When it comes to Long-term Insights Briefings (LTIBs) I sympathise with the public service, I really do. The requirement to produce these documents was introduced by the previous government in fiscally expansive times (core government agency staffing growing rapidly). Even then, it was a fairly flawed idea but if agencies were awash with cash I guess they might as well try to do some analysis. These days, even if the fiscal deficit is not being cut, core government department spending is under considerable pressure, and we have a track record in which the LTIBs that have been produced have rarely added much value. I gather the current amendments to the Public Service Act will eliminate the requirement to produce LTIBs but…..for now government department CEs and acting CEs still have to comply.

A year or so ago MBIE and MFAT decided to get together and produce a joint LTIB this time round. As the law requires they consulted on the proposed topic

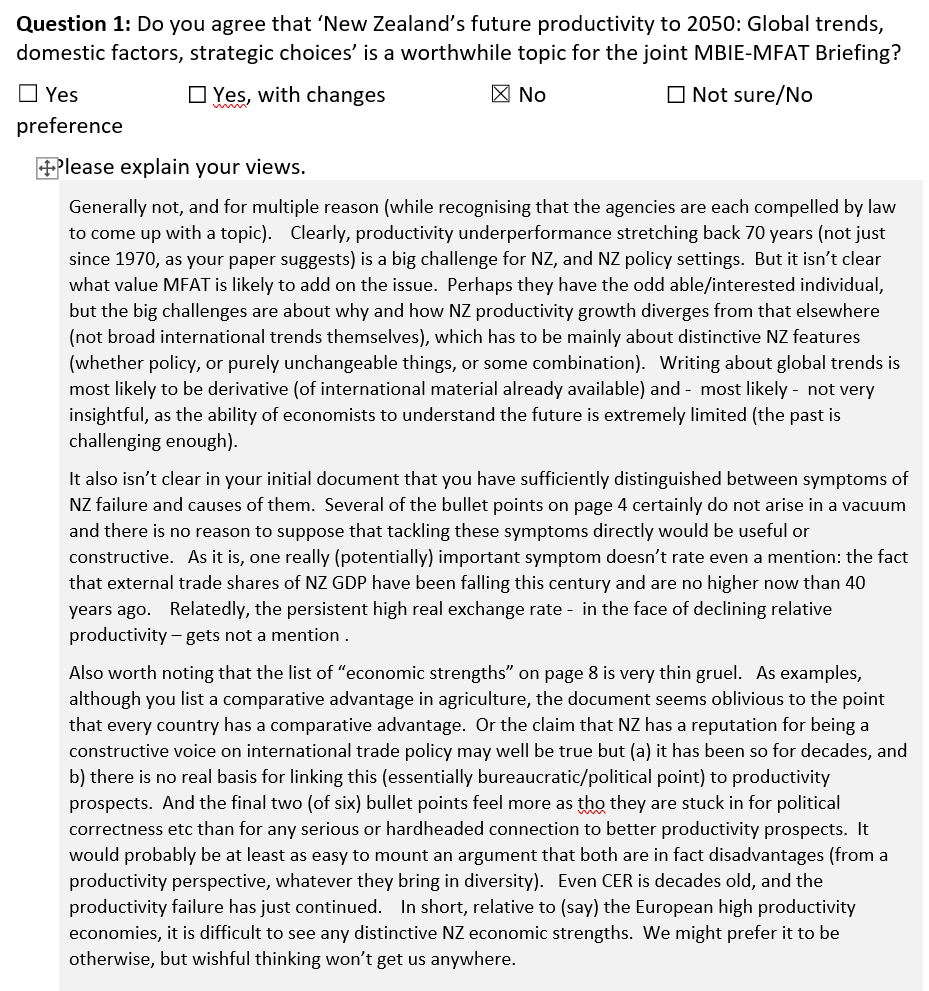

I put in a short but fairly sceptical submission on the topic

Anyway, the bureaucrats have beavered away and last month come up with a draft LTIB (on which submissions close next Monday). They must have refocused their efforts somewhat following consultation on the topic as it is now presented this way.

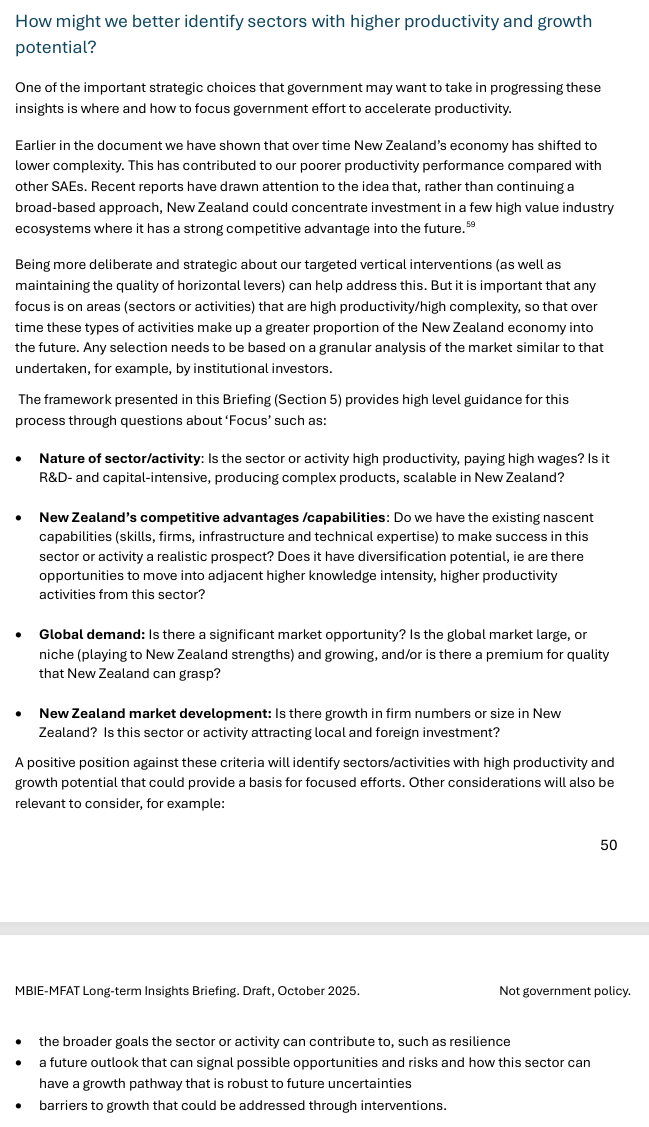

Having made a submission last year they’d included me on their general email inviting submissions on the draft. I’ve been away and otherwise busy and hadn’t really intended to even look at the thing, but there was another reminder yesterday so I took an initial look. It was the “accelerate the growth of high productivity activities” that prompted me to look a little further: the focus apparently was not economywide productivity and policy settings but the sort of “smart active government” stuff MBIE has long championed, involving clever officials and politicians identifying specific sectors to focus on and specific interventions to help those sectors. And, of course, lots of preferential trade, investment, etc agreements (the ones MFAT likes to call Free Trade Agreements). On a day when the dysfunctions of our public sector were on particularly gruesome display it seemed even less appealing and persuasive than usual. In a month when the government had been a) buying a rugby league game, b) increasing (again) film subsidies, and c) subsidising expensive New Zealand restaurants (via the Michelin corporate welfare), all in the name apparently of “going for growth”.

So I decided to sit down and read the draft document after all. It isn’t that long (45 pages or so excluding Executive Summary, glossary, references etc), reflecting no doubt the fact that LTIBs are a compliance cost for agency CEs rather than really core top priority claim on resources. Before reading it I heard on the grapevine last night of a smart person who had opened the document, read the first page, rolled their eyes, and closed the document again. But I persevered….and there is 25 minutes of my life I won’t get back.

Sadly, but perhaps not surprisingly, the draft report is unlikely to be any use to anyone looking for illumination rather than support (the old two uses of a lamppost line).

On New Zealand, we get a fairly long list of symptoms of our relative economic failure, but no serious attempt at analysis of the causes. If you don’t understand the causes, including the roles (positive or negative) of past policy interventions/choices, it is really difficult to see how you tell a compelling story about solutions, unless the document is just a prop for a longstanding predetermined narrative and set of policy preferences.

They then introduce a series of four small advanced economy “case studies” – a page each on Denmark, Finland, Ireland, and Singapore. Not only do they not engage with a really important difference between New Zealand and these countries – ie extreme remoteness – but there is no attempt to understand what drove the successes of these economies either. In each case there is a list of types of interventions that have been or are being used in these countries but no effort at all to assess what role (positive or negative) these interventions have played in contributing to medium-term productivity growth. It certainly isn’t impossible that some might have been helpful, some will almost certainly have been harmful (just consider the range of interventions our governments have tried over the decades), and perhaps many will have just been ornamental or redistributive – not really making much difference at all to the productivity bottom line. And I’m pretty sure that not once in the entire document is there any suggestion of the possibility of government failure, capture etc.

Then the draft report moves on to four domestic case studies (this time roughly two pages each), looking at the dairy industry, space and advanced aviation, biomanufacturing, and the Single Economic Market (mostly Australia but also beyond) with a focus on sector-specific interventions. None of it seems to display any scepticism, only a sense that we (governments) haven’t been sufficiently focused or willing to persist with particular sector supports. Strikingly, in the dairy “case study” there is no mention of the rather large role the government played in enabling the creation of Fonterra, and how the results have, to put it mildly, not exactly lived up to the promised hype.

And the whole document ends with a question that shouldn’t even be being asked by government departments.

But perhaps it is all music to the ears of governments that like specific announceables from week to week? (Whether MBIE or MFAT like those specifics is another matter – quite possibly not, but their mindset and fairly shallow analysis in documents like this helps provide cover for governments more ready to paper over symptoms, toss out some cash to favoured firms/sectors, and avoid insisting that the hard structural issues are identified and addressed).

And this sort of stuff helps keep lots of officials busy and feeling useful.

To any MBIE/MFAT readers, no I won’t be submitting, but I’m sure you get the gist. The sooner the LTIB requirement is removed from the law the better, but eliminating that won’t change the mindset. As far as MBIE is concerned, my ongoing unease was only reinforced when on the page with the consultation document on it, this was the list of tabs/items down the side of the page under the heading “Economic Growth”.