It was six months ago this afternoon that the resignation of the Governor of the Reserve Bank was announced, and with it the tangled and ongoing web of deception and obstruction.

I wasn’t planning to write anything today, but information continues to seep out – occasionally proactively, sometimes involuntarily, and sometimes (apparently) through journalists’ sources. In just the last day or two, we’ve learned a whole lot more about the largely unknown – eg the Minister of Finance says she wasn’t aware of it at all – special Board-members-only Reserve Bank Board meeting on 14 Feb, when the Board finally has to stare in the face the reality that their fanciful bid for resources for the next five years was utterly unacceptable to Treasury and the Minister. It also turns out that Treasury’s first advice on the bid that had been lodged back in September, and which is still described as only a “preliminary assessment”, had only gone to the Minister the previous day (that paper was finally released by the Minister yesterday afternoon, Treasury having previously withheld it). None of this had made any of the Reserve Bank’s previous statements (11 June or 29 August).

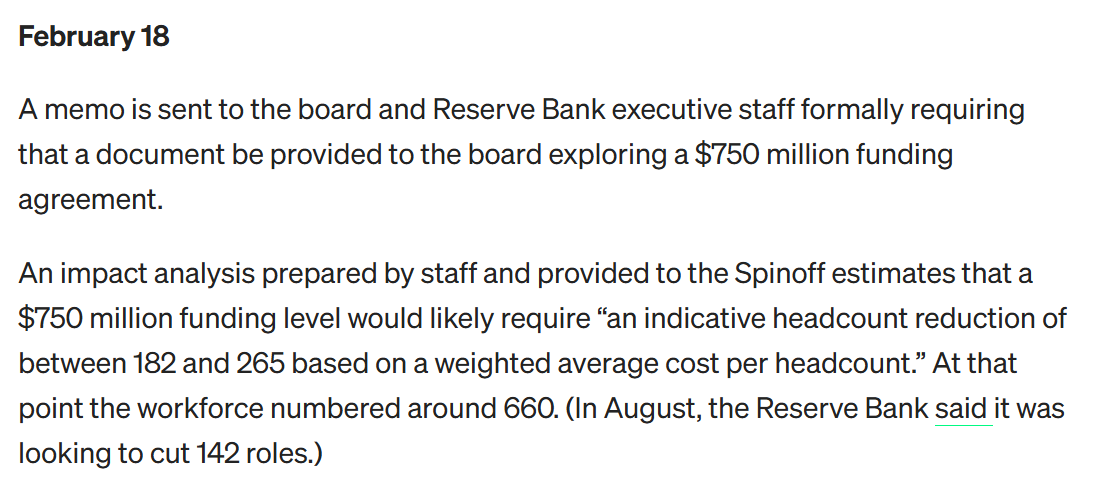

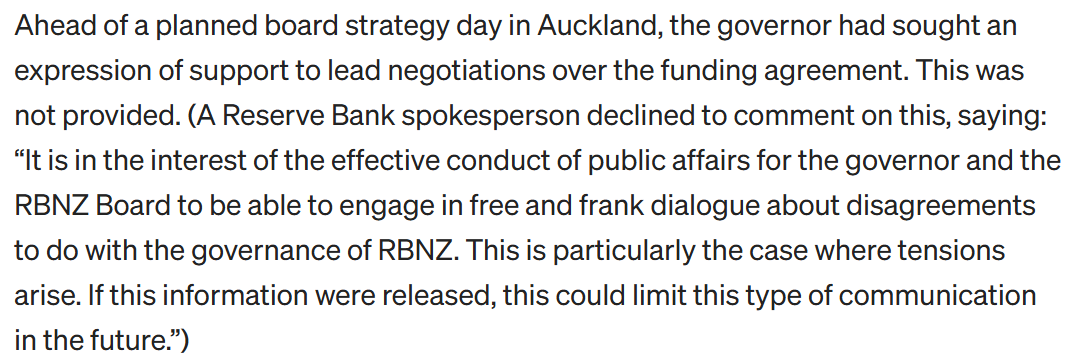

This morning The Spinoff has a piece with material new details, apparently from an inside source. They don’t change the overall characterisation of the story but they flesh out the picture a bit more. The new snippets I spotted included

Days after that crucial special board meeting (I’ve now requested both papers from the RB)

and on 26 Feb (and note that ongoing obstructiveness, about events that are now months old and will hopefully never recur)

Quigley may have gone but the obstructive approach from Hawkesby and the remainder of the board seems to continue.

I have updated my own more detailed timeline to take account of Spinoff’s information. As and when anything more emerges I will attempt to update it but there is a standing link here.

It is worth being reminded of others things the Bank still refuses absolutely to disclose. I had a request in a couple of months ago for just the elements of the exit agreement governing a) the process for agreeing a statement [ie for the 5 March announcement] and b) the non-disclosure terms. The Bank has refused to release that information – so the public has no idea what secrecy they committed themselves (or Orr) to, as regards the departure of one of the most powerful and controversial officials in New Zealand. The Ombudsman lived down to form and confirmed to me yesterday that their office is backing the Reserve Bank on this one, despite what would seem to be a clear public interest now (and long since) in transparency (whether through release of specific documents or summaries of them – the latter done in last week’s partial timeline).

There are two other things where nothing material has been revealed yet. The first relates to the 5 March announcement itself, and the second to the subsequent RB obstructionism.

Nothing in the selective pack of documents released on 11 June, or in any OIAs since, has revealed anything about the bringing together of the Reserve Bank statement announcing the resignation on 5 March. The Bank seems to have known for several days, probably since the previous Friday (28th) that Orr was likely to be going, and agreement on exit agreement terms appears to have been reached by Monday 3 March (although not signed until 5 March). You don’t bring together a document like that press release on such a sensitive issue in half an hour, or without multiple drafts or sets of edits. There must have been discussions about the approach that should be taken – “just how untruthful and misleading can and should we really be?” sort of thing. We know from disclosed documents that Orr and his lawyers had to clear out and they presumably had both wording requests, objections to other proposed phrasings, and probably received pushback on their own proposed lines. There is also nothing about how Quigley’s mid-afternoon two sentence addition statement (which explicitly introduced the “personal decision” bait, reinforcing the line that it was about “inflation job done, time to go, nothing to see here”) came about. Did anyone – other board members, acting Governor, senior comms managers, legal staff – raise any objections? Did they even see what Quigley was planning to say before it went out? Was there any prepping of the board chair for his press conference that afternoon? (it would seem inconceivable in general not to have – someone inexperienced in a press conference on a highly sensitive issue – but after six months of this few things would surprise any longer). Oh, and of course, what input – or visibility – did the Minister or her office have as the comms strategy and press release were formulated (loss of a major economic official etc)?

And, of course, we know nothing about how the Bank has prepared for, deliberated on, debated etc the handling of the numerous OIA requests (other than the generic “not well”). If you go back to the 11 June pack of documents, they actually seemed to start off okay, with the ad hoc committee recognising that there would be OIAs and they needed to make sure that records were properly kept etc. But it must have been downhill from there, with a mix of carelessness, obstruction, the Quigley attitude that the public had no real right to know, and of – at taxpayers’ expense – the hiring of a KC to buttress their determination to try to keep the public and taxpayers in the dark. How involved was the board as a whole in this strategy? If they were, it reinforces why they should go. If they weren’t, they were next to useless and should also go. And what of the acting Governor? Did he just go along, concerned to keep his job application alive, did he wholeheartedly endorse the Quigley strategy, or did he in fact dissent – and yet, in a strong position (they couldn’t afford to lose two Governors), do nothing? And what about the Communications Manager and senior comms staff? Perhaps they were more focused on keeping their own jobs. Precisely whose interests did the board consider was being served by their obstruction, especially once the Minister – to whom they are accountable – became belatedly aware that the misleading and the coverup was not tenable?

Questions – more questions – and perhaps the basis for further OIAs if anyone chooses to ask.

Meanwhile, six months on we still don’t have a permanent Governor. Reports suggest the process is fairly far advanced, but how much confidence can we have in someone this board – chaired by Quigley until Friday afternoon – will have come up with. There is a crying need for a first rate candidate, and not one tarred by the Orr years or the months of obstruction. We must hope the government insists on one, but given the Willis/Luxon record to date – slow and weak in dealing with RB matters, not showing that much sign of caring much – it is difficult to be optimistic. And if the government goes along with a mediocre nominee, we must hope the Opposition parties insist on excellence, and don’t just nod through someone on “any warm body” grounds. A first-rate board chair also seems vital – including to both support, counsel, and challenge the new Governor – and it seems unlikely that that person can be found among the compromised existing board.