Since I published the post on Tuesday, reporting what an anonymous (currently or recently former) insider had told me about events around the Adrian Orr resignation, what new we’ve heard or learned seems (to say the least) not inconsistent with the substance of that person’s story.

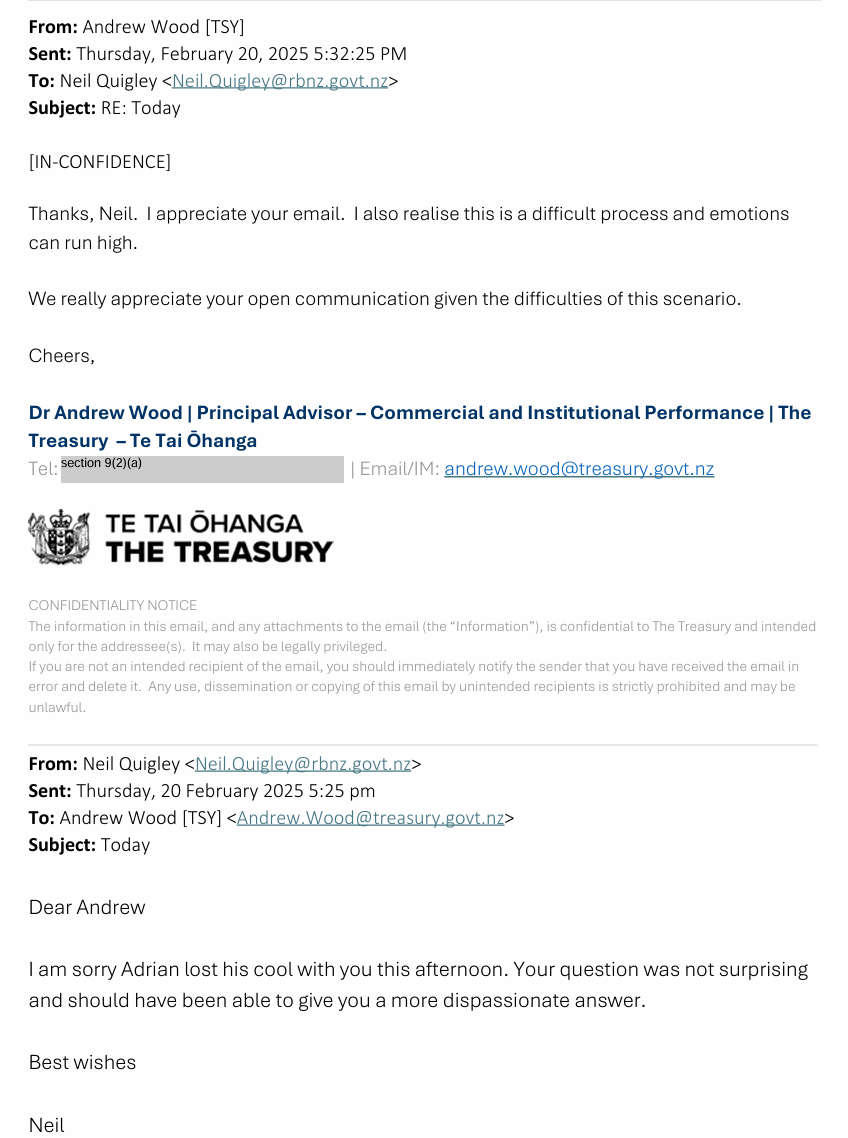

As it happened, the one concrete revelation may almost have come about by accident. In my post on Tuesday I’d written that Board chair Neil Quigley had contacted Treasury quite agitated about a Treasury record of a meeting between senior Bank and Treasury people on 21 February. It was only yesterday I reread my source and realised I’d made a mistake, and that bit of the story related to the meeting between the Bank, Treasury, and Minister of Finance on 24 February. But by then the Herald had asked Treasury about the earlier meeting (which was actually on the 20th). Treasury could, fairly easily, have stonewalled, but in fact they confirmed that Neil Quigley had emailed one of their staff after the meeting in respect of the Governor’s behaviour at that meeting. Today they have released that email exchange.

We don’t know how bad it got but…..things have to have been pretty bad for the Board chair to have taken that initiative (and notice the Treasury official’s “emotions can run high” – about funding debates, among normal disciplined people???), presumably having failed to persuade his chief executive, the Governor, that he himself needed to apologise. So, if we don’t yet know a lot with certainty about the 24 February meeting, and the record thereof, we now definitely know that Orr’s conduct was a significant issue just days before the exit agreement negotiations started, following the Board meeting on the 27th.

We don’t know with certainty that Quigley emailed Orr on the 27th attaching a statement of behavioural/conduct issues going back several years, and asking for a response, but…..the Reserve Bank refuses to deny the existence of such a document (there are multiple OIAs from people trying to smoke it out). Even allowing for their dogmatic “we’ve said all we are saying or legally can say” line, if the story was simply untrue, and had no basis in fact, surely it would be in both Orr’s and Quigley’s interests to have it denied in no uncertain terms (free opportunity to tar me as well I guess). The obstructiveness is, almost certainly, pure choice. And despite their claims otherwise, there has been no evidence of good faith dealing with legitimate public interest at almost any time since 5 March, when Quigley began his unsuccessful attempt to mislead us into believing that it was just “a personal decision’ [as in one sense it was: Orr is a person, he did decide] of someone who was tired or thought a big job had now been done and it was just time for a change.

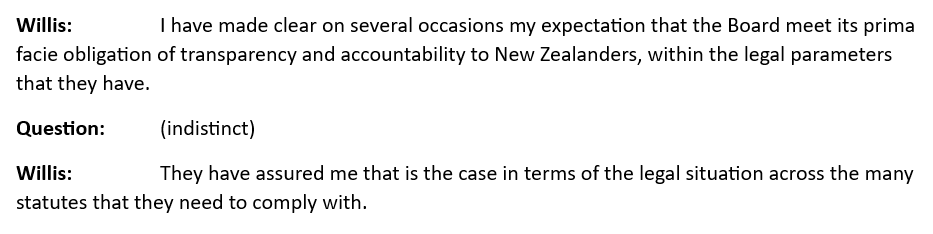

The Reserve Bank and its Board appear to be attempting to hide behind claims that there are legal restrictions on what they can say, including in response to OIAs (and remember that any request for information can in technical terms be considered an Official Information Act request whether it is answered on the spot or months later). This was a line they have also fed to the Minister who said the other day:

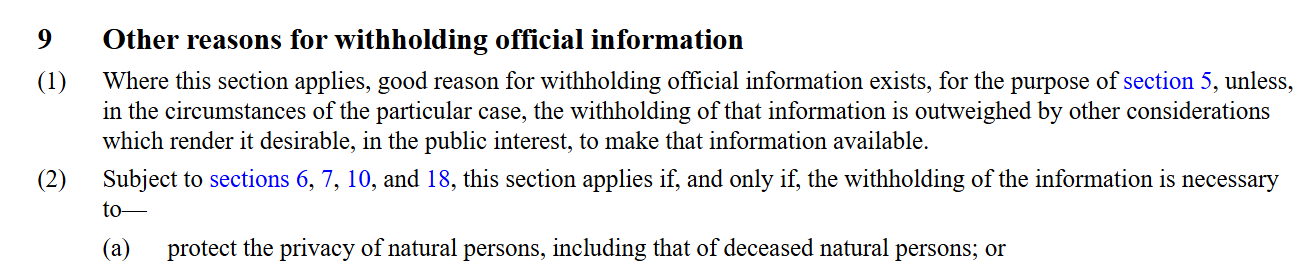

First, consider the Official Information Act itself.

There are conclusive reasons for withholding information. But they relate to national security, diplomacy, and one the Bank has occasionally used on me (very dubiously even then), things that if released could

What was going on around the unexpected sudden departure of the Governor just does not count.

So then we are down to section 9 which has a whole long list of other reasons why information can be withheld, all prefaced with the public interest override. It seems probable that 9(2)(a) is what they will be relying on

although whether it is Orr or Quigley, or perhaps both, they are trying to protect is perhaps open to question. For Quigley, of course, there would no case at all – embarrassment of someone who appears to have actively, deliberately, and repeatedly sought to mislead the public from his highly paid perch as chair of a government board is exceptionally unlikely to count as decent grounds.

Employees are a different matter. If some junior employee was quietly exited you’d expect 9(2)(a) to apply, in all but the most extreme circumstances (if I recall correctly I was once – possibly still – a party to such an arrangement – as manager that is, not employee). But on this occasion we are talking about the utterly unexpected no notice departure of one of the most senior, powerful, and controversial public officials. And it is also clear that the Bank – and its board chair – have already sought to obstruct understanding, transparency and accountability on repeated occasions. Not just by trying to convince us it was just “a personal decision” (tired, job done etc) but by obstructing (for months) and still OIA requests that included requests for material that cannot be any stretch of the imagination come wholly under 9(2)(a) at all (eg there are four board meetings in March – one the day the resignation was announced – where they have not even acknowledged the request for the minutes, let alone provided those minutes, even heavily redacted). They are trying to stonewall and obstruct understanding, and they should not be allowed to do so. 9(1) would give them ample grounds to release almost anything that has been requested, if they were at all interested in the public interest (in scrutiny, accountability, transparency….and little things they say they value like trust in an independent central bank). I say “almost everything”. If there really is the “Statement of Concerns” document, with its list of (alleged) behavioural/conduct issues, I don’t feel a need to see it; the fact of its existence and being sent to the Governor with a request for a response would then provide ample certainty, that what actually happened was a negotiated exit in the context of severe relationship breakdown and loss of mutual confidence, brought to a head by actual and recent serious conduct incidents.

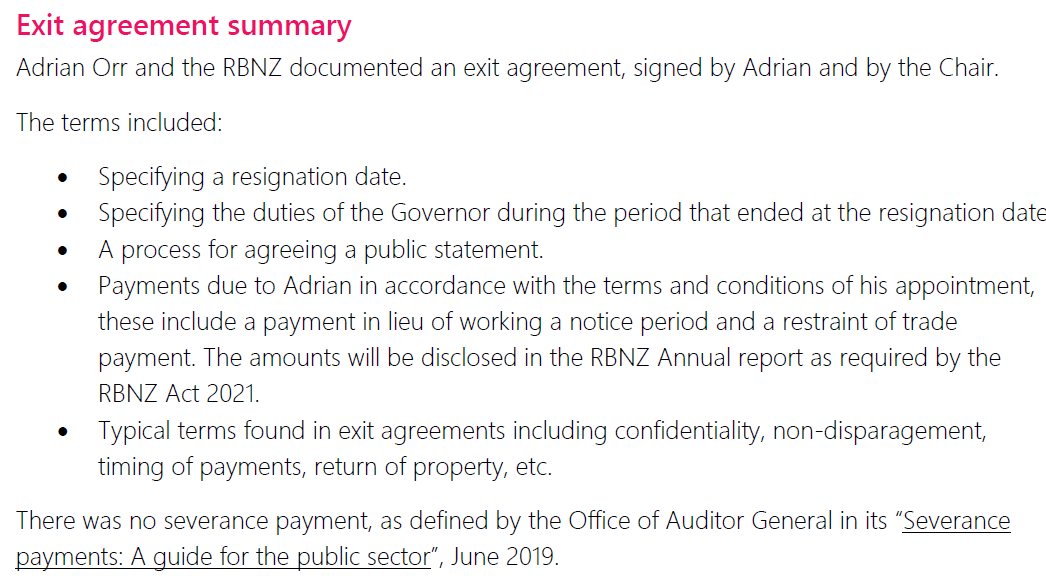

The remaining uncertainty is around the exit agreement negotiated with Orr. As I noted weeks ago, if someone resigns because they are tired etc, you don’t need expensive lawyers to negotiate exit agreements. Tired and job done are perfectly legitimate comprehensible reasons, with nothing to hide. You might agree to waive notice, but it doesn’t take a lawyer for that.

But in this case the expensive lawyers (“senior counsel”) were brought in by both sides.

This is what the Bank told us about the agreement on 11 June

I’ve now lodged a request for a copy of the items: “a process for agreeing a public statement”, and terms around “confidentiality, non-disparagement”. These seems likely to be very process oriented (very unlikely to describe whatever bad stuff Orr is claimed to have done) so there shouldn’t be any grounds to withhold, and there is a clear public interest in such a release, given that no one has given clear answers about the parameters of what the Bank promised not to say or why (or, I guess, what Orr promised not to say). I’m not optimistic, but we’ll see.

As far as I can see (but I’m not an OIA lawyer) you can’t just contract out of the OIA by signing an NDA (with quite as broad a reach as suits two people trying to avoid transparency, scrutiny or accountability). Ombudsman guidance notes suggest as much, but who knows. It looks as though whatever the NDA provisions in the exit agreement are, they could still be overridden by the “public interest” test in section 9 (the more so perhaps now, with so much effort to mislead already, than on 5 March). Perhaps the Bank has committed not to do so unless the Ombudsman explicitly rules otherwise – which could be years away, although I’m sure that I like all who’ve appealed related issues to the Ombudsman hope he is going to give this issue some urgency. We don’t know, and it isn’t good enough to simply wave your hands and say “we’ve done all we legally can”, often without even telling us the nature of what they’ve got and have withheld, or to explain what the parameters are of what they contracted to.

If this really is what it increasingly looks like, a negotiated but pressured exit, precipitated by real behavioural/conduct issues, perhaps some limited sort of non-disclosure provisions might have been a price worth paying. But even if so the public interest – transparency, accountability and all that – had to be paramount, and any restrictions had to be very tightly limited. And non-disclosure agreements don’t give license to simply make stuff up, and actively mislead the public. If Quigley is – as he probably is – so tone-deaf and indifferent to wider public interest considerations not to see that (and to recognise that interested parties were not likely to give up easily on seeking answers), the Minister (and Treasury) should have insisted on it. And despite the Minister’s attempt to disclaim all responsibility, recall that Orr’s resignation was to her, she is the only one who could have fired him, the board chair serves at her pleasure, the board operates accountable to her, the board operates within broad parameters in her letter of expectation. If she knew nothing about it, that is on her. She, it seems, had days to ensure that the public interest was being protected, and that real accountability would be protected.

As for the Minister of Finance, what is new from her is that she says that the first she knew of that Quigley email to Treasury was yesterday. Quite possibly so in the specifics, but Treasury is formally charged by her (and funded) to act as monitor on the Reserve Bank. If they had not been keeping her abreast of conduct concerns which weren’t exactly new – and many of them in the public domain anyway – they simply weren’t doing their job.

There isn’t much else to say about the Minister beyond the scepticism I noted in yesterday’s post. Does anyone believe she didn’t know what was going on? But in reflecting on the mystery of her dogmatic insistence that it is all nothing to do her, two old lines did come to mind:

- methinks she doth protest too much, and

- who will rid me of this turbulent priest [or Governor]?

If somehow she did use an opportunity that Orr created by his behaviour in mid-late February to prompt Quigley and the Board to somehow engineer an exit (that list of behavioural/conduct issues Quigley seems to have had must have been tended and grown over several years) then….well done Minister. If not, well….the mysteries are still there.

As to Quigley, whether or not the Taxpayers’ Union is generally to your taste, it is hard to disagree with this concluding paragraph of their call this afternoon for Quigley to go.

UPDATE: The one other thing I meant to include here was a suggestion that some journalist might ask the Bank (or other plausible entities where people might have become aware of the relevant bits of information – eg Treasury, or MoF’s office) if they’ve launched a leak inquiry. If it is all make-believe stuff and nothing of substance was true in what my source said then…..there wasn’t a leak. If some or much or all of it was substantively true then, given the Bank’s determination to say nothing more, there was a leak from somewhere. I have no idea where the source works or worked, but there is probably a quite limited range of options, and the Bank must be one of them.