2024 will mark 40 years since the great acceleration of policy reform that began with the election on the 4th Labour government in July that year and ran for the following decade or so. I’m sure there will be lots (and lots) of reflections on the period later this year, most especially from the left where the ongoing political angst seems greatest (yes, it really was a Labour Cabinet that kicked off the process and did many of the lasting reforms, much as some on the left remain very uncomfortable about that).

If one thought about the big economic issues that were around at the time, they could probably be grouped under three broad headings:

inflation

fiscal deficits and government debt, and

productivity

One might add to the list the balance of payments current account, which became no longer a policy problem once capital controls were lifted at the end of 1984 and the exchange rate was floated in early 1985. (Yes, recent deficits have been very large, but as a symptom of other imbalances, rather than a policy issue in its own right.)

Of that list, New Zealand has done fairly well on the first two items.

We used to have among the worst inflation record among the advanced countries (high and variable), but in recent decades we - like most advanced countries - have done much better. The last three years have been a bad lapse, but if that never should have been allowed to happen, the ultimate test is whether things are got back under control, and we seem now to be on course for that (eventually the lagged infrequent data will emerge). I’m not here going to get into lengthy debates about other countries, but whatever the common shocks once a country floats its exchange rate its (core) inflation outcomes over time are its own choices (see Turkey for any doubters).

We’ve also done pretty well on fiscal policy imbalances. There are plenty of leftists around who think taxes and spending should have been, and should now be, higher, but my focus is imbalances (deficits and debt). Again, the last few years (post Covid spends) have been bad, but under governments led by each main political party, New Zealand has over decades done a reasonably good job of keeping debt low and reining back in deficits when they have first blown out. And our system of fiscal policy transparency is pretty good too (although like almost anything could be improved).

One could throw financial stability into the mix. Almost every country that liberalised in the 80s ran into serious financial sector problems a few years later (neither the private sector lenders and borrowers nor the putative regulators really knew what they were doing, perhaps unsurprisingly after decades of financial repression), but the last 30 years have been pretty good. Lots of finance companies failed 15 years ago, which wasn’t necessarily a bad thing (risk and failure are integral parts of a market economy), but the core of the financial system has been sound and stable. Plenty of countries would have traded that record for their own experience.

The big hole in the story has been around economywide productivity. 40 years ago people were highlighting how far New Zealand’s performance had fallen (official reports from as early as 60 years ago were already drawing attention to growth rates having slipped behind), and the hope/aspiration was to turn that around. This is one of my favourite photos (reproduced in the Herald a decade or more ago, but showing late 80s Minister of Finance David Caygill)

Even though there had been not-insignificant economic reform and liberalisation over the previous few decades, in the early-mid 80s it was easy to highlight the many very obvious inefficiencies in the New Zealand economy (car assembly factories dotted around the country to name but one example). The previous decade in particular had been a very tough time for New Zealand - hardly any productivity growth at all after 1973/74 – probably less because economic policy became particularly bad (one could quite a long list of useful and important reforms, alongside other problems and new distortions - eg Think Big) than because the terms of trade were very weak.

Almost as bad as the worst of the Great Depression, but averaging low for longer. Exogenous adverse shocks to both export and import prices impeded the ability of the economy to generate high average rates of real productivity.

As recently as 1970 (when the OECD real GDP per hour worked data start) and despite decades of inward-looking policies New Zealand’s average productivity still didn’t look too bad. We were below the median OECD country but not by much, just under the G7 median, and more or less than same as the big European countries (UK, Italy, France, Germany). By the time of the 1984 election we’d slipped a long way further.

We were by then around the same as Greece, Ireland, and Israel, and of the G7 well behind all except (still fast-emerging) Japan.

Here is where we are relative to the same group of OECD countries in 2022

We’ve done clearly pulled away from Greece, but that is about the only semi-positive I could find (and yes, the gap to Italy has closed somewhat as well). For what it is worth, on the data to hand so far 2023 looks to have been a year when New Zealand average productivity fell.

Of course, the rate at which we’ve been falling down the league tables has slowed. But then remind yourself what happened to the (merchandise) terms of trade

They have trended upwards since the late 80s (I remember our puzzlement at the RB when the first late 80s lift happened) and especially in the last 20 years. On this measure (which excludes services, to get a long-term consistent series) the terms of trade have averaged higher than at any time in the last century. And yet still average productivity languishes.

There are of course a whole bunch of new OECD members since 1984. A large group of them were then either part of the Soviet Union or communist-bloc countries, even the least bad of which had much more messed up economies than New Zealand’s. This is how we compare now with that group

Middle of that pack to be sure, but probably not for long on the trends of the last couple of decades. South Korea is just about to go past us too.

It really has been a shockingly bad performance by New Zealand, against what would normally have seemed a propitious background - a sharp sustained recovery in the term of trade and a much greater reliance on letting market price signals work. There isn’t much serious basis for wishing away this failure.

And yet there seems to be little sign that our politicians or their official economic advisers have much interest, or any serious ideas for finally reversing the decades of real economic relative decline.

It is as if the powers that be and those around them have simply become resigned to our diminished fortunes, indifferent to what that failure means for actual material living standards now, and those for our children and grandchildren to come.

The Herald ran an op-ed yesterday under the heading “Why the Government’s new Reserve Bank mandate may lead to worse outcomes”. It was written by Toby Moore who served as an economic adviser in Grant Robertson’s office while he was Minister of Finance (a fact the Herald chose not to disclose to its readers).

I’m more interested in the substance of his argument. Moore is a serious guy, and I suspect he’d run his arguments whether or not he’d ever taken up a role with Robertson. But I think his core argument ends up not very persuasive.

Moore opens his article pointing out that there isn’t an overly strong economic case for having reverted to something very like the old statutory objective for monetary policy. There are certainly bigger economic challenges (albeit probably not ones the law draftsmen could tackle as quickly). As the Governor repeated again yesterday – while trying to minimise the extent to which the previous wording was actually a “dual mandate” (a point on which he was correct, but not a point he’d have made often under the previous government) – no monetary policy decision in the last few years was made differently because of the revised wording of the statutory mandate. That is entirely convincing: the Reserve Bank’s big mistakes (and they were very big mistakes) were forecasting ones. Given their forecasts their OCR choices made (more or less) sense. But they misunderstood how the economy was operating and how real the inflation risks were.

But then Moore attempts to argue that much of the previous 30 years would have been different (and better) if only the Reserve Bank had spent those decades operating under the statutory mandate it had from 2019 to 2023. The episode I want to focus on is that from a decade or so ago. These are his words

One can see the issue more starkly in this chart

As one added bit of context, in 2012 a requirement was added to the Policy Targets Agreements requiring the Governor to focus on delivering inflation near 2 per cent, the midpoint of the 1-3 per cent target range.

I agree with Moore that a series of bad monetary policy choices were made by the Reserve Bank during this period. In fact, while I was still at the Reserve Bank I argued against the proposed tightening cycle that eventuated in 2014 on the twin grounds that core inflation was very low, and (consistent with this) evidence from the labour market suggested quite a lot of slack still in the economy. Once I left the Bank in early 2015, it became a regular theme in commentary on this blog.

But…..the key point is that, once again, economic forecasts were very wrong. The Bank’s forecasts during this period usually had core inflation coming back to the midpoint and needing higher interest rates to keep it there.

And actually I think there is a fair argument - that should appeal to Moore, although not to some others - that during in 2010s one problem was that the Governor, having recently returned from a long sojourn in the US, became fixated on the housing market and the US crisis of 2007-09, and constantly wanted to orient policy to lean against such risks, without ever stopping to consider (a) similarities and differences between NZ and the US, or (b) his statutory mandate. It wasn’t the biggest factor in setting monetary policy wrongly – policy that delivered core inflation bouncing near the floor of the target range for years – the problem was forecasting failure and bad models – but it didn’t help either.

A central bank in the early 2010s (a) strongly focused on the inflation target, and (b) with better forecasts/models (or just looking out the window) would have delivered a lower OCR during that period, and in particular would not have championed a substantial tightening in 2014. That would have had better outcomes for inflation and for unemployment.

Reasonable people can differ on how best to specify and to articulate what we look to the Reserve Bank to deliver with monetary policy, but the problem a decade ago wasn’t some excessive focus on inflation, but a poor understanding (shared of course with many others here and abroad) of just what was going on. Arguably, looking out the window - at actual headline and core inflation - might have given a better steer during that period. A ‘dual mandate’ simply wouldn’t credibly have made any difference, given all else we know. The unemployed paid a price for those limitations/mistakes (as holders of fixed nominal financial assets have paid a big price for central bank mistakes in the last year or two).

Excellent central banks matter. They make a difference to real people, real outcomes. It would be good if we had one, and/or a government seriously resolved to deliver a better one.

[NB: I wrote a few quick paragraphs here before fully appreciating that nothing of the government’s own policies were being allowed for in the numbers (which itself seems unsatisfactory). Nonetheless I am leaving the post up because (a) I don’t want to pretend it wasn’t written, and b) the Treasury’s own comment (see below) that, to a first approximation, government plans to date do not seem likely to improve the outlook, and c) the fact that the Minister’s statements give no particular reason to think actual policy will be better than what is allowed for in these numbers. Fiscal policy has been badly mishandled in recent years and we should not be looking at deficits for the next few years.]

As I wrote prior to the election, both in the PREFU (reflecting Labour’s plans, some plucked from the ether just in time for Treasury to do the numbers) and in National’s Fiscal Plan, there was a strong element of either wishful thinking or vague “trust us, we’ll do it” about the numbers. Both parties talked up getting the operating balance (OBEGAL) back to surplus by 2026/27, but neither gave us any specifics as to quite how the substantial structural deficit was going to be closed. There were lines on a graph, and that was about it. In its pre-election plan National indicated that by 2026/27 it would deliver a slightly large surplus than Labour (in PREFU) had foreshadowed.

That was then. In their pre-election fiscal plan, National’s numbers were for an OBEGAL surplus in 2026/27 of $2.9 billion. In the first EFU of the new government, incorporating the new government’s fiscal plans [UPDATE: the government’s plans are not included, but - see note below - Treasury’s best guess so far is that for things foreshadowed or announced they would make little difference], that surplus has been revised down to $140 million, basically zero (Treasury shows it as 0.0% of GDP). Recall that under the previous government, the date for a return to surplus was always just somewhere over the (rolling forward) horizon. Is it any different now? And the revisions aren’t just to that one year: for 2025/26, the Fiscal Plan foreshadowed a deficit of $1.0 billion, but the HYEFU numbers now show a deficit that year of $3.5 billion.

Core Crown spending was, unambitiously, supposed to fall to 31.0 per cent of GDP by 2027/28 (the only year for which the Fiscal Plan gave us numbers), but HYEFU has spending that year of 31.4 per cent of GDP. Perhaps unsurprisingly, net debt by 2027/28 is also a couple of billion higher in 2027/28 than National’s plan had portrayed.

In the grand scheme of things, these dates are quite a long way away, and the changes are, in isolation, perhaps of only middling significance. But from a starting point of (a) years of structural deficits (when one, just possibly two, years of deficits might have been warranted by Covid), and (b) repeated revisions which pushed further into the future the return to surplus, it is hardly an encouraging sign from the new government and its Minister of Finance (whose comments on the HYEFU bottom lines seems to take them for granted, rather than foreshadowing something materially less bad).

And all this in a “mini-Budget” (perhaps itself an ill-advised pre-election promise, which put the Minister against very tight deadlines) that seems to offer nothing any more specific about how the government proposes to return to surpluses, and what (at scale) it proposes to spend materially less on.

It was all rather underwhelming, and the slippage relative even to what National was promising just over two months ago is disappointing. It is though perhaps consistent with the pre-election rhetoric from National that seemed very little bothered by the size and duration of the run of fiscal deficits Labour had run, and proposed to carry on running. Sure, they have to deal now with coalition partners, but when the first fiscal numbers have a worsened outlook it hardly speaks of a strong and demonstrated commitment to “getting New Zealand back on track”. On these numbers, we’ll have had eight years in a row without an OBEGAL surplus…..and even those numbers rely on high-level wishful plans rather than concrete specifics.

On the economic numbers, much will have been superseded by the surprises in the GDP numbers last week. But it is perhaps worth noting that - working with much the same information the Reserve Bank had for its MPS late last month – the Treasury reckoned that the economy was still runnjng excess demand to a greater degree than the Reserve Bank (a positive output gap on average for the year to June 2024), but that the Treasury also envisaged earlier room for OCR cuts (having the OCR at 4.9 per cent by June 2025, while the Reserve Bank was projecting 5.4 per cent), with a weaker exchange rate too.

UPDATE

From the HYEFU document.

UPDATE:

Notwithstanding the Treasury headline, the highlighted sentence is probably more pertinent. With a higher than previously forecast population, potential output has still been revised down, so mediocre is the NZ productivity story. Treasury should probably have been more careful earlier about believing that somehow productivity growth had accelerated in the wake of Covid, something for which there was never any a priori reason to expect/believe.

The fall in New Zealand’s per capita real GDP (averaging production and expenditure measures) over the last year has been quite striking set against other advanced (OECD) countries for the same period. We are equal second-worst, and quite a bit worse than the next country with its own monetary policy (Sweden) - I’m mainly interested in the inflation situation. The fall in real per capita GDP in New Zealand thus far isn’t much short of the fall experienced in the 2008/09 recession.

With recent data it is certain there will be revisions and thus it isn’t impossible that the last year might end up looking a bit less bad. But for now, the published data are the best official guesses - for us, and for fiscal and monetary policymakers.

The OECD has data on quarterly real per capita GDP, going back a fair way (a lot further for some countries than for others, but pretty comprehensive for current members from the mid 1990s). I was curious how common falls in real per capita GDP had been in that database.

For the 1980s there isn’t data for many countries, but we find large annual falls in real per capita GDP as follows

Australia 1982/83

Canada 1982 (at worst about -5% per annum), and

the United States 1982 (the recession that saw them get inflation down.

Coming forward to the early 1990s we find

Finland 1991/92 (some mix of domestic financial crisis and the fall of the Soviet Union)

Canada 1991

Iceland 1992

(New Zealand would probably be on the list but our official population series begins in the middle of the early 90s recession)

Moving on a few years and we have

Chile 1998/99

Israel 2001/02

In 2008/09 all but a handful of countries saw a significant fall in real per capita GDP. It was, of course, the recession that ushered in the decade or so of surprisingly low inflation. At worst, per capita real GDP fell by about 5 per cent per annum in the US and 6 per cent in the euro-area (and about 4 per cent here).

In and around 2012 various euro-area countries (but notably Greece) did dreadfully, but the euro-area as a whole only saw real GDP per capita falling at about 1 per cent per annum during that period.

Covid intervened – when we shut down economies for a time and deliberately wound back economic activity – but otherwise there are no big falls in per capita GDP on an annual basis in places with their own monetary policy until……New Zealand right now.

What we have seen over the last year isn’t normal or small, but a large fall, of the sort seen in advanced economies only in pretty adverse times.

Why focus on real per capita GDP? The public commentary tends to focus on GDP itself, with all the attention on whether the total size of the economy is rising or shrinking. But for most economic purposes, and certainly for inflation purposes, it isn’t a very relevant measure. Zero per cent growth in GDP means something a great deal different if the population is static or falling than if it is growing at 2.5 per cent per annum. It is (much) more likely that excess demand pressures are easing if – absent really nasty supply shocks – per capita real GDP is falling, even if there is still some headline growth in GDP itself.

That said, all such comparisons, especially across time, take one only so far. In an era of really strong underlying productivity growth, even a moderate GDP or real per capita GDP growth might be consistent with easing excess demand pressures, and if productivity growth is historically modest – as it has been in much of the advanced world for almost 20 years now – even falling per capita GDP might not be consistent with much or fast easing in capacity pressures.

But a fall of 3.5 per cent in real per capita GDP over the last twelve months probably deserves more attention than it has been getting thus far (even if headline unemployment has still been quite low).

With both the annual and quarterly national accounts data having come out recently it is time for a quick update of some old charts.

First, labour productivity (real GDP per hour worked). This chart is from the period since just prior to Covid, and for both New Zealand and Australia

If you want some slight consolation, at least we haven’t lost any ground relative to Australia over this period, but for both countries it is (on current readings) almost four wasted years, with no economywide productivity growth at all.

And whereas Australia’s terms of trade have risen by 11 per cent over that period New Zealand’s have fallen by about 5 per cent. That’s an additional income difference in their favour of 2-3 per cent.

(NB for resident UK pessimists, note that on current readings the UK has done less badly on labour productivity than either New Zealand or Australia over the Covid/inflation period.)

What about the longer-run series? This one is since just prior to the last big recession.

Pretty dismal productivity growth in both countries - less than 1 per cent per annum on average over the full period – but, as usually, we have done a bit worse than them over the full period. Note that although Australia is much more productive on average than New Zealand, it is also well behind the global frontier advanced economies.

Here is another of my longstanding charts, an inevitably crude breakdown of GDP (per capita) into tradables and non-tradables components.

First, covering the entire period back to 1991

and then just for the Covid/inflation period, when the gap between the two lines has widened markedly (as you would have expected initially) and (so far) stayed wide.

On this measure, per capita (real) tradables sector production now is about where it was almost 30 years ago and is about 15 per cent less than it was at the peak 20 years ago.

And then one final graph. This one shows (nominal) exports as a share of GDP

Total exports as a share of GDP have recovered somewhat after the Covid border restrictions but to a level (share of GDP) not seen pre-Covid since 1972 (off this chart, but using SNZ annual data).

And somewhat to my surprise, it is goods exports - not materially hindered by the border restrictions of 2020-2022 – that look really weak, now making new multi-decade lows as a share of GDP. Perhaps one shouldn’t have to say it: exports aren’t special. But successful economies tend to be ones where firms find more and more opportunities (and more firms find those opportunities) to take on world markets and succeed. The economy’s problems can’t be solved by exporting per se (which would be to put the cart before the horse), but successful and competitive economies will typically have a lot of firms succeeding internationally. New Zealand, by contrast (and for all the individual success stories that can be found) is an economy that seems to have become increasingly inward-oriented, increasingly less successful competing internationally. And these aren’t just narratives about one government, or one term in office; they are multi-decade failures.

But each government bears responsibility for their acts of commission and omission, and we now have a new government.

Sadly, there is little sign that senior ministers have absorbed just how poorly things have gone in New Zealand - and were doing when the National Party was last in office - or to have any driving commitment to much better outcomes, or (and the two are no doubt related) any driving narrative for what has gone wrong and what might make a difference. And, of course, there is little sign of an engaged and energetic bureaucracy offering the sort of analysis and advice that might, just possibly, engage a minister or Prime Minister who one day wondered what sort of economy their kids and grandchildren might inherit, if those generations are rash enough to stay.

For reference, and least those Australia comparisons at the top provide some sort of excuse for do-nothing complacency, recall that over the last 10 years half a dozen countries have gone past us on the OECD productivity (GDP per hour worked) league table.

When the Reserve Bank MPC came out late last month with its last words on monetary policy before its extended summer break, my post then was headed “Really?“. It was a commentary on the disjunction between the Reserve Bank’s inflation forecasts on the one hand, that showed quarterly inflation collapsing (not really too strong a word for it) over the next few quarters, and on the other hand the Bank’s OCR projections that showed a better than even chance of a further OCR increase early next year and an OCR at or above current levels well into 2025.

It wasn’t as if the Reserve Bank even gave us a compelling story as to why (a) they expected inflation to be just about to collapse or b) why they were talking in terms of further OCR increases. It just didn’t make a lot of sense, and they seemed doomed to be wrong on one count or another. And here remember the lags (something the Governor himself reminded people off in his press conference): whatever core inflation is going to be by the middle of next year is (unknown but) baked-in already. Changing monetary policy would make little or no difference to most of next year’s inflation.

Now, it is quite fair to note that there hasn’t been much sign so far in the official CPI data of the core and persistent parts of inflation coming down much, if at all. As ever in New Zealand, things aren’t helped by infrequent and lagging data (our last comprehensive CPI data are reading things as at mid-August). Neither the trimmed mean nor weighted median measures are done on seasonally-adjusted data (SNZ, please fix this), but the latest quarterly observations for both measures were about the same as in the September quarter a year earlier. We do have a seasonally-adjusted quarterly non-tradables inflation data, and the latest observations are down from the peak, but the September quarterly inflation rate was still no lower than June’s. There is enough in those official data to suggest core inflation has definitely peaked - which isn’t nothing - but having gotten things so wrong a couple of years ago you can understand why MPC members might still be a little nervous if they were just looking at the CPI (although if you were really that nervous why project such a sharp fall in inflation so soon?)

The issues are compounded for the Reserve Bank - and anyone else trying to make sense of what is going on now and what might happen soon – by the fact that two big and powerful countervailing forces have been at work. On the one hand, we had the OCR raised by 525 basis points in little more than 18 months, an usually large move in such a short space of time (the only move really comparable was in 1994 - focus then on the 90 day bill rate). And, on the other hand, record net migration inflows. In isolation one is a sharply disinflationary force while the other has added to inflationary pressures (although on the Bank’s forecasts net migration is forecast to be sharply lower next year, and if so that is likely to be a disinflationary shock). Since the Bank’s models - and anyone else’s – didn’t do very well at all in picking the sharp increase in core inflation, there is probably little reason for them (or anyone else) to have much confidence now.

All that said, it is getting increasingly hard not to think that inflation is about to fall away pretty sharply, and would keep doing so for some considerable time if the OCR were left at current levels or even raised a bit further.

There are straws in the wind from the partial (monthly) price data that SNZ releases. Indicators from the labour market suggest it is much easier to find staff (much harder to find a job) than was the case just a few months ago (at the level of anecdote I’ve been surprised by stories from my university student kids about how much problem many young people they know have had getting holiday jobs). The experience of several other countries is also not likely to be irrelevant - where inflation has also (finally) seemed to have begun to fall away faster than seemed to likely to policymakers earlier this year (and bear in mind that if the RBNZ was not one of the first advanced country central banks to raise the OCR in 2021 (it was about 7th), it was moving earlier than central banks in the US, the euro-area, Canada, or Australia.

But then there are things like the GDP data. This was from my post on Saturday

Now, it is fair to note that on some international estimates New Zealand had a larger positive output gap than most other advanced countries when inflation pressures were at their peak last year. On that basis, it might take more work - more loss of output - to get inflation back down here than in many other advanced economies. But when you have the second worst growth in GDP per capita of any OECD economy (and materially weaker, on current estimates, than the next country with its own monetary policy - Sweden) it might seem like a reasonable hunch that enough has been done. Of course, there will be revisions to come, but the December quarterly GDP release (ie last week’s) is generally the least unreliable because it benefits from the recent updates of the annual national accounts.

Now, is it impossible that inflation could stay high - or fall only very sluggishly - even if GDP (and GDP per capita, which is more important here) are very weak. In extreme scenarios of course not. But the economy hasn’t been suffering from really nasty adverse supply shocks over the last year, extreme political instability is not a feature (transfers of office happened as normally as ever), and……inflation expectations have stayed encouragingly subdued throughout the last couple of years, and are modest now. In a rag-tag sort of way the system seems to have worked (central banks messed up really badly in 2020 and 2021 - and that can’t be lost sight of – but when all the alternatives had been explored seem to have done what was required). The high inflation of the last couple of years is going to be a nasty memory for quite a while (here as elsewhere), but there is little sign anyone much thinks inflation is going to settle outside the target range.

Worriers may point to recent pick-ups in confidence survey measures. This (Westpac) one just turned up in my email inbox

Being off the lows here still leaves it not far above troughs in the most recent two severe recessions in New Zealand. All the confidence measures are still in contractionary territory, and the medium-term mood is about as bleak as ever.

One reason sometimes mentioned for why central banks would be cautious is that - after the mistakes of 2020 and 2021 - it would be quite unfortunate if they were to sound softer now only to find that inflation was hanging up and that renewed tightening was eventually needed to finally get things back near target.

As a psychological consideration it is no doubt real. But central bankers shouldn’t be purging their own “guilt” or past incomprehension by holding tight indefinitely. Rather they need to recognise those personal biases etc and correct for them.

Against that backdrop I found it useful to look back at some of the last big easing cycles that the Reserve Bank presided over. A couple of weren’t very enlightening: the increases in the OCR in 2014 were never justified in the first place so when they were finally unwound didn’t offer much. And in the mid 90s there was enough weirdness - and volatility - about the management of monetary conditions (for those with long memories, think of the Monetary Conditions Index). But I had a look at 1990/91 and at 2008. In both cases, short-term interest rates fell by 500+ basis points (in the first case, accommodated by the RB – this was pre OCR – and in the latter by direct Reserve Bank decision). In both cases, inflation had been or become quite a problem. In 1990 core inflation had been stuck around 5 per cent and the goal – a couple of years out - was 1 per cent (midpoint of the 0-2 per cent range), and in 2008 headline and core inflation had moved persistently above 3 per cent, the top of the target range (best current estimates have core inflation peaking in that cycle near 4 per cent).

Go back to 1990/91. The first negative GDP quarter was March 1991. That data won’t have been available until late in the June quarter of 1991, but by the month of March 1991 90 day bill rates had already fallen by about half (250 basis points) of that total fall that year. At that point, the most recent (December) quarterly inflation data were hardly better than they’d been a year earlier (although it was to fall away very sharply in the next few quarters). Two-year ahead inflation expectations were still about 4 per cent.

With the benefit of hindsight, if anything we were too slow and reluctant (for a long time) to let interest rates fall that year. Much as we expected inflation to fall, we (like almost everyone else) was taken by surprise be the speed and size of the fall.

What about 2007/08, when the inflation target was much the same as it is now, and the monetary policy implementation system (the OCR) was the same?

Going into 2008, the OCR was at 8.25 per cent, a level it had been raised to in mid 2007 (at the time on the back of rising international commodity prices, when core inflation had already got troublingly high). What was to become labelled as the “global financial crisis” is conventionally dated as beginning in the northern hemisphere in August 2007 but even by mid 2008 it wasn’t seen as a huge factor in New Zealand (within the Bank there were competing views) - the galvanising events (eg Lehmans) weren’t until September that year. The world oil price had peaked - at still all-time highs - a bit earlier that year.

The New Zealand economy could hardly be said to have been in fine good heart. The lagged effects of several years of OCR increases were increasingly evident. But the unemployment rate by mid year was only a little off its lows (3.8 per cent), there’d been just a single quarter of falling GDP published (and some of that had been weather-related), but the first OCR cut was in July 2008. Two-year ahead inflation expectations are the time were about 2.9 per cent (a touch higher than they are right now). I recall the MPC/OCRAG debates at the time, which with hindsight were a bit surreal as there was much discussion about whether just possibly we might be able to cut by as much as 100 basis points over the following year (actual 575 basis points, and probably should have been more).

With hindsight - and here I would put more stress on hindsight – we were too slow to start moving then. It was perhaps understandable given where core inflation was, and the difficulty of anticipating the full gory mess about to break on us from abroad, but it was too slow. But my point was that it was long time afterwards before it was clear that core inflation was actually back near target or even that the unemployment was back around some sort of NAIRU (it was early February 2009 before the Bank knew the unemployment rate had got to 4.4 per cent).

Have there been mistakes in the other direction? Of course. The 2020 monetary policy easing was clearly a mistake. But there have also been a couple of times when we (the Bank) thought we’d done enough only to have to resume tightening (one might think of 2005/6) but the message from the data now is becoming fairly clear. At some point - perhaps before too long - much the bigger risk is likely to be holding the OCR at peak for too long.

Go back a year or so and there was quite a bit of debate about what the neutral OCR might be? No one really had any idea, and in truth no really does now. But……the developments in core inflation globally (and in GDP and jobs ads data locally) given us a much stronger reason now to be confident that policy rates are contractionary than perhaps we’d have had at the start of the year. And central banks do purport to run a system that puts quite some weight on forecasts of inflation. In practice, there is less reliance than is implied by the rhetoric (and models), which reflects the fact that forecasting is hard.

In debates here and abroad about the appropriate stance of monetary policy one often sees mention of two things. First, the notion that “the last mile” might prove materially harder than the first steps downwards in inflation. Mostly that seems like handwaving, especially when the focus is – as it should be - on measures of core inflation. There doesn’t seem to be much evidence from past cycles (including in New Zealand when we were first securing something like price stability in the early 1990s) of a “last mile” problem, and it seems no more plausible this time when inflation expectations have been subdued (and when in New Zealand the exchange rate remains fairly high and stable). The other argument is that central banks need to be sure we are going to get back to target. That is an argument that puts no weight on forecasts at all. I’m not one with any particular confidence in published central bank forecasts, but in most past big falls in inflation it would have proved to be a mistake (as indeed it was two years ago when central banks were slow to tighten). As time passes, there is more reason for confidence than there might have been even six months ago. Even in principle, that confidence isn’t enough to suggest policy rates should be back to neutral - wherever neutral is - but it should be enough to suggest that less contractionary settings might be required to give one the same level of confidence one was seeking 6-9 months ago when policy rates were first approaching what now seems to be the peak. We don’t have any real idea as to whether the OCR settles at 1.5 or 3.5 per cent, but it seems most unlikely it will settle anywhere near 5.5.

I’m still quite deeply perplexed by the Reserve Bank’s stance last month (assuming that it wasn’t - and they say it wasn’t - just about playing games with markets to hold expectations up). It is less than satisfactory that (a) they’ve gone off for a three month summer break (in contrast, the Cabinet seems to get about four weeks between meetings), (b) that there are no speeches or serious interviews exploring the issues, outlook, and risk (without a Parliament there wasn’t even the theatre of an FEC hearing [UPDATE: Shortly after this post went out the RB put out an advisory that there will be an FEC MPS hearing at 8am on Wednesday}). We are left with no insight on the Reserve Bank thinking, or the range of risks, hypotheses etc they are exploring or how well they are marshalling evidence in support etc. It is our inadequate MPC on display again, summoning no confidence in them whatever even if (just possibly) somehow they are right.

If the meaningful dataflow this year is largely already at an end - hard to see the HYEFU or the micro-budget telling us much – the CPI data in late January, the suite of labour market data in early February, and the monthly spending indicators (including those banks are now producing of own customer activity) should be telling us (and the MPC) a lot. If things are as weak as many recent indicators have suggested and inflation pressures are (finally) abating fast, the possibility of an OCR cut in late February shouldn’t be thought completely impossible or inappropriate.

The quarterly GDP data were out on Thursday. Quite how one reads them probably depends on bit on where your focus lies. To the extent that the focus is on squeezing out inflation then any data that points to excess demand dissipating a bit faster is mostly a good and welcome thing. The sooner inflation is back to around 2 per cent, after three years away, the better.

On the other hand, real GDP per capita is the average real incomes of New Zealanders. And since not only did real per capita GDP fall in the September quarter but some other recent quarters were revised down there is the gloomy side to the story as well.

I put this chart on Twitter on Thursday

Looking back over recent recessions in New Zealand, real GDP per capita has already fallen by almost as much as it did in the 2008/09 recession. It isn’t that headline GDP is plummeting, but record non-citizen immigration inflows means the population has been growing at a rate not seen since 1947. This chart is from a BNZ report.

But how has per capita real GDP growth (or lack of it) here compared to the experiences of other OECD countries? The OECD doesn’t yet have quarterly per capita data for all member countries, but here is what they do have.

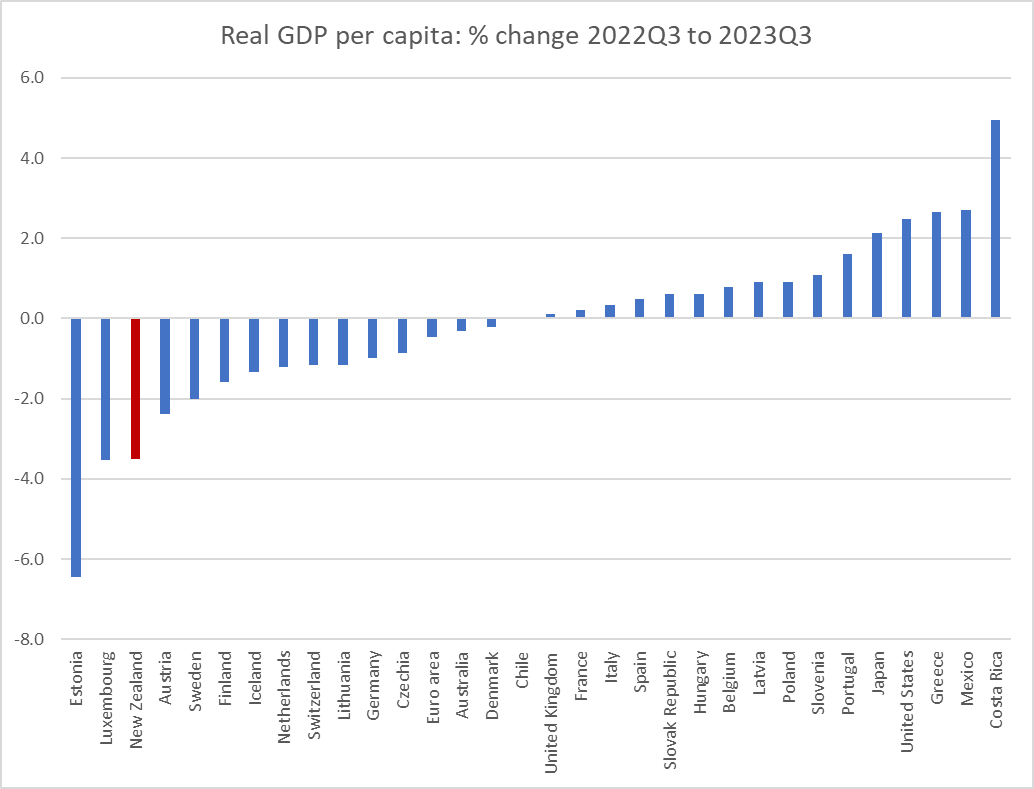

This chart shows the increase/decrease in real per capita GDP from 2022Q3 to 2023Q3. About half the countries have experienced falls in real GDP, but New Zealand’s has been the second largest fall (I’m guessing Estonia is an energy-shock effect).

And here is the cumulative change for the same group of countries from just prior to Covid (2019Q4) to now (2023Q3)

Less bad of course, but (a) less growth than the median country, and (b) bar Iceland, all the countries with a worse performance than New Zealand were severely hit by the gas price/supply shock after the invasion of Ukraine (I’m not sure what the Iceland story is, but I checked the Icelandic statistics office website and the numbers appear to be correct).

It is a far cry from the stories we used to hear - backed by data - a year or two back about the initial post-Covid rebound having been fairly strong, by international standards, in New Zealand.

I guess it will be an Act by the end of the day, but for now the short bill giving effect to a return to a single statutory objective for monetary policy is here. Yesterday’s parliamentary debate (first and second reading) is here, here, and here.

The heart of the bill is this clause

Note that this does not return things to as they were in 2018, keeping Labour’s addition of “over the medium term”. My own view is that references to time horizons are better kept for the Remit, which can be written in a more context-dependent way (sometimes it might be really important to get back to “price stability” – which isn’t 1-3% annual inflation anyway – really rather quickly. For example, after three years of inflation well above target?) With a bit more time, it might have been a good opportunity to simplify the 1989 bit of the wording as well. Simply “maintaining stability in the general level of prices” would be an improvement. But those are second and third order issues about this symbolic legislative change.

My bigger concern is that the legislation is not a complement to substance but a substitute for it. There is nothing wrong at all with symbolic steps, but if done in isolation they quickly come to seem like cosmetic distractions.

Take for example the Minister’s first reading speech

The bill is certainly a symbolic statement, but on its own it is nothing more than that. What is more, the Minister really should know that. There is nothing in the amendment that will, on its own, be “remedying one of the greatest stains of the outgoing Government and that is the stain of the cost of living crisis”. And there is nothing else even hinted at in the speeches from either the Minister or her associate (Seymour).

There has been a massive monetary policy failure in New Zealand in the last four years by the Reserve Bank of New Zealand (similar mistakes were made in many other advanced countries, but each operationally-independent central bank is responsible for its own country’s inflation rates). But, in part because there is a wide range of statutory legislative goals across countries and most of them ended up making much the same (really serious and costly) mistakes, it simply is not plausible to believe that things would have been materially different had that new “economic objective” been in place rather than the one that was actually on the statute books. There is no evidence at all to suggest that the monetary policy easing in 2020, the huge highly-risk LSAP punt, or the sluggish tightening in 2021 and early 2022 would have been any different at all, since the Reserve Bank’s own forecasts at the time (2020 and 2021) suggested to them that if anything what they were doing wasn’t really quite enough to keep inflation UP to the target midpoint.

This is all familiar ground but it is inconvenient ground (it appears) to the Minister who seems more interested in the rollicking political theatre of blaming her predecessor for his symbolic statutory amendment than in fixing our decayed and failing central bank. I read her speeches yesterday in both the first and second reading debates and there is no hint there that this statutory amendment is a first step in a process to fix the Bank or even to insist on some effective accountability for those whose decisions visited highly costly inflation and $12 billion of losses to the taxpayer on us. They used to talk of launching an independent review of Covid-era monetary policy. I was never entirely convinced of the case for such a review, and as I noted here recently if it is done the choice of reviewer will probably pre-determine the character of the final report, but it was a fairly consistent line from National. But there is no mention of it in yesterday’s speeches (the speech from the Associate Minister seemed more focused on the inflation of the Roman Empire than in actually fixing New Zealand’s central bank now).

The Minister (and her predecessor as Opposition finance spokesperson) has on several occasions been lied to by the Governor at FEC. The chair of the Board appears to have gotten away with lying to The Treasury, and getting Treasury to run spin for he and his Board have banned experts from serving as external members of the MPC. No external members have made even a single speech on monetary policy and inflation in their almost five years in office. The Board is stacked with underqualified mates of the previous government – a couple appointed despite, at the time, clear conflicts of interest, suggesting that not only the previous Minister but also the Governor and the board chair have at best a hazy sense of high standards in public life. Hardly anything is ever heard from the Governor on inflation – speeches from him on climate change are more common than those on the conduct of monetary policy. The Reserve Bank publishes little research, and is a bloated top-heavy regulation-fond expensive bureaucracy.

Not all of those failings could be fixed overnight even if the new government were so minded. The problem is that there is no sign at all that they are seriously interested in fixing any of them. This from a Minister and Associate Minister who did not support the reappointment of the Governor – a serious step for them to have taken then, but apparently meaning little now. There is no hint also that the Minister is going to reopen the selection process for the two external MPC roles falling vacant early next year. If she simply takes nominees who got through the Orr/Quigley/Board and Board recruitment agency process undertaken earlier this year, under the broad aegis of the previous government’s priorities/views, it is a recipe for things being no better in future. Either the nominees she is presented with will be amiable non-entities happy to be guided by the Governor, or (at best perhaps) people who were willing to keep their heads down and say not a discouraging word through the last four years of central bank failure.

Perhaps I’m being too critical too early? But if the Minister is at all serious about things being done differently in and by the Bank, yesterday’s speeches would have been a great (and easy) opportunity to have signalled something. It also hasn’t been too early for some other ministers to have written letters of expectation to agencies for which they are responsible, making clear the new government’s priorities around those agencies. But there seems to have been nothing from Willis.

Instead we get examples like this of her economic thinking

As economic thinking, the final sentence is a little embarrassing. There is little or no reason to suppose that there is any medium to long relationship (positive or negative) between the inflation rate and the unemployment rate (or “maximum sustainable employment”). One can have highish inflation and (sustainably) low unemployment or one can have low inflation – even price stability – and (sustainably) low unemployment. The record – across countries and across time – is pretty clear. But inflation – and especially unexpected bursts of inflation – is something the public dislikes, and for good reason. Getting and keeping sustainably low average rates of unemployment should be an important concern for governments, but Reserve Bank monetary policy has little or nothing to do with such outcomes.

Unfortunately there is quite a lot of muddled thinking around monetary policy and the expression of objectives. I could only agree with this line in the Minister’s first reading speech

Flexible inflation targeting, whereby the MPC has regard to the impact of monetary policy on the broader economy when determining how quickly to return inflation to target has been central to New Zealand’s successful inflation targeting regime for many years, and was the case prior to Robertson’s dual mandate hitting the books, regardless of whether there is a single or dual mandate, that remains the case.

and in fact giving expression to that generally shared understanding was one of the motivations for Labour’s legislative change in 2018. But, of course, the issue was never primarily about demand shocks and forecasting errors – like those of the last few years – that delivered us high inflation and unsustainably low inflation at the same time. Failures on the scale we’ve seen recently were simply never envisaged (and should never have happened). By contrast, supply shocks – that tend to drive headline inflation one way and unemployment the other way – aren’t infrequent at all and were always actively envisaged in the design and modification of Policy Targets Agreements over they years. In the face of such shocks it has always been the shared, usually expressed, understanding – and this dates all the way back to the oil shock in 1990 just a few months into the life of the 1990 Act – that faced with such shocks it would generally not be sensible or prudent to attempt to counter the direct price effects immediately, and that to do so would involve unnecessary and undesirable employment and output costs. There isn’t much of a sense of this in the Minister’s speeches – perhaps understandably as it veers to the geeky – but it is important nonetheless.

Finally, approaching the end of this post I wanted to offer a few thoughts on the Treasury’s Regulatory Impact Statement on the removal of the “dual mandate” from the Reserve Bank Act. At five pages long it is perhaps the best advert for the government’s decision not to require RISs for early pieces of legislation that are simply repeals. It leaves readers no better informed on the issues, offers no serious analysis, and actually muddies the ground in places. On the latter, for example, it correctly notes that Reserve Bank and Treasury view that the different mandate made no difference to policymaking over 2019 to 2023 (when the dominant shocks were understood to be demand shocks, likely to affect core inflation and unemployment in the same direction) but simply never engages on supply shocks (see previous paragraphs) or the flexibility long built into both central banking practice and the succession of Policy Targets Agreements. Since the political debate has further muddied this water – reinforced by half-baked media lines (of the sort I heard on RNZ this morning – it might be desirable for the new MPC Remit to make some of this stuff explicitly clear. There are short-term tradeoffs, but no long-term ones.

The RIS also repeats and endorses – and perhaps fed the Minister – the line that price stability is a “prerequisite” for achieving other objectives. It simply isn’t, and Treasury really should know better than to indulge what is not much more than misleading political rhetoric.

In RIS it is customary – perhaps even required – to look at three different ways of responding to the identified “policy problem”. The artificiality of this was never better displayed than in the Treasury RIS, in which they treat as a serious option using the reserve powers in the Act allowing the Minister of Finance to override temporarily the existing statutory economic objective, rather than amending the Act. Unsurprisingly, they recommend against using these never-used (dusted off for refreshing the memory every decade or so), which should never have been considered as an option in the first place – as not only would the market signalling have been terrible, but it would have gone quite against the direction the government was seeking (a permanent change).

Treasury ended up opposing the government’s legislative change, preferring to change just the MPC Remit (which the Minister can do pretty much any time he or she likes). Their only argument for this – eg they don’t seem to invoke any argument about reminding readers of statute of the wider context, or even that it is the Remit not the Act that is supposed to guide the MPC – seem to be a preference not to amend the Act (as if not amending the Act was a good in and of itself). They say “Treasury puts significant weight on the value of a stable and enduring legislative regime for the Reserve Bank” which (a) is weird coming immediately on the back of several years of extensive legislative overhaul around the Reserve Bank, (b) could be as easily seen as an argument for the government’s legislative amendment, which is closer to the “stable and enduring” legislative model that prevailed for almost 30 years, and (c) assumes recent reforms generally got things right, when there are clearly significant problems with the way the Reserve Bank Act reforms were done (including but not limited to making the underqualified board, which has no expertise in monetary policy, primarily responsible for holding the MPC to account and in appointing MPC members and the Governor).

Finally, Treasury seeks to invoke “international best practice” in defence of retaining Labour’s wording. In respect of legislative (or similar wording) they are simply misleading. All four of the most important advanced country central banks – Fed, ECB, Bank of Japan, and Bank of England – have a single statutory objective, even if often accompanied by wording designed to articulate something of why price stability matters. It is certainly true that some central banks have more explicit “dual mandate” wording and others talk openly about the interactions between inflation and employment, sometimes in “dual mandate” terms, but there is nothing out of step with the legislative amendment the government is putting through today. The Treasury explicitly tries to cite the US in its support, but while the Fed likes to talk “dual mandate” rhetoric, its actual statutory objective for monetary policy is (a) a single objective, and (b) one with very outdated – legacy of the 1970s wording.

“So as to” are the envisaged benefits of pursuing and achieving the specified single objective.

It was simply far from being Treasury at its finest, and if time was short there was no obstacle to writing a much better short paper.

As for the government it is early days, but the early signs are not great around the Reserve Bank. I’m quite prepared to believe the new government won’t accommodate more institutional bloat, and that their appointments will be no worse than those of their predecessors, but for now there are no signs leading a reasonable independent observer to expect anything much better about fixing the Reserve Bank (or our diminished Treasury for that matter).

UPDATE:

This is from a speech by the minister at the committee stage

The problem is that she contradicts herself. There are forms of inflation targeting where accountability might be really easy – any time CPI inflation is outside the target range, sack the Governor – but everyone has been agreed for 30+ years that that would not make sense and would generally produce inferior economic outcomes. In fact, the Minister herself agree because she is at pains to point out that the flexible form of inflation targeting (operated for the first 30 years) will be retained. In such a system it is not easy or mechanical to be able to exact accountability. These things -as so often in life – require judgement, and a willingness of ministers to exercise such judgement and, on rare occasions, act accordingly. Grant Robertson failure to do anything – and his decision to reappoint Orr and the 3 externals – is what made him party to their (central bank) failure.

Yesterday’s Sunday Star-Times had an article built around some comments from me and from Infometrics economist Brad Olsen on the economic prospects of Wellington. The headline captured the gist of my contribution, “Sorry, Wellington, things could get worse and they probably will”.

The question the journalist, Kevin Norquay, had posed to me a week ago was about the impact of the government wanting to cut numbers of public servants and consultants, all in the context of a CBD where working-from-home seemed to be taking its toll [perhaps, although it is quite hard to park in The Terrace carpark at even 9am these days] and the Wellington city council was struggling to get enough revenue to maintain basic infrastructure.

My starting point is that Wellington is not in a good way and that, absent serious steps to fix itself, slimming down the public sector (if sustained) only worsens the plight of a city that few private businesses not dependent in one way or another on the government (or its subsidies, see the film sector) now choose to base themselves in. After all, as alternatives there was the big city (Auckland), the much-cheaper similar-sized city (Christchurch) or, increasingly, Hamilton or Tauranga.

Olsen, who is reported to be a member of the Wellington Chamber of Commerce, has a more optimistic take

Perhaps he had in mind the top of Mt Everest as in inhospitable place that few get to, and none stay longer than they really need to, where nothing grows, and most humans who make it need additional oxygen?

I’m not sure quite which of my comments Olsen was shown, but his comments seem quite cyclical in nature. And by most standards the last few years have been good for Wellington – it doesn’t export much and it does depend on the fiscal spigots being turned on. And that is more or less the story of the last few years.

But my points were set more in the context of longer-term decline. For example, this chart showing how GDP per capita in Wellington (regional council area) compares with that in the country as a whole, from a post earlier this year.

The trend decline is, large, clear and (as yet) unbroken. Sure, average GDP per capita here is still higher than the national average, but that seems to be largely because Wellington is a big head office town of a entity that isn’t subject to any sort of market test. Much of central government is complex and needs specialist support services etc, and those sort of roles will naturally pay above average. In principle, GDP is measuring value-added, but in a central government function that is largely just what the government pays people (there is no market test for the outputs). The externally-facing private market has increasingly gravitated away from Wellington.

Which isn’t that surprising when the climate is blah at best (yes, temperate sounds good, but that just means really hot days in summer are very rare. Oh, and the wind…..), house prices are punishingly high, almost everywhere you turn there are water leaks, while the councils seem more interested in really expensive vanity or ideological projects (be it the Wellington Town Hall, a heavily-subsidised convention centre, or the endless cyclelways) than in doing any of the basics well. Did I mention that the regional council is keen to stop new greenfields development of housing, and the local authorities mostly seem very much in tune with that sort of approach. Even by New Zealand standards Wellington is a long way from anywhere (90 minutes from Christchurch gets you to Mt Hutt, but 90 minutes from Wellington gets you to Masterton and Levin. 10 minutes from Tauranga gets you to the Mt Maunganui beaches). Oh, and latterly it seems we have a public drunkard as mayor of the largest local government unit in the region.

Wellington once had one big thing going for it: a large, deep, and safe harbour. That mattered a lot in the 19th century. It was still a significant asset in much of the 20th. I looked up an old New Zealand Official Yearbook on my shelf and found this overseas trade data. This was the import data by port

and this is exports (note the comment in the previous picture re exports via Tauranga)

Twenty years on Wellington was still the second largest port for foreign trade. But that was then. These days, by contrast, you struggle to spot Wellington port data (and at that the port doesn’t cover its cost of capital, at cost to ratepayers).

Of course, there are services exports these days as well. Wellington is well-known for the heavily taxpayer-subsidised film and related industry, but not so much for viable private businesses making it on their own (just recently the council’s “economic development” arm was clamouring for subsidies for gaming firms lest, horror of horrors, those firms relocate to Christchurch, where the climate is better and housing much cheaper).

In my comments to the journalist I noted that Wellington will always be a bit of a magnet for young graduates who want some years under their belt working for central government. But how many will really want to stay when housing is impossibly expensive, rates bills are spiralling. And these days, Wellington is so expensive that not even the presence of government and the much-vaunted Cuba St generates enough of an inflow of university students to sustain the sort of courses you might think natural in a capital-city university (the way it liked to market itself). When I was young all but one of the our economics honours class moved into public sector jobs. These days – the need for expertise being no less – Victoria can no longer sustain a proper economics honours programme.

The SST article ended with these comments from me

I guess there is nothing very wrong with being a Canberra, but that isn’t the story local government figures and other worthies like to tell themselves. They like to tell themselves tales of a vibrant private sector, a tech hub etc etc, but the data don’t really support their story. And why would it? Wellington isn’t a big city, not even by New Zealand standards. It is remote and expensive and ill-governed.

It could do things differently to give it at least a bit of a better chance. Its local government could, for example, commit to making housing abundant and affordable – cheap houses, cheap rents. That doesn’t mean building them themselves, or deciding where they should go, or what they should look like, but simply freeing up the land – all the land – and making it easy to build. Instead we have ideologues of intensification (NB, there is nothing wrong with intensification if that is what individual purchasers want), even though intensification as goal has simply never worked to collapse, and keep low, house and rent prices anywhere.

The Council could move to strip out the savage rates differential that acts as a hefty tax on private businesses operating here. No doubt those costs are passed through – in one form or another often back to government, the captive industry – but, as with corporate income taxes generally, when you tax heavily something that is mobile (and most outward-oriented services sector businesses have choice) you get fewer of them.

Perhaps there was some golden age of Wellington (100 or more years ago) when government was relatively small, direct subsidies few, and Wellington wasn’t that much smaller than Auckland. But those days are a very long time ago now, and the recent sugar rush (lots more public servants under the recent Labour government) don’t disguise the fact of Wellington’s decline.

Sorry, Wellington, things could get worse and they probably will. And that is even though the political tides will turn again and before too many years pass perhaps there’ll be another resurgent wave of public servants and the consultancies that hang off government agencies. But it is unlikely to mask the decline of Wellington as anything other than a centre of government.

It doesn’t seem to have been the best week for the Reserve Bank since the release of the latest Monetary Policy Statement last Wednesday. Of course, one could make a pretty compelling case that in the Orr years few weeks have been, and especially not any weeks when Bank figures actually say or do anything. But for now we’ll focus just on the last week.

On the one hand there was some pretty clear pandering by the Governor to the instincts and preferences of the new government. There is nothing like losing $12 billion dollars of taxpayers’ money and delivering several successive years of core inflation well above target – with no contrition on either count – to suggest past loss of focus and energy, but we learned from the Herald that

The PM said that during his conversations with Orr on Tuesday he was pleased to hear the governor’s “obsession” with lowering inflation.

If that was really Orr’s word – and it isn’t entirely clear from the story whether it was his word or the PM’s take – and he really meant it (as distinct from just indulging in loose rhetorical pandering) it would be more than a little concerning, when central bankers (New Zealand and abroad) have been at pains for decades to explain that having an inflation targeting regime does not mean they are (in their own words) “inflation nutters”. There are many many examples, in formal literature and less, from here and abroad, but as just one local example this article from Orr’s time as the Bank’s chief economist back in the (allegedly hardline, but always actually quite flexible) Brash years. I don’t think Orr was actually serious about the “obsessive” bit, because when he was asked about inflation in the MPS press conference he was at pains to explain – sensibly – that if there were forecasting errors around how quickly inflation comes down they simply couldn’t be sensibly corrected immediately (lags and all that). But it speaks of a Governor who is simply not a nuanced and serious communicator (consistent with the near-complete absence of speeches from him on monetary policy, through a period of serious policy failures).

In his remarks last week Orr also seemed to be getting on side with the government’s stated intention of legislating to restore the statutory goal for monetary policy to price stability, noting that the Bank’s own work on the Remit review had suggested a more prominent place for the price stability goal. That was all fine, and Orr has been pretty clear all along that Labour’s change to the goal in 2018 had not made any material difference to monetary policy decisions in the last few years, and the Bank – under successive Governors (and chief economists) – has long championed its (internationally standard) flexible inflation targeting approach.

But then the current chief economist was let loose and in remarks to Newsroom is reported under this headline

as having said

which is an astonishingly loose comment from someone paid hundreds of thousands of dollars a year and holding a statutory office as an MPC member. It is no doubt true that one could set up a highly-simplified model in which some arbitrarily chosen reaction function to some specific types of shocks might end up with (temporarily) higher unemployment under one specification of the statutory target than the current one. But….not only would there be other shocks in which unemployment would be (temporarily) lower (when both inflation and unemployment are low), but there is no sign of any work or thought on whether such shocks are at all frequent, or how they were actually dealt with under the statutory goal in place here for the best part of 30 years. And, notwithstanding Conway’s comment, the monetary policy decisions that matter are almost never easy, precisely because they are about uncertain futures. Take the last time core inflation was well away from the target midpoint – in 2008 – and check how many times the Reserve Bank was tightening then. It wasn’t, of course, and was right not to have done so (whatever mistakes it (we) might have made in the previous couple of years). It might be interesting for someone to OIA the Bank and ask what evidence they have for Conway’s claim that the planned legislative amendment will result – even “at the margins” – in higher unemployment.

But all that was general high level policy frameworks stuff. What about actual policy and outlook.

In the MPS – which the Governor described as “a wonderful wise document” – the Reserve Bank again revised upwards their future track for the OCR, lifting both the peak of the track (to the point where they reckon there is a better than even chance of another OCR increase next year) and increasing quite materially the extent to which they expect interest rates will have to stay high. The further out projections have been lifted by about 50 basis points, coming on the back of similar increases at the previous MPS.

But here is the most immediate problem (from a tweet last week).

Much of the media comment focuses on annual rates of inflation. The Reserve Bank projections have annual inflation finally dropping into the target 1 to 3 per cent range – although still a considerable way from the 2 per cent midpoint the Bank is required to focus on – for the year to September 2024. Even that isn’t far away now, but in thinking about policy it is typically more useful to be looking at the projections for quarterly percentage changes in the CPI.

There is some seasonality in the CPI (September quarters are typically much higher and the other quarters a bit lower than average). Unfortunately the Reserve Bank does not publish its inflation forecasts in seasonally adjusted terms, but on this occasion eyeballing does fine. You can see not only that ever quarter in 2024 has quarterly inflation at about half what it was for 2023, and as early as the June quarter of next year (mostly measured as at mid May, so only five months away) the headline quarterly CPI increase is projected to be already 0.5 per cent. By the December quarter of next year, the quarterly CPI increase is explicitly consistent with annual inflation of 2 per cent.

And how long does monetary policy take to have its largest effects? Views differ but the standard Reserve Bank line – the reason why the Governor suggested that if they are wrong about September 2024 they can’t sensibly immediately fix things – is something like 18 months. Even if it is as short as 12 months, those inflation outcomes next year in the Bank’s projection are the result of the current OCR, not a possible increase next year. And those outcomes are entirely consistent, on a quarterly basis by next November at the latest, with the midpoint of the inflation target range.

So why would you publish projections now showing a further OCR increase next year, and no cuts below the current 5.5 per cent until mid 2025 when (a) your best projections (presumably) are that quarterly inflation will be at target next year, and (b) your routinely repeated view is that monetary policy takes perhaps 18 months to have its main effect on inflation? If anything, that looks like a recipe for keeping the unemployment rate – not expected to peak, at above 5 per cent until mid 2025 – a bit higher rhan otherwise “at the margin”.

One possibility was that it was all just about “jawboning”. In the MPC’s view markets were getting a bit over-enthusiastic looking for the first rate cut so perhaps the track was pushed up and out a bit to send a message (and yes, late messaging changes to interest rate tracks do happen). But…..even if that had been the case, why wouldn’t you also have pushed up the inflation track? After all, the Reserve Bank’s inflation projections (see chart above) show a really sharp collapse in quarterly inflation rates, starting right about now.

But two members of the MPC have been sent out to assure us, via different media outlets, that no, the Reserve Bank was dead serious, and it was not (in a Post article reporting comments from Conway) “talking tough for effect”, or (in a Herald interview with the Deputy Governor) that there were no games going on and “our messages are genuine”.

If genuine, then incoherent. If inflation is doing anything like what the MPC’s own published inflation projections are suggesting (ie very quickly now getting back to target), there is no credible case for keeping the OCR well above (assumed) neutral for the indefinite future, and not cutting at all until mid 2025.

(To be clear, I am not and never have been a fan of published central bank interest rate projections, or any medium-term central bank forecasts – the state of knowledge is so limited that anything is more about messaging and game playing than any real information – but it is the MPC that chooses what it publishes.)

The story really doesn’t add up. Nor is it particularly compelling to suddenly start playing up fiscal pressures on demand (nothing having changed on the expansionary side around fiscal policy settings since the May Budget, and the Governor repeatedly played down demand effects in May and August – when it suited the government of the day for him to have done so). One could say something about immigration pressure (when the huge surge in net non-citizen arrivals has been evident for many months) altho the near-term estimates of the inflow have been increased.

But that big shock – the additional net arrivals – has already happened (quarterly this year), and yet the MPC tells us the think the inflation rate is just about to collapse, on current monetary settings.

Up to this point I have not taken a view on whether the Reserve Bank’s inflation forecasts are likely, just highlighting the tension between what are really quite rosy inflation projections, and that OCR forecast track – and the rhetoric- which is anything but.

The Reserve Bank has also been at pains to make the (obvious) point that they have to set monetary policy in the light of the New Zealand inflation outlook and that whatever is going on in other countries is not necessarily a great guide to what will be required in New Zealand. Which is all true, but…..much of what has gone on around inflation in the last three years has been fairly common to a whole bunch of advanced countries. There were, of course, the largely common supply shocks – ups and downs of oil and freight prices etc – but more importantly excess demand pressures, and extremely stretched labour markets, also became apparent in many countries. And if our fiscal policy looks to have been a bit more expansionary than in most, the biggest demand effects of that seem set to have been in 2022 and 2023 rather than beyond. The surge in immigration has certainly been huge – and my standard model for a decade has emphasised the positive net short-term demand effects from migration but (a) similar things have been seen in Australia and Canada, and to a lesser extent in countries like the UK, and (b) the Bank’s forecast assume quite a sharp slowing (annual net immigration next year is forecast at half the rate of this year.

In a post a few weeks ago I highlighted that on IMF estimates New Zealand had had the biggest excess demand (positive output gap) problem of pretty much any advanced country. If so, that would be a reason for caution, why inflation might be tougher to beat here than elsewhere (and it is true that our OCR is only around those of other countries, whereas in most past cycles it has had to go higher). But the OECD’s recent forecasts, out last week, suggest a picture that has New Zealand’s experience closer to the pack for this year and next.

What has happened then to (core) inflation in other advanced economies?

There are positive stories (US and euro area getting a fair number of headlines)

Each of those current annual inflation rates are materially below New Zealand, and the quarterly/monthly data are often more favourable.

In the Nordics, perhaps a mixed picture

but even then if one looks to the Norges Bank’s core indicators things seem to be heading in the right direction.

And even in the central European countries there has been a big reduction in core inflation (with a long way to go)

None of this is any guarantee that any of these countries will get to 2 per cent quickly, but the direction seems pretty clear, and it isn’t really obvious why it would suddenly become so much harder to cover the last mile. Nor, thus, is it really apparent why things will prove so much different here – when the RB itself tells us they think inflation is just about to collapse. It wasn’t as if there was any serious sustained analysis in the MPS itself to explain a) why the Bank expects inflation is on the brink of collapsing, or b) why they are really reluctant to believe their own numbers. Sure, the Governor was heard to mutter things about inflation expectations – even, bizarrely, suggesting that 10 year ahead numbers were some sort of personal blow, when we know the Governor will be gone in 4.25 years at most – but the best predictor now would have to be that if headline and core inflation fall away sharply, as the Bank tells us it expects, survey measures of inflation expectations will follow.