I had an OIA response yesterday from the Reserve Bank. There is more obstructionism, so a letter will be going off to the Ombudsman this morning, but there was also some interesting information released.

A while ago the Bank’s Board started publishing proactively minutes (carefully crafted ones) of its meetings. It seemed like (and was) a welcome (if limited) initiative, including because it minimised the number of OIA requests they’d need to deal with. But they leave out a lot, and it also only slowly became clear (to me anyway) that they were only releasing minutes of what they described as the regularly scheduled meetings (more or less monthly). The minutes of the February and March Board meetings included these

Of those this year, only the 27 February meeting was a regularly scheduled one (you can read the minutes of that meeting on their website, although almost all the interesting stuff isn’t included (there is nothing about the Funding Agreement or about the Governor – to be clear, not redacted or withheld on OIA grounds, simply not included in the minutes, despite the Public Records Act). Similarly at the full meeting in late March there is no discussion or debrief on the resignation of Orr, or of communications around it, or on approaches to the various OIAs they had already received. Yeah right.

Anyway I asked for the minutes of the other meetings, and received them (in full) yesterday. There are no redactions. The 5/6 March, 10 March and 13 March ones were done by email circular confirming a) Orr’s exit agreement and b) aspects of the revised Funding Agreement proposal. The meeting of the 18th dealt with the appointment of a temporary Governor, where there appears to have been substantive discussion including on expectations of such a person, but a decision that the only person they would seek an expression of interest from would be Hawkesby.

MInutes of RB board special meetings Feb and Mar 2025

[UPDATE 5/9 The minutes are now also on the Bank’s website.]

The one that caught my eye though, and the reason for this post, was the minutes of the 14 February special Board meeting. It was a virtual meeting attended by all board members, but with no other senior management present, just a staff notetaker. Here is the substance of the minutes (not forgetting the opening prayers)

Which seems like a rather important, and deliberate, omission from the carefully chosen set of documents the Bank released on 11 June, when they were still trying to divert us from what actually happened.

What they had released included the following.

From an Orr email of 5 Feb (to senior management, cc’ed to Quigley and Finlay). (I hadn’t previously noticed the rather surprising final bracketed observation – a Governor whose MPC was charged with keeping inflation near 2 per cent worries that inflation could average 3-5 per cent per annum over five years)

And from a long email from Orr to the Board on the morning of the special Board meeting (but before it)

And then an email exchange between Orr and Quigley after the board meeting. This is from Quigley

To which Orr responds with a “Yep all good”.

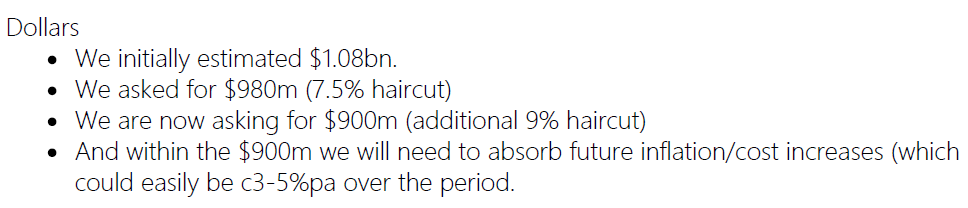

But what they didn’t release was the bit in the middle, which makes the timeline a bit clearer. The Bank had submitted its original Funding Agreement bid back in September, unanimously approved by the Board. This was the egregious one (seeking $981 million over five years), presented as offering savings of 7.5 per cent, but in fact involving materially higher future spending than the Funding Agreement covering the period to 30 June 2025 (variations approved by Grant Robertson had allowed). There is no sign in the minutes of December quarter Board meetings that they’d had any serious blowback (or feedback at all) and the only mention of the Funding Agreement is a discussion of the ‘nature and structure” of the next Funding Agreement when a couple of senior Treasury officials came for a regular visit.

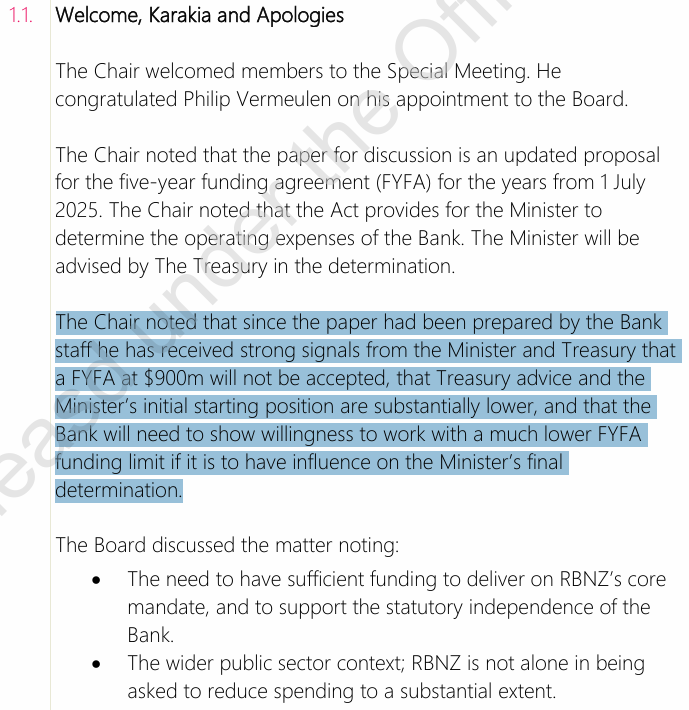

The (still) missing bit is what initially prompted the Bank to propose to revise down its bid. That plan was the paper in front of the Board at the 14 February meeting, in which it appears to have been proposed to lower the bid from $981 million to $900 million. Perhaps there was some initial Treasury pushback, but it cannot have been too strong or clear, because note the chairman’s introductory comments (emphasis added).

The Chair noted that since the paper had been prepared by the Bank staff he has received strong signals from the Minister and Treasury that a FYFA at $900m will not be accepted, that Treasury advice and the Minister’s initial starting position are substantially lower, and that the Bank will need to show willingness to work with a much lower FYFA funding limit if it is to have influence on the Minister’s final

determination.

“Strong signals” and from both the Minister herself and from Treasury, that what was probably intended as a compromise offer would come nowhere near meeting the mark. (Which is to the credit of the Minister and Treasury, but why weren’t those messages being sent back almost as soon as the initial dropped into the Secretary to the Treasury’s inbox five months earlier? And why has none of this previously been disclosed?)

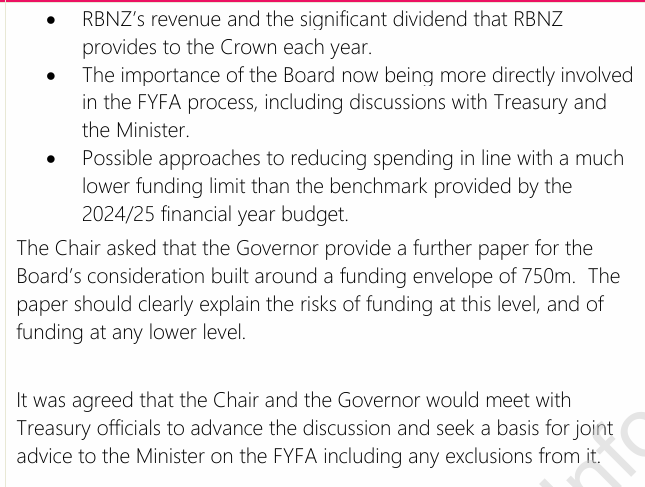

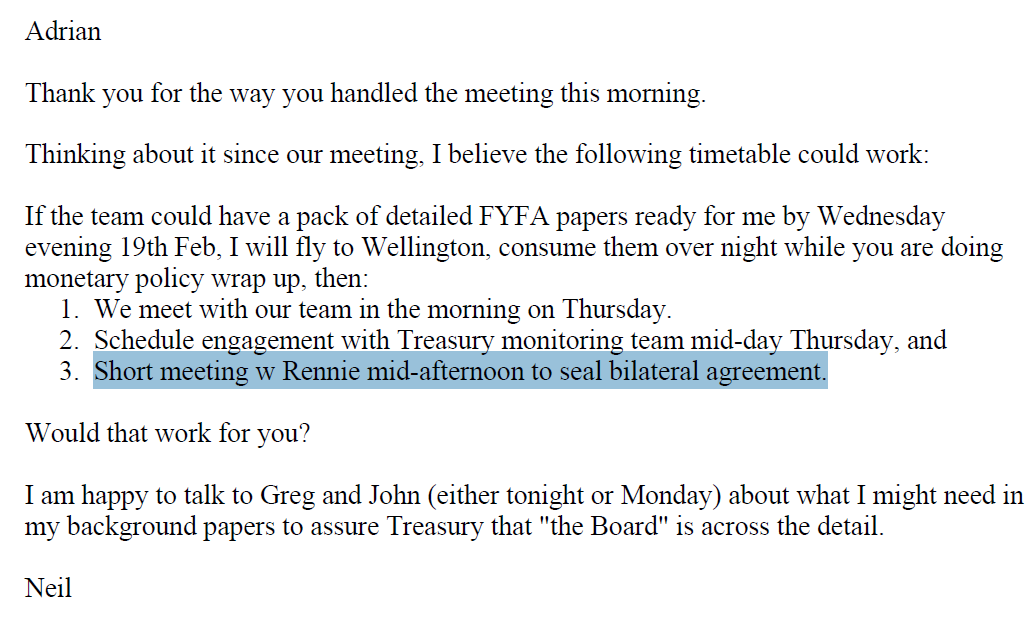

The Board’s response seems, belatedly, quite realistic (noting “RBNZ is not alone in being asked to reduce spending to a substantial extent”) but then you have to wonder how Quigley ever envisaged later that day that they would be able to “seal bilateral agreement” with Rennie at a meeting the following week. Did Orr not disclose to either Quigley or the rest of the board at the meeting on the 14th just how strongly opposed he was to having spending limits pulled back to around the levels in the expiring Funding Agreement? Did it only become clear when Orr lost his cool – and refused to apologise – at that meeting he and Quigley had with mid-level Treasury staffers on the 20th? In the end it wasn’t his call – the Funding Agreement is between the Board and the Minister, and the chief executive is responsible for working within it – but if he hadn’t put his cards on the table, in a calm and rational manner, at a special board meeting on the issue, it is hardly to his credit. And if the goal of the 20 February meeting had really been “joint advice” to the Minister, it is even more reason for Quigley to have regarded Orr’s behaviour as so unacceptable (and utterly counterproductive).

Does any of this greatly matter at this point? Probably not, but it does fill in a few more blanks (and prompt another OIA or two).

UPDATE 5/9 . There must have been quite serious and perhaps robust debate and exploration of issues/options, since the meeting ran for 105 minutes with no staff. Unsurprisingly the minutes don’t record the tenor of the debate but note that that same evening Quigley thanked Orr for the way he’d handled the meeting, so this one can’t have been explosive.

I had a little play on AI and came up with the following numbers. Whilst I have not verified their veracity, I do recognise that the overall trend of the numbers do not lie. Why in the age of computers (including AI) do we now have such large number of headcount (and the corresponding expense)? We should be down in the 200 FTE as per the Brash age.

Gemini AI:

The Reserve Bank of New Zealand (RBNZ) has undergone significant changes in its staffing and expenses, with a notable pattern emerging from the tenure of Don Brash to the present day. This period shows an initial trend of downsizing followed by a more recent and substantial expansion.

Historical Data 📉

Don Brash served as Governor from 1988 to 2002. During his tenure, the RBNZ underwent a major restructuring and efficiency drive that dramatically reduced its size. In the late 1980s, staff numbers were around 600-700. By 1999, this had been cut to around 285, and by 2002, the number was below 200. This period was marked by a focus on “productivity and efficiency gains” and the establishment of the RBNZ’s pioneering inflation-targeting framework.

After Brash’s departure, the RBNZ’s staffing levels remained relatively stable for over a decade. From 2000 to 2017, the headcount hovered in the 200-250 range.

Recent Expansion and Key Numbers 📈

Since 2017, under current Governor Adrian Orr, the RBNZ has seen a massive increase in its workforce and expenses. This growth is linked to a broader expansion of the bank’s mandate and functions, including new responsibilities for banking supervision and financial stability. The number of full-time equivalent (FTE) employees has grown significantly, more than doubling in recent years.

Year Headcount (FTEs) Operating Expenses (NZ$ millions)

late 1980s ~600-700 N/A

1999 ~285 N/A

2002 under 200 $24.9

2017 ~255 N/A

Jan 2025 660 ~$200 (2024/25 budget)

Export to Sheets

Key trends:

Headcount: The number of full-time equivalent employees has grown from 255 in 2017 to 660 as of January 2025. This increase is largely attributed to growth in non-legislative functions.

Expenses: The RBNZ’s operating expenses have also increased dramatically, with the 2024/25 budget at approximately $200 million. A new funding agreement for 2025-2030 has been negotiated, which will see the average annual operating expenses reduced to $150 million, a 25% decrease from the 2024/25 budget.

Salaries: The number of employees earning over $100,000 has more than tripled since 2017, from 132 to 436.

Leadership Structure: The leadership structure has also become more complex, with the number of Assistant Governors increasing from zero in 2000 to eight in 2024.

LikeLike

Interesting. I was in the senior management group at the end of the Brash era and I thought then we had unsustainably too few staff (my dept had about 6 functions, incl crisis-related ones, and about 25 staff, so were v thin). The Bank has been given various new functions by Parliament since then, so I’m prepared to believe that 350 FTEs might be about right today)

LikeLike

A belated but very warm thanks to you, Michael (and, as you have noted, Jenee Tibshraeny at the NZ Herald) for your persistent, principled & courageous pursuit of what’s been going on at the RBNZ over the past 5 years.

It is sobering to realise that without your work we (the public they are meant to serve aka the mugs who fund it all and bear the brunt of their multiple failures) would have known very little of it: the LSAP debacle, the misleading of Parliament, the funding & staffing blowouts, Orr’s meltdown, Quigley’s incompetence and the absence of honesty, transparency & accountability on just about everything.

None of the major players come out of this well, including Ministers Willis & Robertson, and all members of the RBNZ Board & MPC. Willis & the Board are fortunate to have an opportunity now to appoint a new Governor and a new Chairman, and show us they have at least learned something from a very sorry, much too-long saga that has not only severely damaged public trust in the RBNZ, but has also inflicted considerable financial pain on New Zealanders and cost us very significant money that could have been directed to, for example, hospitals, schools, housing and infrastructure.

More power to you!

LikeLike

Thanks

LikeLike