I think my post yesterday made a pretty conclusive case that the Minister of Finance had been fully part of the choice to deliberately mislead New Zealanders about what went on with the resignation of Adrian Orr. It might, initially, have been a fairly passive involvement re the proposed comms lines – when she, as responsible minister, should have been taking the lead in the run-up to 5 March, not leaving things to Quigley and the post-Orr Bank management (who, to put it mildly, do not have a strong track record on openness and accountability, or much sense of the likely public and political interest and risks). But she and her office quickly became fully part of it – prevailing on Quigley to do a press conference, knowing that it was exceptionally unlikely he was going to tell the truth, never challenging his statements before they went out, and signalling to the media afterwards that she was comfortable that a sufficient explanation had been offered. And then for months, even as it appears she gradually realised the coverup wasn’t going to prove tenable and offered occasional rebukes of Quigley, she continued to defer to the Bank/Quigley and used none of the knowledge or leverage that she had to force a more truthful set of disclosures. When finally Quigley was tossed overboard on Friday, it was only in the wake of fresh public furore about stuff she’d known of all along, and even then her press release just (so she says) recycled Quigley’s excuses for going – “the good job, well done, time to move on” stuff, Quigley had for a long time tried to deceive us with about Orr. Yes, she got more honest in her radio interview shortly after, which was better than nothing but not a great deal.

All in all, it should be quite unacceptable behaviour from a very senior minister. And even at this late stage there is no contrition, no sense that she might ever have done anything better or different. In face of the pretty clear set of facts it is both unconvincing, and leaves her looking weak (prisoner of Quigley gone rogue, sort of thing).

When I wrote that post yesterday I hadn’t heard the interview/exchange on Radio New Zealand earlier that morning (audio here, article here). Willis was no more convincing than in any of her other defences (eg as reported by the Herald, in an article linked to in yesterday’s post). She knew, she actively deferred to the Board chair for months, and at any time she could have insisted on more truthful explanations (even if the RB persisted in its own obstructive OIA responses). But I wanted to touch just briefly on a line she used in that interview yesterday, where she claimed that the independence of the central bank needed to be respected, and it would have been quite inappropriate for her to be involved in anything around Orr’s exit.

The Minister knows very well that the Reserve Bank legislation is carefully designed to distinguish matters over which the Bank has policy-setting responsibilities (eg many areas of prudential policy, such as bank capital requirements), where the Minister sets the goal but the Bank has operational autonomy (around monetary policy: the Minister sets the inflation target, the MPC adjusts the OCR to (aim to) deliver inflation near target), and where the Minister has primary responsibility. The old mantra was that Act was designed to balance operational autonomy with accountability, and to delineate carefully where it was that ministerial powers and responsibilities should be, and needed to be, exercised. One can debate the structure of the Act – I do, in a number of respects – but it is the law, and the Minister voted for the current legislation when it went through the House in 2021.

No one, but no one, seriously suggests that the issues that prompted Orr’s departure (announced on 5 March) had anything at all to do with the conduct of monetary policy (where it is important for the Minister and Prime Minister to keep their distance, not offering OCR advice in private meetings). As far as we know – and the Minister says she hasn’t seen the letter of complaint – the issues the Board sought responses on related to Orr’s personal conduct, and issues around trust in the context of a breakdown over Funding Agreement negotiations. There has never been a hint that monetary policy decisions were in the mix.

And the Act is quite clear that hiring and firing a Governor is finally a matter for the Minister (and Cabinet). The Board has roles in some of that – the Minister can only appoint as Governor a person the Board nominates (she is not bound though to accept any specific nominee), and the board can offer thoughts on whether the Governor’s performance or conduct rises to dismissal level, but even there the Minister (and only the Minister) can act to remove the Governor without a recommendation from the Board. Orr’s resignation was, as the law requires, submitted to the Minister, just cc’ed to the Board. So the repeated claim from the Minister that it was really important that she had nothing to do with any of it (was just a passive bystander, updated only when necessary) does not stand a moment’s scrutiny. Not only did the law give her a perfectly valid role, but so – frankly – did commonsense. In Opposition she’d objected to some of board appointees Robertson had made, who were mostly still there in February 2025. She knew that Quigley’s public handling of some past Bank issues had been questionable (to put it charitably). Wouldn’t any sensible senior minister, informed (say) on Friday 28 February that it was now all but certain that the Governor was going, after “employment discussions” initiated by the Board, have been all over the proposed communications lines? She might not have wanted her hands, or those of her office, to be too visible, but to sit idly by while the Bank (and Orr) dreamed up comms line – which would inevitably face robust external scrutiny – was to (voluntarily) make herself a hostage to fortune. That would be both risky and inept.

But the real point of this post wasn’t to repeat ground from yesterday. Instead, I want to put the Minister’s highly questionable part in the events of the last few months in the context of her overall handling of Reserve Bank issues since her days in Opposition.

Anyone who watched FEC hearings prior to the election could detect the frosty (at best) relationship between Orr and Willis. At times she did ask searching questions, and Orr did not like that, and tended to treat her – as so many of those who challenged or criticised him – dismissively. But there was never much follow through from Willis.

National opposed Orr’s reappointment, when (as the new law required) the other parties in Parliament were consulted. It was good that she did, but her central argument was half-baked (at best) and thus undercut the thrust of what could have made it hard for Robertson to proceed.

The point in the first sentence of that clip from her letter was quite right – and one hopes she bears that approach in mind with the appointment to be made shortly – but she’d already undercut the case with the half-baked “it’s election year argument”. People like me, who agreed with the bottom line (it really was dreadful that Orr was reappointing, leading us to this year’s mess), had to distance themselves from such an ineptly made case.

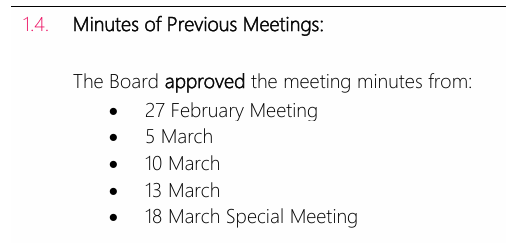

In Opposition she made much of the need for a strong independent inquiry into monetary policy during the Covid period (pushing back against the adequacy of the Bank’s own rather self-congratulatory and premature review of the MPC). One could debate how useful it might be, but it was a strong commitment, but nothing happened. (Curiously, in the March 2025 Board minutes there is this

and yet still nothing has been seen or heard.)

They made quite a bit about the staff bloat and loss of focus in Opposition, but then what?

Even in Opposition, there was no follow-up when Quigley was caught out actively misleading the Treasury, which in turn prompted them and Robertson to mislead the public in (about the infamous ban on experts serving on the first MPC).

It was pretty clear when National was in Opposition that they’d have preferred to be rid of Orr if they could. I pointed out back then (in a post prompted by a conversation with an interested party) that he couldn’t just be removed, but that there were quite a few things that could be done to put pressure on, to encourage early change, to improve how the MPC worked, and perhaps even to prompt Orr to think it really wasn’t an environment he wanted to stay on in). Almost none of it was done.

Quigley’s term as chair expired on 30 June last year. He’d covered for Orr for years, he’d led the board that recommended the reappointment, he’d been responsible for the blackball (and the lies), and he’d been chair since 2016. It was no-brainer to replace him, and would have been entirely uncontroversial, but she didn’t. She didn’t even keep the board fully manned (she was stuck with the Labour appointees until their terms ended, but you have to use the leverage and opportunities you have).

She did nothing to overhaul the charter for the Monetary Policy Committee, to encourage greater openness and accountability, or an expectation that members would be available for speeches/interviews. She seems to have done nothing more generally to encourage scrutiny and openness – it is now almost 11 months since the Governor or any second tier Bank person gave an on-the-record speech (extraordinary by modern central banking standards).

And if she did appoint two new MPC external members when the terms of the two 2019 originals finally ended, and the new ones appear to have been an improvement…..but we can’t really tell because we hear nothing of or from them. And then, again for reasons that escape understanding, she extended for one last six month period the last and elderly external MPC member from 2019 who’d been there through all the policy mistakes and communications lurches of recent years (that position now needs to be filled in the next few weeks).

We might also give her some credit for this year appointing a bit more economic expertise to the Board, although both appointees seem stronger on macroeconomics, which the Board isn’t directly responsible for, than on the regulatory side of things which the Board has direct responsibility for.

And what about the organisational/management side of things? Given the Minister’s evident unease about Orr, and her (quite appropriate) Opposition concerns about use of resources, you’d have thought that on coming into office she’d all over this (herself, and on her behalf her office and The Treasury) making life much less comfortable for the Bank from day one, even if (as was the case) they had a generous Funding Agreement running through to 30 June 2025.

Instead what we got was little and feeble for far too long.

Take last year’s Letter of Expectation to the Board (dated 3 April) These documents can’t compel agencies to do anything in particular, but wise boards are sensitive to the emerging expectations and priorities of ministers. There is six pages of the letter but nowhere does the Minister hone in on the very rapid increase in spending and staff numbers and signal a need for cutbacks. There is just woolly generic stuff

This was written in the run-up to last year’s government budget. Most departments were facing cuts immediately, and one other independent agency – ACC – while not directly controlled by ministers decided that, reading the times, they’d make savings anyway. It wasn’t even suggested to the Bank. And although there was a reference to the future

which should have been enough for a Board attuned to the times, it was pretty thin gruel and there is no sign the Minister ever sought to use the moral authority of her office, her bully pulpit.

The Bank doesn’t include the specific Letter of Expectation they got a bit later on the next Funding Agreement with the other documents on that deal, but it is here. I pointed out last week that, reasonable as it seemed, it contained a rookie error

talking in terms of savings relative to the Bank’s 24/25 budget, rather than savings relative to the Funding Agreement limits for 24/25. And even then, you might have hoped that in an agreement reached only every five years, in an institution that the Minister knew had lost focus and discipline, you might want a zero-based case for spending rather than just trimming the last level your predecessor happened to approve.

But, of course, it was all worse than that. The Bank actually set a budget that was about 23 per cent in excess of the Funding Agreement limits for 24/25 – fully and unanimously endorsed by the board – and when they had to consult the Minister on the Statement of Performance Expectations for 24/25 they simply left out the numbers. They didn’t tell the Minister what they were planning to spend. And neither she nor Treasury insisted on finding out. It isn’t clear when they finally realised, but it looks like not until very late last year at the earliest. And even when they did there is no sign of any consequences for anyone. There is no robust letter from the Minister rebuking the Bank for such egregious excess (and even if the Bank has a KC who claims – as lawyers do for their clients – that it wasn’t strictly illegal, it was entirely out of step with the thrust of government policy, and the times), the board chair wasn’t sacked, and no board members were removed (another of them was actually reappointed this year).

And then of course there was the egregious Funding Agreement bid approved by the board (unanimously) in late August and lodged with Treasury in September 2024. In a sane and serious world, Treasury would have opened the document, realised the gamesmanship that was afoot (at taxpayers’ expense) – this was trying to set a base for the next five years using the bloated 24/25 budget as base, not the previous Funding Agreement limits – and a) sent it back immediately, with clear expectations of something much lower, and b) immediately informed the Minister of what was going on, and advised her to call in, or write to (or both), the chair and the Governor to make clear that not only was the budget itself a fundamental breach of trust, but that the new bid was egregious and utterly unacceptable.

[UPDATE: This afternoon (4/9) MOF proactively released various documents relating to the Funding Agreement. Among them is Treasury’s preliminary assessment to the Minister of the Bank’s Funding Agreement bid, which is dated as late as 13 February.]

But there is no sign that the Minister did any of that, or that her expectations of Treasury monitoring of the Bank were sufficiently clear that Treasury did anything either. It seems not to have been until very early this year that the Bank finally began to get a sense that the bid was not going to fly.

In the end, she sort of got there. The final Funding Agreement limit was a lot lower than the Bank had wanted – and involved big dislocation for the Bank and staff because of the unauthorised spree the Bank had continued on with last year, when the Minister could have acted to bring it to a halt much earlier. Even then of course, the cuts relative to the Robertson levels were modest, and the current restructuring seems to be taking staff numbers back to about 2023 levels, probably still 50 per cent above what is necessary. And the Governor and board chair are now both gone. But what a messy and inadequate way to have got there.

It isn’t as if everything she has done as regards the Bank has been bad or wrong, but most of it has been late and/or weak, when she knew from Opposition days that it was a problem institution with a highly problematic chief executive. Who knows why. I wonder if some of it was that she just didn’t care much (it was a below the radar issue with no votes in it) and perhaps she was rather out of her depth (eg the limp arguments recently about independence, showing she has no deep feel for the legislative model, or an ability to articulate it). She seems to have been poorly advised, and ill-served by his own advisers and by The Treasury (which has since cleaned out and replaced almost all its senior managers).

But all in all it is a deeply underwhelming performance from such a senior minister. And if that stuff is just regrettable, avoidable and expensive, the coverup and deliberate sustained intention to mislead New Zealanders around Orr’s departure is inexcusable: weak, inept, and dishonest.

UPDATE: While I was typing this post I had an email from a senior political journalist who passed on this snippet (with permission to use it)

“On October 30 I interviewed Willis about her role as State Service Minister. So it was not an economic interview, per se. At the end of the formal part of the interview we chatted about a few things but we did not discuss the Reserve Bank until she brought it up and said she was determined to cut back its funding.”

Which is interesting, and perhaps consistent with my story. Her instincts were sound – the funding needed to be cut back – but it isn’t clear that she did anything at the time, and it isn’t even clear that she’d yet had any advice on the bid or was aware of the egregious 24/25 budget the Bank’s board had set for itself. The “strong signals” – see this morning’s post – don’t seem to have come until February, months later.