I’m pretty tied up for the next couple of weeks so unless there are significant new developments (things like, for example, complying with the OIA) this will be my final post on events around the Orr resignation for the time being.

We know from what the Reserve Bank did choose to release last week that their story is now one in which Orr’s behaviour triggered by the prospect of deeper cuts to the Bank’s next Funding Agreement than he would have liked was what led to the departure. That is the gist of the (no doubt lawyer-vetted language) of the statement/press release last week:

“This caused distress to Mr Orr and the impasse risked damaging necessary working relationships, and led to Mr Orr’s personal decision that he….could not continue in that role with sufficiently less funding than he thought was viable for the organisation”. They wouldn’t have included that “this caused distress” stuff if it had just been a bunch of reasonable senior people (Board, management, Treasury, Minister) having a purely professionally-conducted disagreement and one deciding it was time for him to go.

But, as I’ve noted in a number of posts, having finally got that disclosure, more than three months after the resignation, there are still lots of unanswered questions (some for Quigley, some for the Board as a whole, and some for Willis, the people who continue in office). It would, of course, be great if Orr himself would give a substantive interview to a serious but searching journalist, but he is now just a private citizen.

This post attempts to bring the outstanding questions together in a list.

Questions for the Minister of Finance

- Did you really never ask (Rennie, Quigley, or indeed Orr) why Orr was planning to resign?

- Did neither officials nor the Board chair nor Orr (eg in his resignation letter, which had to be submitted to you to be effective) ever tell you why the Governor of the Reserve Bank was resigning?

- Did you ever make it known, directly or indirectly, that you did not wish to know?

- Were you aware that an exit agreement (going beyond resignation terms in Orr’s contract) was being negotiated? When?

- If not, why not? If so, did you ever make representations regarding possible severance payments and/or non-disclosure agreements?

- What was the atmosphere of the meeting held between you and Orr/Quigley and others (including Treasury officials and Hawkesby) on 24 February? Was the Governor’s conduct wholly and entirely professional?

- What representations and comments did you make on the Reserve Bank’s proposed 2024/25 Budget as part of their required consultation with you on the draft Statement of Performance Expectations?

- If those comments did not push back very strongly on planned levels of operating spending that went well beyond (around 23 per cent in excess of) what was permitted under the then-current Funding Agreement, why not?

- What was Treasury’s stance on that proposed budget?

- When did you first indicate to Treasury and/or the Bank (management or Board) that their initial bid for the new Funding Agreement (for $981 million in opex over five years) was unacceptable?

- Why were levels of Reserve Bank operating spending far in excess of (say) what the previous Funding Agreement had allowed for 24/25 included in the HYEFU numbers in December last year (reflecting fiscal policy decisions you had made up to 28 November). (NB: The previous Funding Agreement allowed around $154 million of (in scope) spending in 2024/25, while HYEFU appears to allowed $181 million per annum for each of 25/26, 26/27, and 27/28.]

Questions for Neil Quigley, Board chair

- Why did you approve a Bank budget for 24/25 involving levels of operating spending far in excess of what was allowed under the then-current Funding Agreement? Had any comments from Treasury or the Minister’s office raised any material concerns before the final Board decision was made?

- Why was it that as late as your email on Friday afternoon 14 February you seemed to believe that an agreement with Treasury on funding agreement matters could be sealed the following week?

- What stance had the Board taken on these matters at its meeting earlier that day?

- When did Treasury or the Minister first make it clear to you (or the Board generally) that the level of funding the Bank was still seeking by early February ($900m over five years, per Orr’s 5 February email) was quite unacceptable?

- Was there any communication from the Minister (or her office) to you after the 24 February meeting raising concerns about the Governor’s behaviour etc?

- When did you first learn that the Governor was seriously considering resigning? Was it at or after the 27 February Board meeting?

- Why was a negotiated exit agreement (covering anything more than, say, waiving notice requirements) considered necessary or appropriate (given that standard resignation provisions were presumably already part of the Governor’s contract)?

- Why did the terms of that agreement include paid “special leave” to 31 March rather than a resignation effective immediately (ie from 5 March)?

- Was there any discussion with the Minister, her office, or with Treasury regarding the possible terms of such an exit agreement. Did any of them raise concerns about gagging orders (whether binding on the Bank or on Orr?)

- What, if anything, are the terms of any gagging restrictions still in place? Given the extensive comments you have made, it seems the Bank may not be subject to material constraints? Is Orr, and if so why, and what consideration was given in exchange for him agreeing to such a term?

- Why did you say (per statement in the released pack) on the afternoon of 5 March (but independently of your press conference) “Adrian’s decision to resign as RBNZ Governor was a personal decision. He has conveyed that with consumer price inflation back within its target band, the time was right for him to step down.” Relative to the option (always open) of saying nothing, wasn’t this aggressively and deliberately misleading? How does that square with the Bank’s values around transparency and accountability?

- Why did you choose to hold a press conference at 5pm on 5 March? There is no suggestion of one in the pre-event planning. Was holding such a conference consistent with your agreement with Orr?

- Why did it take the Bank (for which, as chair you are responsible) more than three months to make the public statement that you did last week? Even if one granted some sensitivity around the Funding Agreement negotiations, the final Funding Agreement was released in mid-April?

- Did you and/or the Board approve what was released last week, including the text of the Summary Statement?

- What steps has the Board now taken to ensure that the Bank complies with its legal obligations under the Official Information Act, including in respect of requests on this broad issue (Orr resignation) that have been outstanding for months are were not addressed at all in last week’s release)?

- Why does last week’s release disclose nothing about dealings between you/the Board and either the Minister or Treasury in and around Orr’s release?

- Why does last week’s release disclose nothing about the Board’s own deliberations on these matters and/or their engagement with Orr once he made clear he was considering resigning?

Questions for the Board as a whole

- Why did you approve a budget for the Bank for 24/25 that was so far in excess of the level of spending authorised under the then-current Funding Agreement?

- Why did you agree to make a Funding Agreement bid that involved a large increase in future operating spending relative to levels authorised in the previous Agreement, despite being well aware of the prevailing climate of fiscal stringency. What sort of pushback did you provide to management, and did you insist on stress-testing the various options (including likely ministerial reaction to such a bid)?

- When were you first collectively made aware that the Governor was considering resigning, and what (if any) reasons were you given. What was the Board’s reaction?

- Why did the board agree to negotiating an exit agreement beyond the standard resignation provisions in the Governor’s contract. Did you approve the terms or was everything delegated to the chair? If the latter, given the sensitivity of such issues, why?

- Do you still have confidence in the chair after his handling of the public side of this issue, both on 5 March and since?

Questions for the temporary Governor

- Did you ever push back against either the 24/25 Budget, approved by the Board last June, or against the appropriateness of using such a vastly inflated level of spending as the starting point for the Funding Agreement bid?

- Who decided, and when, that Adrian Orr would not open or attend the inflation targeting conference (noting both his email at lunchtime on 5 March and comments later that day from the Board chair suggesting it still wasn’t clear)?

- Why did it take three months for any sort of statement (other than the highly misleading ones made to public and staff on 5/6 March) to be made on Orr’s resignation?

- What steps have been taken to ensure that the Bank meets its obligation under the Official Information Act, including actually addressing the specific requests lodged on this subject some months ago?

Questions for Treasury?

- What comments, if any, did you make on the proposed Bank budget for 24/25? What advice did you give to the Minister on this?

- When did you first make clear to the Bank’s Board that the initial Funding Agreement bid was quite unacceptable? Why weren’t they sent away early to revise and resubmit?

- Why were such spending numbers (well above previous Funding Agreement) included in the HYEFU fiscal numbers?

- Were you aware that an exit agreement was being negotiated with Orr? If so, did you make any representations on severance payments and/or gagging restrictions (if so, what?)?

UPDATE:

As it happens, I received a response to my OIA to The Treasury on (some of) these matters this afternoon.

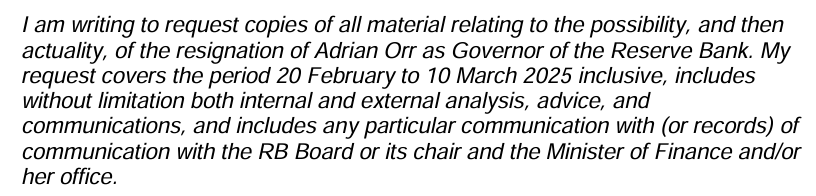

The request was as follows

There is very little there. Here is the full response, including a note of one document (only) withheld completely, with even the title kept secret.

Treasury response to OIA re Orr departure 16 June 2025

I think the only positive things we learn from this is

- Rennie’s initial advice to Willis on the afternoon of 27 Feb (the day of the crucial RB Board meeting) apparently reporting initial advice from Neil Quigley is very short (2.5 lines of a text) and not enough for more than a “Thank you for the heads up” from the Minister in reply. It seems to have been followed up with fuller conversation (Rennie/Quigley) that evening, which seems to conclude with the suggestion of a meeting or phone call (Willis/Quigley?) presumably the next day.

- On the Friday 28th, Quigley texts Rennie to ask him to call, saying he has an update. It seems likely this was the point where Orr had decided to go. Other papers reveal the exit agreement between Quigley and Orr was reached by Monday afternoon (3rd).

But what surprises me is what isn’t there. Faced with the likely, and then certain, resignation of the Governor of the Reserve Bank, an agency Treasury is responsible for monitoring and where the Secretary sits as a non-voting MPC member, there is nothing else at all written down, either before the announcement, on the day, or in the few days following.

Questions about the Funding Agreement, HYEFU, and last year’s RB budget were, of course, not covered by this request.