On 11 June the Reserve Bank finally (more than three months after his departure) did a pro-active release of carefully selected documents relating to the departure of Adrian Orr. Those documents purported to respond to various OIA requests, although many elements of events around the departure, and many elements of the OIA requests, were simply ignored. It appeared to be a belated attempt to shape the narrative, never mind the law.

I’ve done a number of posts on these issues since 11 June, drawing partly on what the Bank released in that package, and on various interviews, and some other OIA releases, all to try to make more sense of what really went on in the months, days, and weeks leading up to the resignation and sudden departure of the central bank Governor.

and last week this

That last post, from last Thursday, prompted someone who seems to have been very close to events back in February/March to contact me out of the blue with a number of quite detailed comments about some of what really seems to have happened. I do not know who the person is.

I also cannot directly verify what follows. I have however this morning lodged a series of Official Information Act requests with the Minister of Finance, the Reserve Bank, and The Treasury in an attempt to check key elements of the account. My overall sense is that the account is likely to be trustworthy. It is written in a calm style, in places details fit with other stuff that is already in the public domain, and the author is not black and white (at one point Quigley is defended, on another where part of the account appears to be secondhand, the lack of certainty is explicitly acknowledged). My interactions since suggest someone who, while a little fearful for their own position, is frustrated at the lack of transparency (including abuse of the OIA) and believes more of the story needs to be told. Could I be being played? I suppose so, but on balance I don’t think that is what is happening.

When I was contacted, the person commented positively on what I have written about these events and suggested that they wanted to fill in some gaps. I will step through the various elements of the account I have been given, and will explain how what I was told fits with other stuff we know, or seems to fill gaps. As I noted to the person, their account “isn’t overly surprising unfortunately”.

The person who sent me this account out of the blue asked just that I keep their details confidential (I have barely any). I was still a little unsure what they envisaged or hoped for, so I went back and explicitly asked what, if any, of what they had sent me they would be happy with me using here. I noted that an alternative would simply be that I used what had been provided to shape some more OIAs without referring directly to anything in this correspondence. I also suggested that I might not be the ideal vehicle if they did want the material publicised and explicitly noted that, for example, the Herald had given these issues serious coverage and might be a better vehicle (including – a point I didn’t make explicitly – because they could ring up people in power and ask follow-up questions directly).

I was uneasy about the idea of using direct quotes since, in principle, writing style could be used if someone (a past or present employer) wanted to try to track down the individual. Independent of that unease, my correspondent got back in touch and explicitly indicated that they were okay with me using their information here, subject to using paraphrases rather than direct quotes. They reiterated both an unease about their personal risk and a view that the story should be told. They have made several mentions of the public interest considerations that are supposed to be of importance in dealing with OIAs.

And so here goes:

In last week’s post, I referred to a mention in a recent OIA response from the Reserve Bank that an hour or so after Orr’s resignation had been announced the Minister of Finance’s office had asked Neil Quigley to do a press conference. According to the Bank’s account, “the Minister thought it was important for the chair to front the media and possibly to calm the markets”. I’d noted in another post that no one had made Quigley do this press conference (which proved to be a bit of train wreck).

My correspondent starts by noting that in their view on this point I had been a bit unfair to Quigley. It is claimed that Quigley did not want to talk to the media (something I can quite believe, based both on his past behaviour and his responses to questions on and after 11 June) and had made that clear to management. My correspondent states that it actually took multiple communications, texts and calls with/from both the Minister herself and people in her office, before Quigley finally agreed to do so. There was no hint of any of this in the 11 June Reserve Bank release and my correspondent indicates that it was material that was within-scope for at least some OIA requests on events around the Orr resignation (including, I believe, mine). I still maintain that it was Quigley’s choice to do the press conference, but clearly he was put under considerable pressure.

In and of itself, it is not a revelation of great moment. However, the Minister of Finance has consistently attempted to distance herself from events around the Orr resignation, having claimed variously that she had no knowledge of why Orr resigned (“I have always been able to speculate”) and had no contact with the Board or Board chair on such matters (even though the Governor’s resignation had to be made to her not to the Board and – more a matter of substance than law – this was the very powerful chief executive of one of her main agencies). Perhaps it also points to the chaos of the day: recall that an earlier Herald OIA had revealed that Orr’s resignation had been brought forward on the morning of Wednesday 5 March to that day rather than, as planned until then, the following Monday. One might have supposed that the Bank, the Board chair, and the Minister and her office would have sorted out who would say what when before the resignation statement went out.

The second leg of the story goes to the heart of the resignation itself.

Recall that the Bank has tried to spin us a story that it was all about disputes over the Funding Agreement. This extract is from the (final version of the) statement the Bank published on 11 June.

An earlier (but near-final) draft – which they sent in error that morning to OIA requesters – had tied it more to a meeting between Orr, Quigley, Treasury officials and Willis on 24 February.

I noted then that it clearly wasn’t correct to characterise this as just a dispute over funding (as much media coverage did), since many public service CEOs have had disappointed expectations in the last 18 months and none of them had resigned with no notice. In one of my post 11 June posts I even observed (but briefly and without follow up) that it really wasn’t clear to what extent Orr had chosen to go and to what extent he’d been pushed.

My correspondent suggests there was a very considerable element of push to it, and that funding disputes were really no more than the immediate presenting context.

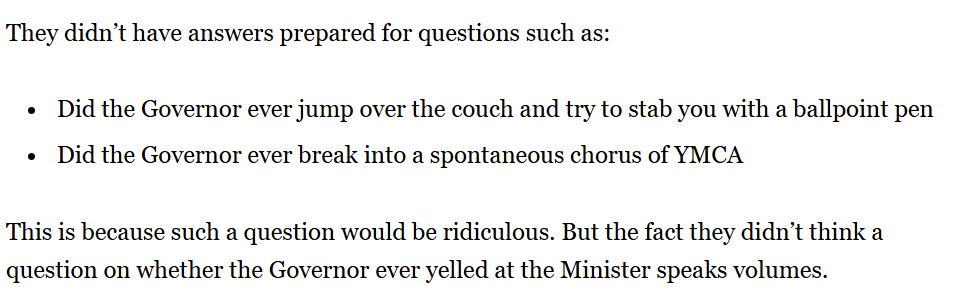

You may recall that an earlier Herald OIA (reported here) reported some Q&As that the Minister’s staff had prepared for her around the resignation included the telling one “Did the governor ever raise his voice with you?”, which it was suggested she should avoid answering, clearly suggesting that exactly such a “voice raising” had in fact occurred. As David Farrar put it at the time

My correspondent says “raising his voice” was the least of it, reporting that at a meeting with Treasury on 21 February the Governor had completely lost his cool, behaving in a way that was “completely inappropriate and swearing” and that it had been much the same in the 24 February meeting with the Minister.

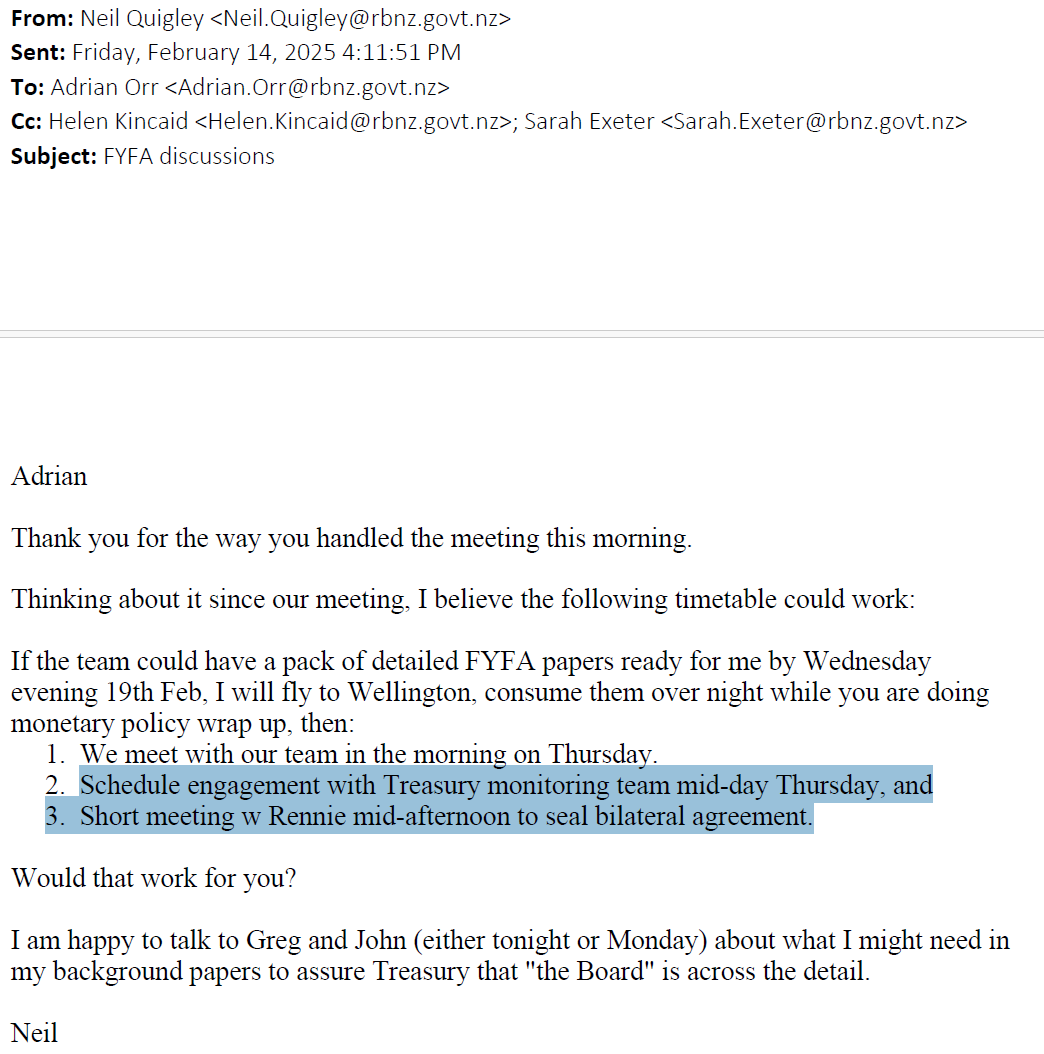

The timing of these events is pretty clear. The fact of the 24 February meeting has long been known. Of the meeting on the 21st we hadn’t previously heard directly, but it is likely to be the one proposed in this email from Quigley that was in the 11 June release pack

but ended up happening on the 21st rather than the afternoon of the 20th as Neil had proposed. The Bank clearly envisaged by this point that it was going to be smooth sailing on the Funding Agreement from here and that everything could be tied up within a few days. Clearly, that wasn’t what happened…..and as context for Orr completely losing it (if in fact he did) it sounds quite plausible and aligned to the facts.

Now, in this debauched age swearing isn’t uncommon and newspapers have taken to reporting crass and vulgar language directly. If you are less bothered by such behaviour than I am, it was still pretty extraordinary for an official – no matter how senior – to completely lose it in crucial meetings, most particularly with/to the Minister herself. You could see why future working relationships might be impaired – not by differences over approved spending (just the meat and drink of bureaucratic life) but over Orr’s quite extraordinary conduct. Or rather, just the latest episode.

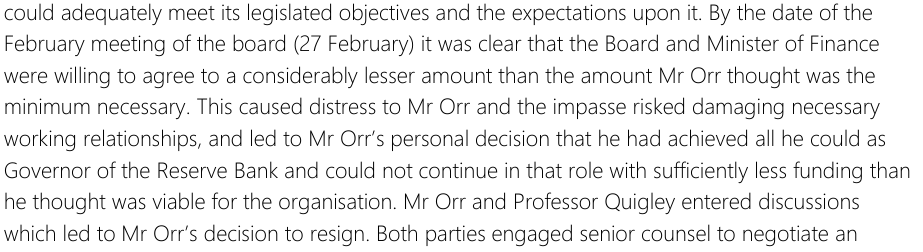

Because my correspondent goes on. The claim made to me, quite specifically, is that on 27 February Neil Quigley, as Board chair, sent an email to Orr which had an attached “Statement of Concerns” outlining quite a range of concrete and specific issues with the Governor’s behaviour covering several years (and not about funding). Quigley is reported to have asked Orr to respond. It was this, my correspondent says, that triggered Orr’s resignation.

The story fits with other things we know. The Bank’s Board met, for seven hours on 27 February. As I noted last week there is nothing in the minutes about the Funding Agreement, nor of course about Orr. It seems that such issues were all discussed in a (probably protracted) “Board-only time”, perhaps in part (also not disclosed in the minutes) without the Governor. We know that 27 February is also when Quigley advised Rennie who advised Willis that something was in the works re Orr’s future. And (although I can’t track it down this minute) if I recall correctly the exit agreement negotiations occurred over the couple of days after 27 February, and were concluded on Monday 3 March.

The story, if true, also goes some way to the mystery of the exit agreement which – we’ve been told – included gag provisions of some sort. When it appeared that the exit had been driven solely from Orr’s side it was very puzzling why the Board agreed to any such restrictions (setting aside the fact that resignation was a matter for which the Minister was responsible for dealing with).

But for the Board – and we must presume that Quigley wouldn’t have been acting without their support – to have presented Orr with a memo documenting behavioural concerns over several years, and explicitly seeking a response, they must have got to the point where, even if they wouldn’t put it in quite so many words, they had lost confidence in the Governor. When things get to that point, exit is a pretty common option (at lower levels, when public servants are told they are going to be put on performance improvement plans it isn’t unheard of them for them to up and resign, saving everyone the pain, and the employee the CV issues, of a dismissal process). But Orr still held a few cards: he was only two years into a second five year term, the Board couldn’t fire him, and (even with serious behavioural concerns) it would not have been easy for the Minister to have fired him (intense scrutiny, political controversy and all). So perhaps he told Quigley “I’ll go, so long as no one tells the truth about what went on”. By then perhaps it seemed cheap at the price to Quigley (bearing in mind, even more mundanely, that Orr’s record was an an empire builder not as a cutter and chopper, adjusting to budgetary restraint and – as the Bank’s 11 June statement notes by then the Board had accepted that much lower budgets were coming).

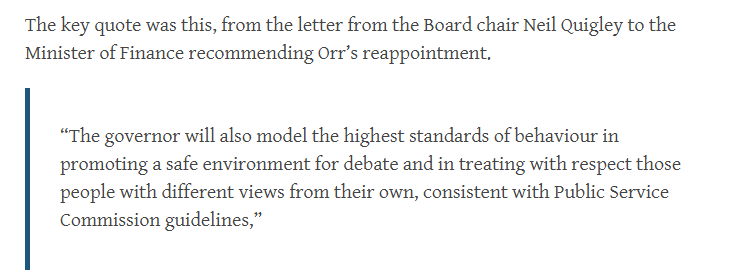

Who knows what items were on that behavioural concerns list, if such there was. Even on the things in the public domain there were so many to choose from over Orr’s time as Governor, let alone all the stories that seep out from those who were there. Why, on the very morning before he’s reported to have completely lost his cool at Treasury, he’d been lying to FEC (again). None of this, sadly, seems very surprising. If there is a surprise it is that the Board had finally – finally – chosen to take a stand. With one exception (new Board member) these board members had all been responsible for recommending Orr’s reappointment in late 2022, when almost all the concerns – well, perhaps not swearing etc at ministers – were already documented. At the time, Quigley signed the recommendation with this

At the time I observed

They must have known then – Quigley more than most (much of the Board was new, but Quigley had been there throughout, chairing the board that first nominated him in 2017) – just how detached from reality that endorsement was. Of course, Robertson will have known too (I’m looking forward to how his book, due out next month, treats Orr).

But, we must be fair, and give the Board some credit for finally acting, possibly under pressure.

What then becomes utterly inexplicable is the decision to lie about what went on.

It isn’t just the press release on 5 March which was spin from start to finish, lauding Orr’s contribution, including in “modernising its culture” (losing your cool and swearing?), or Quigley’s statement – released by the Bank – a bit later that afternoon

We were clearly supposed then to believe that a long-serving Governor was, perhaps, tired, and having done his one big job he decided – Cincinnatus-like – to take a step back and return to private life. It seemed unlikely then. It is pretty clearly outrightly false now.

(As previously documented from the 11 June release, the Bank (Hawkesby) ran the same utterly misleading line to staff.)

And if those statements weren’t bad enough, there was the press conference. Even accepting that Quigley was pushed into doing it by the Minister, surely, surely, he must have rehearsed his lines and tested how he was going to answer the inevitable questions he would face?

At the press conference, Quigley started off with “he felt it was just the right time to go” sort of stuff, highlighting all he’d done. Then when he was asked if the Board still had confidence in Adrian he responded – avoiding the specific question

“My relationship with Adrian has been very good, and I have confidence in Adrian. Yes, he and I have been through a lot in my time as board chair of his time as governor, and with the pandemic and everything else, we have very good memories of the challenges that we have confronted.”

I recall noting earlier that interesting juxtaposition (he claimed he still had confidence, avoided answering about the Board), but how can we possibly now believe Quigley was being honest even reporting his own views. You don’t send a written statement of multi-year behavioural concerns by email and ask, by email, for a response when you have confidence in your CEO (a quiet CEO/Chair chat might be a different kettle of fish).

There were then actively misleading answers about the Funding Agreement before we got this

Q: What has been the precipitating factor to what you call this personal decision?

A: I think you have to remember that the job of the Reserve Bank Governor is one where you face unrelenting critique of your actions. You know, no matter what you do, there are near alternatives that other people say that they would have taken. And so there is a time when you think having achieved what you wanted to achieve, that’s That’s enough.

I suppose just possibly he had in mind some “unrelenting critique” that included the Board, but it was clearly a deliberate exercise in deception, all the more so if today’s account is accurate.

It goes on and on (bringing to mind Peter Mahon’s famous line on Air New Zealand) including

Q: Can you just be clear that no, policy, conduct and performance issues are at the center of this resignation?

A: We have issues that we’ve been working through, but there are no issues of that type that are behind this.

You’ll recall that when challenged on some of this after the 11 June release, Quigley first attempted to fob off questions suggesting he wasn’t going to be grilled by a journalist acting like a courtroom lawyer, only to fall back on the excuse of the supposed gag orders (the details of which have never been released). But gag orders do not oblige (or excuse) chairs of powerful government organisations to go out and actively misrepresent what actually was going on. Don’t hold a press conference if you can’t or won’t give straight answers.

So far, we have heard quite a bit about Orr’s conduct. Quigley’s has long been pretty egregious as well, centred on his repeated and deliberate attempts to mislead as regards appointments to the first MPC (summarised again here). My correspondent added some more, on top of the already documented public cover-up and avoidance of scrutiny efforts around the resignation. According to the correspondent, any records of that meeting with Treasury on 21 February were within-scope of at least one of the OIA requests (not mine). It turns out that Treasury staff at the meeting had written up a record of the meeting (which would seem to be a normal thing to do), but that when Quigley learned of this record he went apopolectic (my word, but captures the flavour of my correspondent’s words) – not just internally, but rang Treasury to complain vigorously. It is reported that in meeting some or other OIA request the Bank so heavily redacted that document that an RB comms manager could boast that they’d rendered it useless. [UPDATE 23/7: Rereading my source, this claim is actually about the Treasury record of the meeting of 24 February with the Minister and Treasury.]

On its own, again perhaps not so surprising. Senior public officials often don’t like stuff being written down – discovery risks and all that awkward stuff, scrutiny – but…..the Official Information Act is the law, and there are overriding considerations of public interest. The Bank’s approach (most likely either acquiesced in by the Board chair or driven by him) has been to release absolutely as little as possible, as inconsequential as possible (so note that the 11 June release had quite a few bits and pieces, but most shed no light at all, and almost none of those that might shed light were released at all. OIAs were – and are being – simply ignored.

The final point in my correspondent’s statement related to an issue I wasn’t aware of at all, and isn’t directly related to the Orr departure. The correspondent claims that the Bank is about to move its Auckland office into one of the plusher buildings down near the waterfront (PWC Tower, which seems to boast all sorts of Orr-pleasing green credentials). I have no way of knowing if this is so, but published board minutes certainly reveal that they were planning to shift and suggest that in March negotiations were still ongoing. The suggestion is that the space being leased is “three times” what would be needed for the staff there, the more so after the Funding Agreement cuts. The report from my correspondent is that management – post Orr – suggested reconsidering (optics, job losses, and all that) but that the Board itself refused, and that by the time the final decision was made the Board knew the lower level the new Funding Agreement would be set at. My correspondent seems very confident about all that, but notes that they are not sure of the reasons, reporting only a general sense among Bank people that the Board had wanted fancy spaces for themselves. Staff will speculate, staff may have that one wrong, but it doesn’t sound like a very good look at all. Again, occurring on Quigley’s watch.

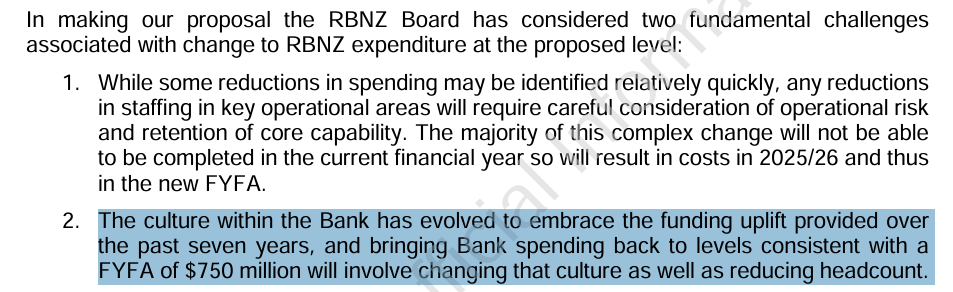

If offence it is, it is certainly one of the lesser ones, but it does point in the direction of the Funding Agreement not actually having been cut to the bone. You’ll recall last week’s post that the Bank’s operating expenses in 2025/26 will be 12 per cent above the level in 2023/24, the last year budgets were set under Labour, and that line about the culture of excess that Quigley had included in his last ditch bid in March to limit the cuts the Minister was going to impose.

This has been a long post. As noted earlier, I have lodged a number of new OIAs, with the aim of trying to verify as much as possible of what is reported here. I expect there will be more obfuscation and outright ignoring of requests, although if so that will be telling in itself.

None of it leaves anyone looking very good (although perhaps it partly redeems the standing, at that late date at least, of the Board members other than Quigley). We have not had straight answers yet from either Quigley or the Minister of Finance (and have heard nothing at all from Orr, which might perhaps be more understandable if he really was close to having been forced out on conduct/behavioural grounds). And OIAs continue to be ignored.

If this were just any junior public servant of course things would be different. There would be no particular public interest in disclosure. But we are talking here about the sudden departure of one of the most powerful and highly paid officials in New Zealand, who had often boasted (mostly not correctly) of how open and transparent he and his institution were. And yet someone who used his office to treat people poorly, in some cases (it seems) abominably, and of course who had such a questionable policy record too – all that (core) inflation, all that economic dislocation, those $11 billion of losses for taxpayers. We deserve some honesty. And it remains almost beyond belief that after all this not only is Neil Quigley still in office, but that he is now leading the search for the nominee for a new Governor. Because his last pick worked out so well?

A month ago, I wrapped up a series of posts on these issues with one posing 41 Questions for the Board, for Quigley, for Willis, for Treasury, and for the temporary Governor Christian Hawkesby. Most remain outstanding.

UPDATE: I hadn’t known there was any accessible footage of Quigley’s 5 March press conference (and some Wilis comments) but here is a link that contains many of his answers. Nothing new beyond what I’ve previously quoted from a written transcript, but fyi.