I didn’t have too much problem with either the Reserve Bank Governor’s speech a couple of weeks ago on a framework for how monetary policy might deal with the oil shock, or with this week’s OCR review release from the Monetary Policy Committee. It was really all very orthodox stuff, much as any of the previous Reserve Bank Governors over the inflation targeting era might have said. Almost always, you will let the first round (direct and indirect) price increases through – as major relative price changes, and as happening too soon for monetary policy to do anything much about anyway – and then keep a very close eye on what happens beyond that to the generalised medium-term inflation outlook (where the pressures can be conflicting – weaker economy on the one hand, and potentially higher “true” inflation expectations on the other). And, of course, when the oil shock hits, no one really knows how long the disruption and associated price effects will last, and that matters.

A comment that was passed to me yesterday expressing concern that the MPC might be going soft on inflation risks, they having mentioned the potential near-term growth implications of the shock (which could yet be savage, given how low the price elasticity of demand for diesel is), prompted me to go and dig out the Monetary Policy Statement the Bank issued in the wake of the first oil shock of the inflation targeting era, that prompted by Iraq’s invasion and occupation of Kuwait on 2 August 1990.

That invasion caught most of the world flat-footed. It complicated life for us too. We’d just issued a small tightening statement on 1 August, which hadn’t made us at all popular with a government that was facing a crushing defeat in an election now only a couple of months away. We tightened again – different system then from today’s OCR – on 3 August, and when mortgage rates rose that day the (normally sensible) Minister of Finance was reduced to calling the banks “mean” and claiming they were out to get the government. We were also just a couple of weeks out from the scheduled release of our second Monetary Policy Statement (editorial and production processes were a lot more protracted then than now, and the documents weren’t forecast focused), for which the team I managed was responsible. We pretty quickly realised that we needed to postpone the MPS by a couple of weeks and I spent a harried few days rushing out a substantial redraft, centred now on the oil shock policy issues.

Oil price shocks, of course, had not exactly been unknown to this point. In fact, the two dramatic ones to that point (1973 and 1979) were only about as far back in history then as 2007/08 and 2022 shocks are now. And in devising the inflation targeting framework, and the formal Policy Targets Agreements between the Governor and Minister, we’d been careful to think hard about how to handle supply shocks of that sort. And we had discussed specifically an oil shock scenario in our first Monetary Policy Statement in April 1990.

Folklore sometimes has it that the Brash Reserve Bank was full of utter zealots and nothing, but nothing, would ever allow us to deviate from a narrow path to price stability, and certainly not any considerations of output or employment. It simply was not so, whether in conception, or in practice. There were numerous examples during the early years, but this is a particularly clean one.

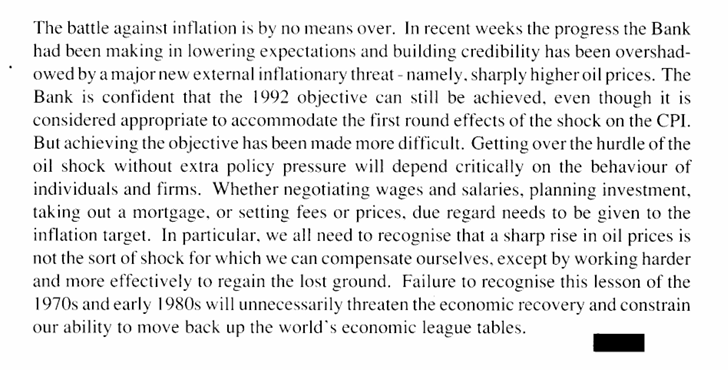

Here is what we had to say in the Monetary Policy Statement finally released at the start of September.

Whereupon the extract (above) from April was repeated, before the discussion continued

Reading that final sentence, there is a certain similarity to much current commentary…..

And we ended the entire document this way

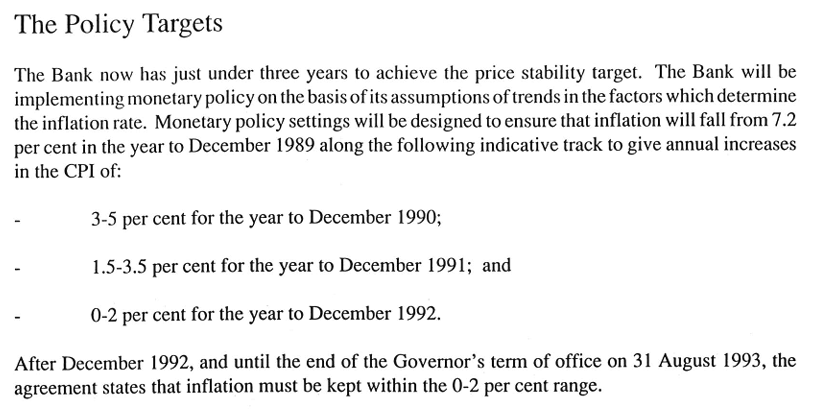

Our monetary policy approach then was right, and flexible, and not at all reluctant (my diary, for example, records a senior-level meeting on 7 August where we agreed, without apparently any significant dissent, that even the 1991 indicative target range for inflation on the path to price stability (announced here in the April MPS) should probably be increased (there was later a formal adjustment, in agreement with the Minister)).

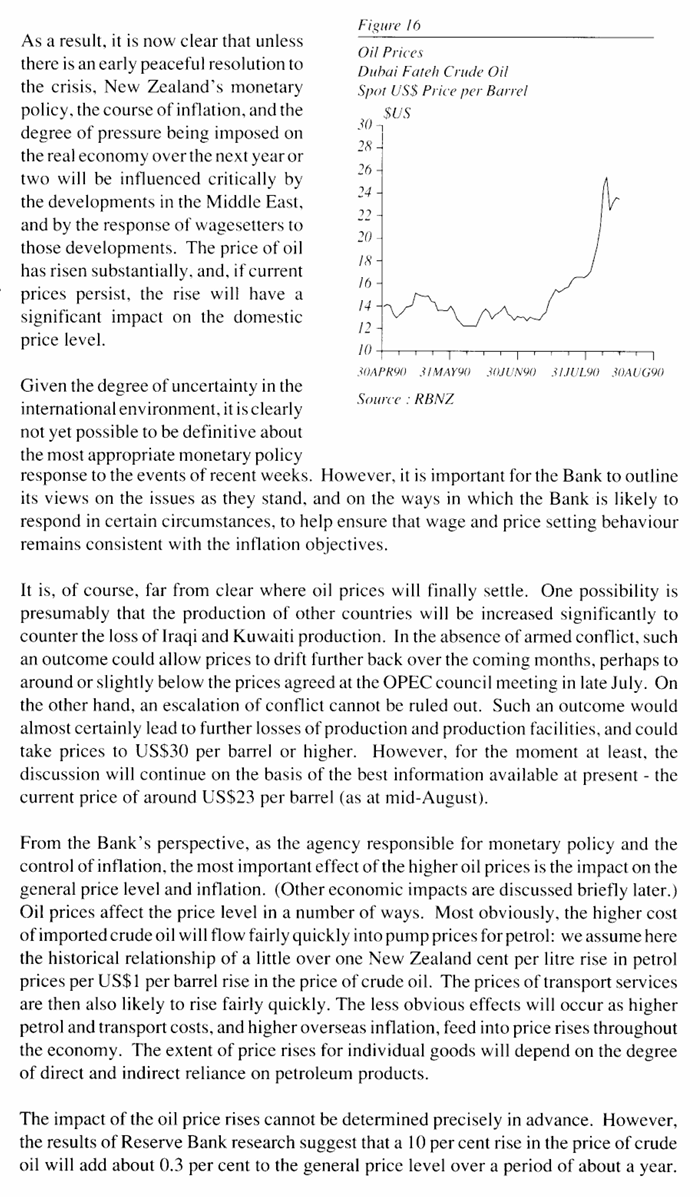

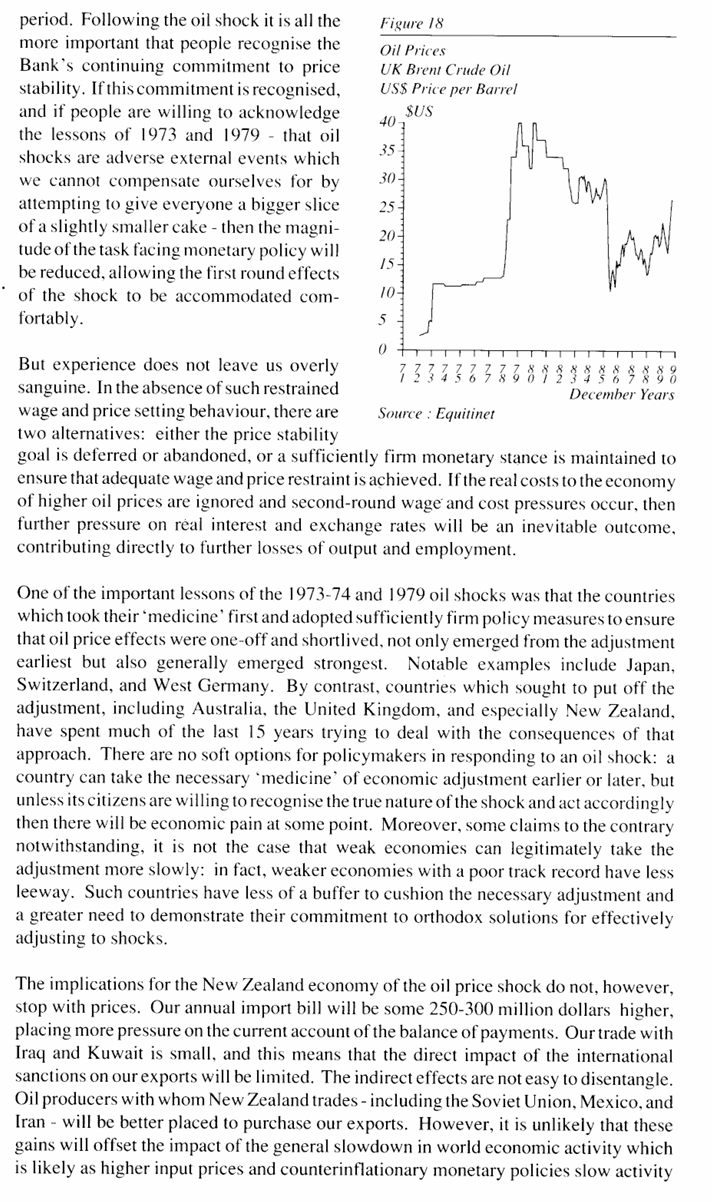

Rereading that 36 year old text, one thing I was struck by was that our experience then had been with oil price shocks that proved semi-permanent (see Figure 18 above for both the 1973 and 1979 shocks). Faced with permanent oil shocks it really was critical to get across messages like the one above, that if the national cake was now smaller we couldn’t try to fix that by all trying to cut ourselves a larger slice. As it happened, permanent shocks haven’t been a feature since then; whether in 1990/91, in 2008 (more a demand-driven surge, but still extreme for countries like us), or in 2022. The current view is that the Iran-related disruption, severe as it is (and likely to worsen, as it affects end users at least) will also be temporary, and that presumption is a reasonable one on which central banks are likely to operate for the time being.

(Acute readers may have noticed the final sentence of that September 1990 document – the bit about threatening “our ability to move back up the world’s economic league tables”. We were then optimistic. Unfortunately, in the decades since, we’ve nothing better than slowing our rate of relative decline. It is difficult to think of any country we were poorer than in 1990 that we are richer than now. But whatever the – contested – reasons for the failure, it wasn’t anything much to do with the Reserve Bank or its handling of monetary policy over the decades, whether faced with demand shocks or more supply shocks like today’s oil one.)

Hi Michael, thanks for the history, useful. Seems difficult to judge how long or when second round inflation risks are developing (e.g., give it three months, six months?) but wondering if you had any thoughts on this in the context of a ‘medium term’ return of (core) inflation to within the target band. Labour market conditions /future wage growth seem a key part of the judgment around persistence: guess unemployment conditions today differ from 2022 but it also seems the RBNZ is keen to raise rates or at least affirm the rise in wholesale interest rates (as shown on their website). Thanks again.

LikeLike