correlation in the cross-section (across countries) is between high inflation and high nominal interest rates (it is also substantally true across time within countries). Action now to drive inflation up to, say 2.5 per cent should over several years enable us to get the OCR 100bps or so higher than it is now (with core inflation around 1.5%), given more leeway for using mon pol when the next severe recession comes. Of course, it doesn’t help if the next severe recession comes next month, but it doesn’t hurt either.

LikeLike