Yesterday’s post focused on the puzzling events around the adoption of last year’s Reserve Bank budget: the board planned to spend massively above what the Funding Agreement had allowed and for reasons still totally obscure neither Treasury nor the Minister of Finance raised any concerns whatever.

A few months ago now, after Orr had left the scene (with many questions still unanswered), a new Funding Agreement for 2025-30 was signed. I noted then that while the new spending allowances were well down on what the Bank had itself egregiously planned to spend in 2024/25, they didn’t appear to represent much of a cut at all relative to previously agreed levels (past Funding Agreement and 2023 variation), despite the huge increase in allowed spending that had been granted on the Orr-Quigley-Robertson watch. A few weeks ago – and only a day or two beyond the statutory deadline – the Bank released its Statement of Performance Expectations (SPE) for 2025/26. You’ll recall that, by law, the Minister (and hence Treasury) will have had a chance to provide comments on the draft.

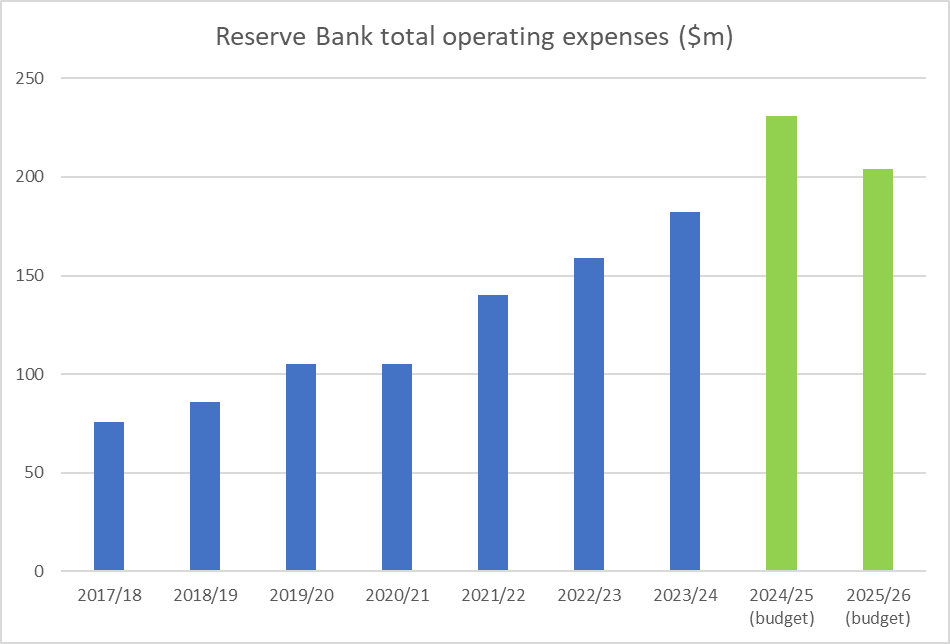

The SPE contains the Bank’s budgets for 2025/26, and enables us to use some directly comparable numbers over time for total operating expenses. One of the sleights of hand in the new Funding Agreement was moving more items – some potentially quite significant – out of scope of those particular limits. It turns out that in the Bank’s 24/25 budget 13 per cent of operating spending was out of scope, while in their 25/26 budget, as reported in the SPE 24 per cent is.

It is fair to observe that the relationship between recent Reserve Bank budgets and actuals seems to have been surprisingly loose – Orr seems to have been unable to spend all the money that board allowed him when they set annual budgets – but for 2024/25 and 2025/26 budgets are all we have to go on. For 2024/25, the Minister was still happy to have used the budget numbers in her March Cabinet paper on the new Funding Agreement and we know (from that document) that there had been a big increase in actual staff numbers (FTE) between 30 June 2024 and 31 January 2025 (up about 10 per cent in 7 months), and staff expenses are by far the largest item of opex.

Anyway, here is the best chart I can put together, using Annual Reports for actuals and the SPE budget numbers for 2024/25 and 2025/26.

Since the Bank has been in full-on retrenchment mode in recent months (eg top management numbers have more than halved, and they’ve been reduced to laying off a quarter of their first and second year new graduates), it isn’t impossible that the 2024/25 actuals will come in a fair way below the budget adopted last June (although there will be unforecast redundancy costs).

But what really caught my attention was the budget for 2025/26. You’d have to think that, having been adopted only last month, with a Board chair and temporary Governor wanting to show how they’ve moved with the spirit of the times, these aren’t vapourware numbers, but the best hardnosed estimate of what the Bank expects operating expenses to be in 2025/26. That number is 12 per cent above actual operating expenses in 2023/24, the last year in which budgets were adopted under the previous government – the one the current Minister of Finance rightly and regularly attacked for extravagant levels of spending. 12 per cent above…..(this only becomes apparent now because it is only now that we can put hard numbers on how much spending was moved out of scope of the Funding Agreement limits, in a way that allowed the Minister to sell the extent of restraint as materially greater than it turns out to have been). How many other government agencies have budgets this year 12 per cent above levels of spending in 2023/24? Not many would be my bet. It is quite astonishing.

(Yesterday, I linked to someone else’s OIA published on the Bank’s website. It included this plaintive appeal to the Minister of Finance not to cut the funding agreements amounts further in a report dated 14 March

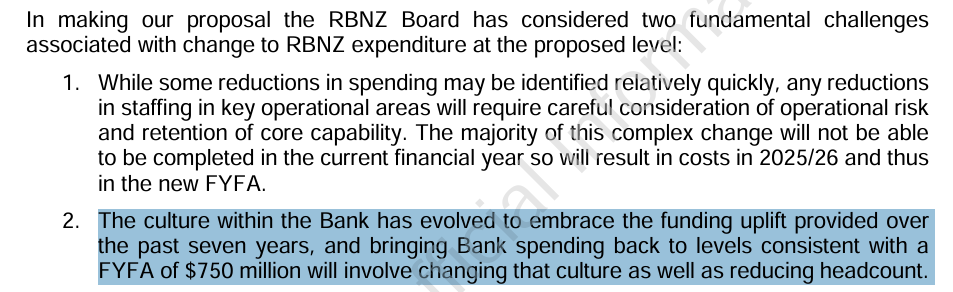

The Board chair owning up to the culture of excess that had developed over recent years. Who had been the board chair right through that period? Why, that would be Neil Quigley. Who is the board chair still today? Why, that is Neil Quigley. )

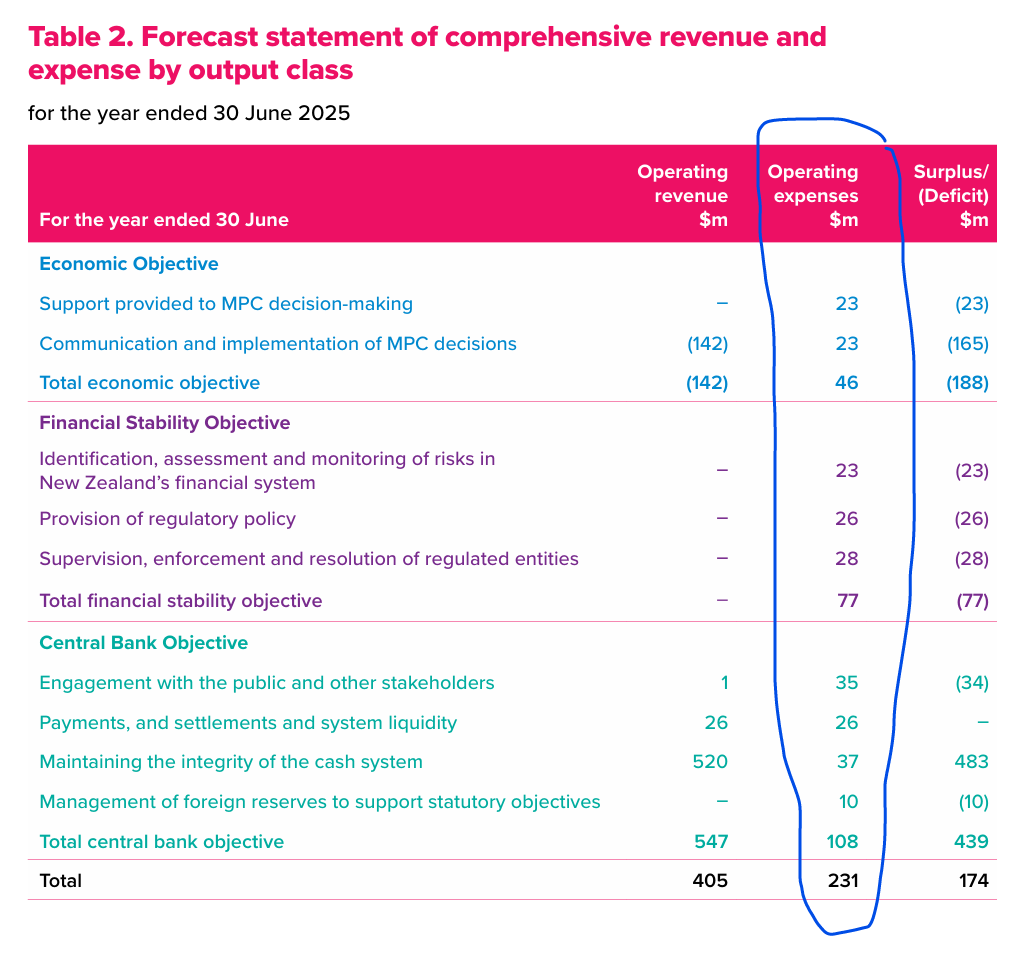

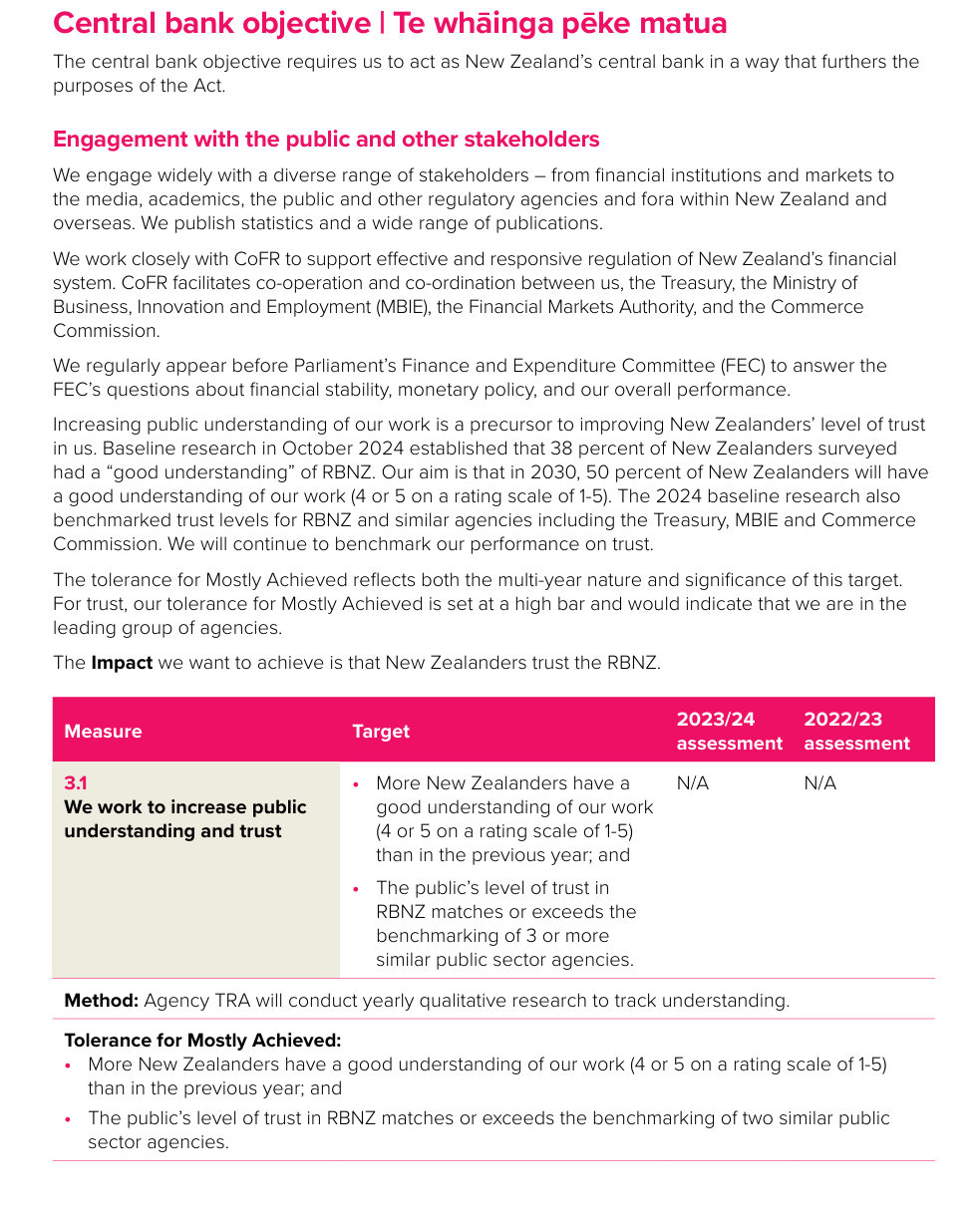

What of the rest of the Statement of Performance Expectations? It is very little use to anyone (I’d have thought). There is less of a breakdown of planned spending this year than last. This was from last year (bother only about the spending column)

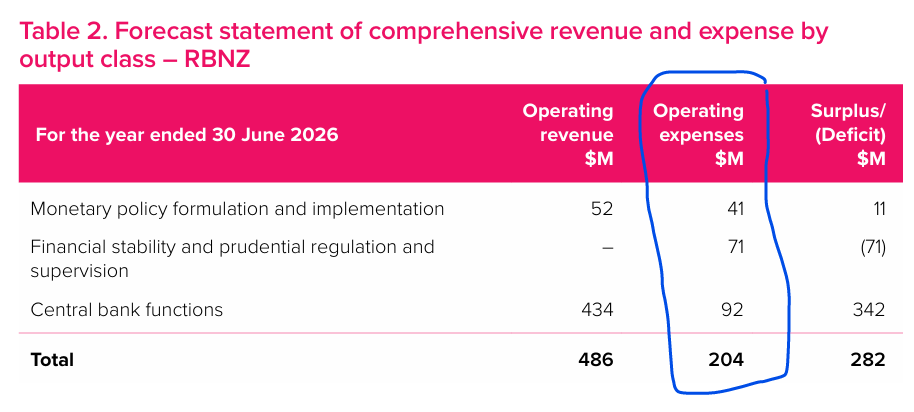

It raised several questions then (I had a post about the extraordinary $35 million of planned spending on “engagement with the public and other stakeholders”, which seemed so egregious that the truth surely couldn’t be quite as bad as it seems (but we have never any answers). This year, they’ve collapsed the categories so we get only this

With that utterly-meaningless “central bank functions” heading hiding almost everything that might be interesting.

And then there is this (with no numbers at all)

After the six months the Bank has had (coming on the back of the last few years – $11bn of losses, worst outbreak of inflation in decades), you really wonder how they can write this stuff with a straight face. But I guess that is the sort of quality bureaucrats (and associated board members) are recruited for. Well-grounded trust usually requires a record of achievement or at very least a record of open and self-critical transparency when things don’t go so well. The Orr-Quigley-Hawkesby Reserve Bank is still failing on both counts. A Governor just disappears, with no notice and no explanation. Or recall all those unanswered questions in my recent post (let alone all the ongoing OIA obstructionism), and the inability to even give straight answers regarding the actual level of spending restraint when the Funding Agreement was released three months ago. (Note too the odd benchmark: while the Commerce Commission has some independent powers, Treasury and MBIE are simply ministries whose activities or advice are rarely directly visible to the general public in a way the Reserve Bank’s independent exercise of its powers is. They aren’t similar, and I don’t think “no worse than how the public thinks of (or trusts) Treasury” is really an adequate benchmark at all.)

Isn’t it bordering on criminal to collapse the categories?!?

There should be a law against bulking up such huge amounts against such vague “descriptions”.

SURELY the Min of Finance should act when Quigley admits/concedes a culture of excess has “evolved” during his reign!!

LikeLike

Pretty poor show all round. So many pages, so little substantive content.

As for Willis, I don’t understand her choices around the RB and Quigley at all. There is no obvious logic to it – he hasn’t really proved even to be a safe pair of hands. My working hypothesis is that as there are no votes in RB things these days she really doesn’t care. Don’t like to believe that is the story, but otherwise it is hard to reconcile her approach, incl towards Orr, in Opposition (when inflation was high etc) to how she’s operated in office.

LikeLike

Nicola appeared to be v tough in opposition, and still talks tough at times. But she’s a worry, esp when we’re seeing an increase in the national debt and RBNZ wastage is anything but peanuts…..

LikeLike

It maybe she was advised to limit the appearance of political interference in the activities of the reserve bank. This helps maintains the integrity and independence of the institution which plays well globally and in markets.

LikeLike

Replacing the chair at the end of his term would certainly not have been seen as inappropriate political interference (after 9 yrs in the role)

LikeLike

I note your disappointment in the way Orr did a magic act and disappeared in a puff of smoke only to re-appear wearing a Toga and jandals on a Pacific island recently as if nothing happened.

The one observation I would make in Orrs favor is that his departure caused hardly a murmur. The markets had faith in the institution of the RBNZ itself, and things continued normally.

Now this outcome might be down to the larger and more collegiate board and collaborative culture that Orr encouraged during his tenure. In other words, it wasn’t all about one person or the leader – he created an environment in which he was no longer needed.

This is a good attribute in a leader.

LikeLike

I don’t begrudge Orr his Cooks role at all. I hope he can add some useful value.

“Collegiate board and collaborative culture” however does not for a moment sound like Adrian. It was one dominant person. As for markets, you wouldn’t really expect an impact unless the departure was because of some monetary policy dispute (and there was never any suggestion of that). From a markets perspective, the waters closed as smoothly over his head as they did when Don Brash – hero of the disinflation years, symbol of the independent RB, to many – resigned in 2002. For better or worse, issues of public sector governance – the sorts of things in yesterday’s post and today’s – are of little moment to wholesale investors (they should however matter to NZ voters)

LikeLiked by 1 person

I’ve tried engaging withe the RBNZ regarding the operations of the fiat currency monetary system in NZ.

For example, where does the money come from that is used for transfers into Cash Settlement Accounts that commercial banks use for government spending.

Initially I was told that taxes are used to fund government spending and that bonds are ‘debt’ and not term deposits.

In the end they told me they did not have sufficient staff to discuss my questions in detail – which is fair. These are not highly expert economists at the contact team.

LikeLike

That’s a shame. When I was young and everyone had to engage by letter we regarded it as a good discipline for young economists to be able to make sense of where people were coming from and engage simply and clearly on how we thought about the monetary system.

LikeLiked by 1 person

I’m probably trying to be cleverer than I am and I still have much to learn and understand – including communication skills – so I accepted their response as a reminder to practice humility and to continue learning.

LikeLike

Bonds are a debt instrument by which the government borrows, quite separate from the RBNZ Cash Settlement Account. That is correct. Nothing wrong with that answer. The RBNZ Cash Settlement Account was only used as a last resort borrowing to enable the government and Treasury the facility to borrow up to $100 billion during a period of Covid instability without the normal market driven pricing of risk. The RBNZ only drew up to $59 billion of the planned $100 billion, but actually used only $32 billion for the Covid response. Likely around $10 billion went towards taking over full ownership control of Kiwibank from its previous National Superannuation and NZPost owners. The RBNZ books are being cleared up by the government each year at around $5 billion a year. The dispute with Adrian Orr likely over how quickly the government was prepared to clear the RBNZ books of that artificial Cash Settlement Cash liability that was created artificially for the Covid response.

Most economists, including senior top economists do not understand the transaction flow to explain to you because those are actually Accounting book transactions which you have to speak to highly specialised Accountants as to how those artificial transactions were created that moved billions of dollars around like cash on a monopoly board game.

LikeLiked by 1 person

Thanks getgreatstuff. This is where I like to go into the weeds and examine the real-world operations of fiat currency monetary systems and the true nature of money.

What is interesting is that the creation of the liability at the RBNZ for COVID (and presumably other macro-economic shocks) is that it has no impact on the functioning of the private sector.

In fact, it implies that the existence of a stable private sector is dependent on the ability of a reserve bank to absorb failure and risk onto its balance sheet. Furthermore, there is no compelling argument to pay down the liability other than conformity and convention.

The application of double entry accounting is critical and the above supports the MMT statement.

public sector deficit = private sector surplus

My other point is to disagree with you on the nature of bonds. They are not a ‘debt’ instrument for the following technical reasons.

Debt is a loan from a commercial bank where the loan principle is created out of thin air as new money that is put into circulation. When that principal is repaid it is destroyed i.e. the bank can’t re-use that money for another loan – it can only be created once.

A term deposit is when you take your own savings (already created money in circulation) to the bank and agree to a return on the savings for a given period of time. This removes money from circulation – the opposite of a loan. When the term deposit is completed, your savings are returned into circulation.

Government bonds are term deposits – they remove money from circulation and return it to circulation at a later date with interest. Government bonds are a safe harbor asset for investors – they provide the risk-free baseline that underpins other assets in a portfolio.

Technically the government does not borrow money – it provides a service to private sector savers to protect surplus income and withdraw money from circulation to control inflation.

The government creates money to spend. It has limitless overdrafts at its own bank, and these are used in the first instance to pay for resources in the private sector as agreed in the budget.

Taxation and bonds are inflation tools used to withdraw excess money from circulation after it has been created.

Michael – if you have time can you verify or dispute the above description on general technical accuracy.

LikeLike

Depends on which side of the fence you are sitting on as to whether a Bond is a debt if you are with the government or a deposit if you are an investor. There is no right or wrong. This is the reason the RBNZ has no free staff to speak to you. It is a circular argument and there is no right or wrong. It comes down to your perspective as to which side of the fence you are on.

LikeLike

Thanks getgreatstuff. I have to disagree with you – I think the “it depends on which side of the fence you sit” argument ignores the actual reality of what happens.

Without taking any political or economic view map out the technical operations that take place in a fiat currency monetary system and you will observe that government spending creates new money and increases the money supply. A commercial loan from a bank does the same thing.

Government bonds remove money from circulation which reduces the money supply – an inflation control activity. Not a loan – just like a term deposit is not a loan – you take existing money and save it with the bank. A term deposit does not create new money.

It is really important because the stories we are told about the economy (and to be honest macro-economics is not even part of the story) inform economic policy and real-world outcomes for people’s standard of living and quality of life.

I find it very frustrating that economists justify the use of the household budget analogy for a government because people can understand it easily.

Imagine if Einstein or Galileo had taken the same approach to their fields of study and expertise.

Modern economics is a fraudulent fabrication, and everyone is perfectly happy with it being that way.

LikeLike

“In fact, it implies that the existence of a stable private sector is dependent on the ability of a reserve bank to absorb failure and risk onto its balance sheet. Furthermore, there is no compelling argument to pay down the liability other than conformity and convention.”

The RBNZ does have a important role in the stability of the Financial sector. Actually for me, that obvious important role of the RBNZ, I only started to understand was during the Covid response and the continuing strength and confidence in the NZD. Remember that NZ does not make and sell many products for overseas consumption but yet the NZD is the 11th most traded currency in the world which is a billion dollars traded every day and $350 billion traded every year with only an export trade of around $80 billion a year which is a clear indication of the confidence in the NZD.

The compelling reason why debt is repaid is because it is not your money that you are borrowing. It belongs to someone else. If debt is not repaid then no one would have the confidence to lend you the money to spend freely in the future. Our trade flows are dependent on debt being repaid. No one will sell you product if you can’t pay for it with a respected currency like the NZD and we live on imported products. If you don’t pay your debts the NZD will collapse and you will need a wheelbarrow to buy a loaf of bread.

LikeLike

“The compelling reason why debt is repaid is because it is not your money that you are borrowing. It belongs to someone else. “

If reserve banks simply create money or liability by typing values into accounts on the public sector side of the ledger – without ‘borrowing’ or removing any money from the private sector – who are we repaying in the private sector to pay down that ‘debt’?

Which private sector bank or bond issuance do we have to return that money to?

The answer is no-one. In the above scenario the reserve bank has not borrowed any money from the private sector – so who are we repaying and why?

It’s an entry on an account on the public sector side of the macro-economic ledger.

LikeLike

“I find it very frustrating that economists justify the use of the household budget analogy for a government because people can understand it easily.”

If you are trained in the Financial sector, the real world of money comes down to a very basic set of Financial Statements but don’t forget a highly robust audited by an army of Accountants set of books.

1. The profit and loss statement – what is my income versus what is my cost and do I have a profit that I can put to savings.

2. The Balance Sheet or Statement of Financial position – what assets, savings, house, car, I have and how much I have borrowed and owe others.

The government does work in exactly the same way. It is not new economics. It is a recognition that is how the real world of money works.

The confusion arises because the government does have the ability to print unlimited money. But that is where the RBNZ plays an important role and one key reason why we have a RBNZ. It is to prevent the government from freely printing money.

The Quantitative Easing Covid response we must be very clear was not a money printing exercise but an asset swapping exercise. There was not a dime printed. All of it was borrowed from every Financial Institution that held existing NZ Treasury bonds that was licenced and had a Settlement Cash Account with the RBNZ.

Why borrow instead of print? It is the real fear of the devastating devaluation of any currency of a government that prints currency freely.

Quantitative Easing was a set of simple accounting transactions but yet a very complex set of legal behind the scenes negotiations and legal documentation with the RBNZ waving a big stick. The transactions required are on both the RBNZ books and it does also affect the private sector Financial Institutions books that had to book the transactions in the opposite ie Book a liability on the RBNZ books and book an asset on the private institutions books.

LikeLike

The Quantitative Easing steps are as follows. For ease of understanding we will call the existing NZ bonds as Old NZ bonds and the new issued bonds as New NZ bonds. During QE there is at play Old NZ Bonds and New NZ Bonds

The RBNZ buying the Old NZ Bonds from all the Private Financial Institutions meant that there was now a vacuum of NZ Bonds on the Private Financial Institutions books. Any Banking or Superannuation or Life fund requires to maintain a Balanced investment portfolio that requires a certain amount of NZ Bonds. Having sold up all the Old NZ Bonds to the RBNZ, they must now approach the government and Treasury to buy New NZ Bonds. This is how Quantitative Easing Covid respond was funded. New NZ Bonds were issued by the government to the Private Financial Institutions to replenish the Old NZ Bonds bought up by the RBNZ.

LikeLiked by 1 person

Thanks greatstuff. This is where the magic happens.

LikeLike

Fantastic breakdown. So, in essence the RBNZ swapped newly created money for already issued bonds. Effectively returning savings into circulation early – before the natural maturity of the old bonds.

The new deposits in PI accounts were then used to purchase new bonds as required to meet portfolio requirements etc. and this purchase withdraws the new money from circulation again.

So, what was the point in these transactions exercise? If memory serves me correctly it was something to do with protecting private sector investors from changes to bond interest rates. I.e. the reserve bank absorbed losses that would otherwise have been absorbed by the private sector.

LikeLike

This is where Economists get completely lost. The Settlement Cash Account is not an Asset on the RBNZ Books. Although it is called the Settlement Cash Account, It is actually a Liability Account on the Balance Sheet. For you to more simply understand the QE transaction, the RBNZ approached the Private Financial Institution and said, I will buy all your Old NZ Bonds. I will not pay you Money for the sale but I will give you an IOU via the Settlement Cash Account. You can book an equal and opposite Asset ie I, the RBNZ am now on your Private Financial Institute books as a Debtor.

Under normal circumstances, the Settlement Cash Account functions as a Clearing Account or otherwise called the Exchange Settlement Account System (ESAS), and facilitates the settlement of interbank transactions and other payments between financial institutions. ie Money In and Money out. Under QE, the function changed and it becomes an Overdraft Account or an IOU Account.

No Actual Money is transferred for the Purchase of the Old NZ Bonds.

QE was actually funded by new money that the Private Financial Institutes that have to buy New NZ Bonds from the government. New Money had to be coughed up from their shareholders or otherwise borrowed from other sources using the strength of their Balance Sheet with that guaranteed IOU from the RBNZ and the profit from the Sale of the Old NZ Bonds. It is actually new money supply.

LikeLike

Thanks greatstuff. What was the purpose of these transactions? Michael has complained on this blog before that the RBNZ ‘lost’ $11 billion from the process you describe and I’m guessing this $11 billion is what the private sector stood to lose when interest rates changed, and bond values fell or rose in some particular way.

So, in effect the $11 billion liability on the RBNZ side of the ledger is the absorption of a private sector failure or mistake that destroyed savings or value in some way.

Have I got that right?

LikeLike

Isn’t this a bit of a joke, when acknowledging how many extra staff they have added recently? “they told me they did not have sufficient staff to discuss my questions in detail”

LikeLike

The questions being asked are of the artificial transactional entries of the RBNZ Settlement Cash Account and the associated issuance of NZ Treasury Bonds. These are questions that are actually in relation to the Quantitative Easing, Covid 19 response. It is not a question that most Economists can answer. This is in the the realm of highly specialist Accountants as it involves the manipulation of the RBNZ’s Balance Sheet by the creation of artificial book entries.

LikeLiked by 1 person

Yes – exports are one way to create new money and grow the money supply. In a modern economy trade flows are a critical component in the mix, but exports are not a silver-bullet, magic solution because they are subject to forces completely beyond your control.

Sometimes exports support your money supply and sometimes they don’t – ask Germany.

I’m not arguing that debt should not be repaid or that bonds (savings) should not be returned – in the private sector. You noted earlier the importance of double entry accounting so now apply that at the macro-economic level between the public and private sectors of the economy.

What would happen to the private sector if the reserve bank just left its balance sheet as is and didn’t worry about it too much – like the Bank of England did after the GFC or COVID.

As soon as a reserve bank starts to pay down their liabilities they are removing money from circulation in the private sector so it would need to be part of an inflation fighting cycle not just to ‘pay down the debt’.

Again, I come back to double entry accounting – public sector deficit = private sector surplus.

If the public sector settles liabilities at the reserve bank it is reducing the money supply in the private sector. If governments run an operational surplus they are reducing the money supply in the private sector.

Contracting the money supply should only be done during inflationary upswings or in an overheated economy.

LikeLike

As far as Private Financial Institutions are concerned, Debt has to be repaid or interest is paid on the Debt. The RBNZ decided to pay interest on the Settlement Cash Account Liability at the OCR rate. Now the tricky part. How to repay the Settlement Cash Account Liability owed to Private Financial Institutions?

This is where it starts to get murky.

1. RBNZ borrows $59 billion but the Covid response was only worth $32 billion. What happened to the remaining $27 billion?

2. Westpac offers its NZ subsidiary for sale and undertake due diligence from interested parties. Why?

4. Grant Robertson, Finance Minister was giving away cash freely in the First Covid lockdown and had undertook to spend freely again under the @nd Lockdown but decided he had run out of cash in the 2nd Lockdown after only burning through $32 billion. Why?

5. 10 RBNZ Officers resign. Why?

6. How did the government end up in full ownership of Kiwibank seizing 100% share ownership from our state owned pseudo Private Financial Institutions, National Superannuation and ACC?

7. What happens to Bond values when the RBNZ raises interest rates?

LikeLike

Does the RBNZ ‘borrow’ money – who is it borrowing that $59 Billion from? Is it going to a commercial bank or the bond market for that $59 billion? Or does it just type values into accounts at the reserve bank?

LikeLike

Read the discussion above previously. I repeat. The RBNZ borrows via the Settlement Cash Account by recording the following entries.

The Settlement Cash Account is a Liability account on the RBNZ books. It means that the RBNZ owes someone ie a Liability.

RBNZ takes a immediate loss on the purchase of the Bonds of $5 billion. Subsequent losses are due to interest payable on the Debt via the Settlement Cash Account. Also Bond Values decline as Interest rate rises which can lead to the $11 billion loss that the RBNZ has indicated that they have sustained undertaking QE

LikeLike

getgreatstuff “The Settlement Cash Account is a Liability account on the RBNZ books. It means that the RBNZ owes someone ie a Liability.”

In double entry accounting that liability sits on the public sector side of the ledger – the reserve bank is a public sector institution. Who is the ‘someone’? they need to repay to settle that liability?

Where getting deep into the weeds here but it lies at the heart of MMT’s observations about fiat currencies.

You are still avoiding answering my question – who in the private sector side of the economy is the RBNZ liable to – for the $59 billion?

I asked ChatGPT

Hi Chat – I’m in a discussion with someone about the LSAP programme that the RBNZ did during COVID.

I’m trying to understand where the RBNZ got the ‘money’ from that it used to make the purchase.

Does the RBNZ ‘borrow’ money – who is it borrowing that $59 Billion from? Is it going to a commercial bank or the bond market for that $59 billion? Or does it just type values into accounts at the reserve bank?

Answer:

The RBNZ did not borrow the $59 billion it used for the LSAP programme.

It created the money — digitally — by crediting the reserve accounts of commercial banks at the RBNZ.

The LSAP (Large Scale Asset Purchase) programme involved the RBNZ buying New Zealand Government Bonds (NZGBs) on the secondary market (i.e. from banks, financial institutions, not directly from Treasury). The stated aim was to:

Where did the RBNZ get the money?

It created it out of nothing, as central banks can do.

When the RBNZ buys bonds under LSAP, it pays for them by:

This is not funded by taxes, and not funded by borrowing from the public or the bond market. It’s an asset swap:

The RBNZ simply updates its balance sheet:

This is digital money creation, not borrowing.

Is ChatGPT technically correct here? Michael, getgreatstuff I would love to hear your thoughts on this – time permitting.

LikeLike

Lets get onto the interesting part, ie how does the RBNZ remove the Settlement Cash Account of the debt owing to the Private Financial Institutions of $59 Billion?

LikeLike

I understand what you are saying about the commercial banks deposits at the reserve bank – the RBNZ pays interest on them and is liable to take care of the money and settle it if required etc.

From Chat:

Think of it like this:

Just like you have a deposit at ANZ, and:

Banks have deposits at the RBNZ, and:

The RBNZ sees them as liabilities — because it “owes” the banks that balance.

The banks see them as their money (their settlement cash),

LikeLike

Greatstuff – I chucked your comment into ChatGPT and here is its response:

What’s true (or mostly true):

❌ What’s misleading or wrong: 🚫 “The RBNZ has to remove the Settlement Cash Account debt”

This misunderstands how QE works:

🚫 “Government now has $118B in bonds issued (Old + New)”

No — this double counts. The RBNZ bought existing bonds (Old) from the market — those still exist but are now held by the central bank. The government only counts what’s outstanding to the public (excluding what’s held by the RBNZ) as its “net core Crown debt.”

Also:

🚫 “Robertson had $59 billion in real cash to fund UBI”

🚫 “RBNZ pulled the plug, paid back $27 billion to PFIs”

🚫 “10 RBNZ officials resigned over this”

💡 So what’s actually going on?

Here’s a clearer, reality-based version of events:

No record of “$27B repayment” or RBNZ pulling the plug.

RBNZ LSAP (2020–2022):

RBNZ bought ~$59B of government bonds to keep interest rates low.

Created $59B in settlement cash (liability) and held bonds (asset).

Government fiscal response:

Government issued new bonds to finance ~$30–40B of COVID-related spending.

This was enabled by strong bond market demand, partly thanks to QE.

Aftermath (2022–2025):

Interest rates rose → RBNZ incurred losses on bonds + OCR payments.

QE ended → RBNZ allowed bonds to mature without replacing them (QT).

Settlement cash balances declined as a result — slowly, not suddenly.

LikeLike

Love it greatstuff. Absolutely agree that governments cannot print unlimited money and that all new money has to be countered with controls on the overall money supply to prevent inflation – taxation and savings. The money supply at any point in time has to reflect the real- world capacity and potential (under utilized labor and resources) in the economy.

The problem is, in part, that we allow the eternal accumulation of excess currency and this creates asset bubbles and ridiculous financial engineering that diverts money from useful and productive activities.

In addition to increasing taxes – bring back the accumulation crushing 90% top tax rate, compulsory savings and how about currency expiry – this could be done in the bond market by extending and rolling over terms of the bonds that banks are forced to buy.

Allow the government space in the economy to deliver the welfare state in full and provide a stable level of employment and capacity in the economy across private sector cycles.

LikeLike

“Detailed breakdown of Net Core Crown Debt

2019: Net core Crown debt was $57.0 billion, or 19.3% of GDP.

2020: Net core Crown debt increased to $77.0 billion.

2021: Net core Crown debt increased to $103.5 billion.

2022: Net core Crown debt reached $124.4 billion, or 38.5% of GDP.”

Google AI derived Net core Crown Debt between 2019 and 2022.

It was purely human reasoning that I came up with the number $118 billion ie $59 billion RBNZ debt purchasing Old NZ Bonds plus Treasury issued $59 billion New NZ Bonds for the Covid19 Response Support payments. If the RBNZ borrowed $59 billion to buy $54 billion of Old NZ Bonds, then Treasury would have just raised cash to spend the equivalent $59 billion by issuing New NZ Bonds.

The actual Crown debt for the Covid response looks like the difference between $124.40 billion (in 2022) – $57 billion (in 2019) = $67 billion. As you indicate some secondary market debt.

Net Crown debt effectively more than doubled during the Covid response period between 2019 and 2022.

Conclusion is that my human reasoning is not wrong because the actual numbers speak for itself.

There has been more than a doubling of Net core Crown Debt between 2019 and 2022 which is very much in line with my human predictive modelling and the failure of your ChatGPT AI reply.

LikeLike

Thanks Greatstuff. I suspect we are both saying the same thing, but I am trying to understand the nature of the reserve bank balance sheet where a liability is an asset in the private sector. For example, the $11 billion dollars the reserve bank absorbed as a loss to protect private sector savers – pensions funds exposed to changes in bond yields and bond values.

As to your calculations – I’ll need to dig into these more to understand what you are saying. It is key to remember that governments don’t borrow money from the private sector. They create new money all the time as they spend – room has to be made for this new money to prevent inflation.

Bonds are issued to remove existing money from circulation to make room for new money that the reserve bank creates for government spending. Yes, the bond issuance has to be met on maturity or rolled over but because the government creates new money to meet its obligations this isn’t technically a real problem.

Yes – inflation and currency value are a problem – I’m not saying there are no real-world consequences.

Anyway, I’ll spend some time going through calculations and see what you are saying.

LikeLike

Lets stick to hard numbers rather than deal in definitions otherwise you will end up in a circular argument.

You must also remember that the RBNZ ultimately is a Crown entity. It is not a separate and independent third party.

The RBNZ makes independent judgement but ultimately whatever the RBNZ Balance Sheet shows on its public webpage, those numbers must be consolidated onto the governments Crown books.

So whatever logic you decide, the ultimate truth lies in the governments Crown books ie what is the Crown core debt. It will take into account whatever liabilities the RBNZ takes on board.

The RBNZ books are relatively straight forward. I repeat.

The reason why I believe that Grant Robertson had thought he had $59 billion cash in hand for the Covid Response is because Treasury most likely did issue $59 billion in New NZ Bonds.

But somewhere along, $27 billion cash never eventuated and disappeared which resulted in only a $32 billion Covid response support.

The additional Journal entry, I have just recorded is the likely transfer of the $27 billion from the Private Financial Institues to the Crown. This is shown as the reduction in the PI Settlement Cash Account Liability and was replaced by an entry with the Crown Settlement Cash Account Liability.

In total, the Settlement Cash Account Liability is still the same at $59 billion on the RBNZ books but the Private Financial Institutes got paid out $27 billion and cleared of the liability and is now held by the Crown Settlement Cash Account Liability.

I did think that perhaps, Treasury only issued $32 billion in New NZ Bonds but then you would have 10 senior Treasury Officials departing instead of 10 RBNZ officials. Clearly someone would have paid the price for the missing $27 billion that Grant Robertson was planning to spendup on the 2nd Lockdown, and his grand vision for the Universal Wage went down the proverbial drain.

LikeLike

The Kiwi Bank buyout and transfer of ownership from ACC, National Super and NZPost to the government Crown ownership is part of the bailout of the risks of undertaking QE where you are replacing higher interest Old NZ Bonds with a almost zero interest rate New NZ Bonds.

The largest holders of NZ Bonds are actually ACC and National Super. National Super is a $82 billion Fund and ACC is a $60 billion fund. Most of National Super is invested in NZ Bonds. ACC has a more diverse investment Fund but still hold a significant amount of NZ Bonds.

What is interesting about National Super is that it’s declared nominal value holdings in NZ Bonds is actually $105 billion. This does suggest that there is at least a 20% decline in the Market value of the NZ Bond holdings in its Fund compared with the Nominal or original invested value of the NZ Bond since the Fund is only valued at $82 billion.

The final piece of the puzzle. Who is at the end of the Private Financial Entity(PI) Settlement Cash Account Liability. I think there is only 2 remaining parties to the original $59 billion Settlement Cash Account Liability.

1. The Crown Settlement Cash Account Liability $27 billion

2. National Super Settlement Cash Account Liability $32 billion.

ACC being a third party funded entity would likely have been removed from the QE scheme early and as quickly as possible with the Buy Out of Kiwi Bank part of a Bailout solution of declining Bond values as interest rate rises.

The reason at the time to quickly remove any third party Private Financial Entity from Quantitative Easing Scheme is the risk to the NZ Bond Market values when RBNZ started cranking up interest rates. Bond values fall when interest rate rises.

LikeLike

Thanks greatstuff. I still struggle with all of the transactions you describe and where they sit in terms of the private sector. But I do understand what you say about bond value and the yield. Which is very confusing – but essentially the holders of existing bonds lost value (private sector savings were destroyed) when the value of the bonds they were holding fell.

The RBNZ intervened and effectively swapped the old bonds for new ones in order to restore the lost value to the original bond holders.

Anyway – I need to work. Will dig into the numbers another time.

LikeLike

Michael, I’m unsure how you view the prudential requirements/retentions that Adrian wanted to impose/increase on banks? As I understand it, Orr wanted to raise the bar to a higher level than most other countries, and that – since his departure – RBNZ has backed off a bit.

I’ve long been interested in OpenBanking and how well it seems to have developed in the UK in particular (thanks to Govt intervention Vs NZ’s weak “encouragement”).

So I saw a reasonable relaxation as helping to stimulate competition.

For that reason, I’m asking what you think of this news today about the UK from the Guardian “Chancellor Reeves has announced a raft of changes in what the Treasury describes as the “biggest financial regulation reforms in a decade”. Her plans include loosening rules on the financial sector, increasing innovation, and allowing lenders to offer mortgages at more than 4.5 times a buyer’s income. “We have been bold in regulating for growth in financial services and I have been clear on the benefits that that will drive: with a ripple effect across all sectors of our economy putting pounds in the pockets of working people,” Reeves said..”

LikeLike

I thought Orr went too far and that a robust cost benefit analysis would not have supported anything like what ended up being done. It is an open question whether anything much will change as a result of this year’s review but I reckon there would be a good case for stopping further increases in capital requirements from here. Much may depend on the new Governor, whoever he or she may be.

My bigger objection is actually to LvR and DTI restrictions for which there has never been a decent justification. I believe the Ministry for Regukstion should be reviewing these restrictions with a view to having them removed (and power to impose or remove them should be shifted back to the govt rather than left with the RB)

It isn’t clear to me yet (incl reading her FT oped how far Reeves proposes to go but winding back their DTI restrictions would be a start.

LikeLike