Various media this morning have given quite a lot of coverage to the new paper released by the NZ Initiative, headed How Central Bank Mistakes After 2019 Led to Inflation. The authors are Bryce Wilkinson of the Initiative and former Reserve Bank Governor (2012-17) Graeme Wheeler – the coverage probably mostly because of the trenchant words from the former Governor, I think the first we have heard from him since he moved back to corporate board land in late 2017.

I’m not one of those who has any particular problem with former Governors and Deputy Governors commenting on what is going on with monetary policy. If it isn’t always common, well we have a fairly thin pool of commentators in New Zealand, and these are hardly ordinary times. The quality of the debate is only likely to be improved by hearing, and challenging/scrutinising, alternative perspectives. We can only hope that one day the Reserve Bank’s own Monetary Policy Committee will learn from that sort of example, instead of continuing to act as some impenetrable monolith, even faced with the inevitable huge uncertainties of macroeconomics and monetary policy. And if Graeme Wheeler was not, to put it mildly, known during his term as Governor for welcoming debate and dissent – internally or externally – I guess we can only say better late than never.

In some ways the Wilkinson/Wheeler collaboration is a curious one. They go back 45 years to when Wilkinson was Wheeler’s boss in the macro area of The Treasury, and have apparently been friends since. But whereas Bryce Wilkinson has long been sceptical of any sort of active monetary policy (I have various emails on file challenging me as to what evidence there is that central bank policy activism has accomplished anything much useful over the years), Wheeler chose to take on the job of central bank Governor under an entirely-standard policy target, put into sharper relief than previously with the addition that the Governor was to be required to focus explicitly on keeping future inflation close to the 2 per cent midpoint of the target range. And there was nothing very unusual or distinctive about the way monetary policy was run on his watch – conventional models, conventional judgements, and in many ways conventional errors. If there were distinctives, they were mostly that Wheeler proved more thin-skinned than your typical central bank Governor or Monetary Policy Committee members (the young or those with short memories may have forgotten Wheeler deploying his entire senior management group to attempt to silence criticisms from BNZ’s Stephen Toplis – several relevant posts here).

The (quite short) paper isn’t specifically focused on New Zealand and our central bank, and consistent with that the authors have secured a Foreword from Bill White, former deputy governor of the Bank of Canada, and then long-serving Chief Economist of the Bank for International Settlements, from which perch he irritated many with his warnings about system fragility in the years leading up to 2008. He is a really smart guy and what he writes is usually worth thinking about, and I’ve enjoyed various stimulating discussions/debates with him over the years. His views today, reflected in the Foreword, still stand out of the mainstream (rightly or wrongly). If he is keen on fiscal consolidation etc across the advanced world, he champions “significant tax increases, particularly on the wealthy”, and while suggesting this would be desirable but politically impossible then suggests that a heavy reliance on monetary policy may pose a threat to democracy itself. White appears to believe that we are on the cusp of a very substantial adjustment, as the public and private debt built-up over the last few decades is sorted out (“we must review carefully our judicial and administrative procedures to ensure the necessary debt restructuring, and there will be a lot of it, will be orderly rather than disorderly”. Perhaps, but it is a long way from debates about how monetary policy has been run in the last 2.5 years or so. (And, for what it is worth, New Zealand has low public debt, and (for ill) its housing debt remains underpinned by governments and councils that refuse to free up land use on the margins of our cities.)

But enough introductory discussion. What should we make of the substance of the note? There is 13 pages of it, but about half is itself scene-setting or largely descriptive stuff. There are bits I might quibble with, bits I strongly agree with (unexpectedly high core inflation is the responsibility of central banks and the results of mistake choices by them – given inflation targets that is close to being a tautology), five big charts. Oh, and this was good to see.

Wheeler and Wilkinson seem to think QE-type operations (including our LSAP) are more effective macroeconomically (for good and ill) than I reckon, but the sheer scale of the losses is a reminder that even if there are some potential benefits, those would need to be weighed against the potential downside risks.

But the heart of the note is in the six points under this introduction

The first is “Central banks became over-confident in their inflation targeting frameworks”.

Much of the discussion of this point could have been written 15 years ago, although even then if there was much to the story it wasn’t so in New Zealand. We grappled with needing interest rates higher than the rest of the world to keep inflation near target, as well as repeated political assaults on whether we had the right target or the right tools.

But the story of the decade prior to Covid, in New Zealand and most other advanced countries, was of central banks struggling to keep inflation UP to the respective targets. New Zealand went for a decade with core inflation never once getting up to the 2 per cent midpoint that Wheeler himself had signed up to target. Now, I think it is probably true that in 2020 and early 2021, many central banks and central bank observers were more focused on the previous decade and its (very real) downside surprises, and not perhaps alert enough to the possibility of (core) inflation rising sharply. But that seems to me to be an importantly different thing to what Wheeler and Wilkinson are arguing.

They end this discussion with this point

But for now I think the evidence is against them. With headline inflation as high as it is, what is striking is how low market-based measures of inflation expectations still are (around 2 per cent here and in the US). The Bank’s own survey of 2 year ahead expectations, at 3.3 per cent in May, is higher than it should be, but probably not disastrously so at this point (and I reckon there is a good chance that the next survey, just being finished now, will show slightly lower numbers). Central banks were slow to act last year, but for now evidence suggests some confidence that they have, and will, acted decisively to keep medium-term inflation in check.

I also reckon that Wheeler and Wilkinson don’t adequately grapple with complexities and uncertainties of the Covid shock. It doesn’t really excuse the slow unwind last year – as, for example, the unemployment rate was falling rapidly – but it certainly makes much more sense of the initial monetary policy easing in 2020. Wheeler faced nothing of the sort during this term.

I had to splutter when I read the second item in their list: “Central banks were over-confident in the models they use to base monetary policy decisions”. Several paragraphs follow making the widely-accepted point that it is hard to work out the size of the output gap at any particular time, or to know with confidence the neutral interest rate. All very true, but who is going to disagree with them on that?

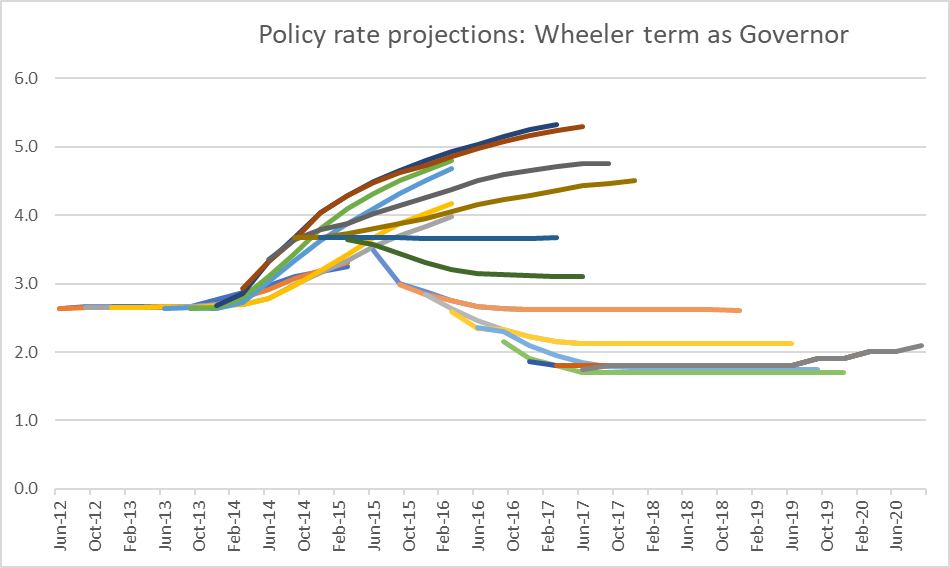

Well, one person who might was Governor Graeme Wheeler over the period from about 2013. He was convinced – quite convinced – that the OCR was a long way below its neutral level, and that large increases would be appropriate to get things back in check. So much so that in late 2013 he was openly asserting (in public) that 200 basis points of OCR increases were coming (any conditionality was very muted). These were the 90 day/OCR forecasts the Bank published while Wheeler was Governor

He was convinced that inflation pressure were building and rate rises would be required. Overconfidently, he started out on his tightening cycle in 2014, got 100 basis points in, and then finally was confronted with the data. The rate increases had to be reversed in pretty short order (and later in his term, the Bank was much more modest in its assertions). Note that although there were a number of central bankers globally who were keen on eventually getting policy rates higher, Wheeler was one of the few to back his model with ill-fated policy rate increases.

And to be fair to today’s central bankers, I haven’t detected an enormous amount of confidence in comments over the last couple of years, but rather (a) a huge amount of uncertainty, and then (b) some really big (but widely-shared) forecasting mistakes.

In the podcast interview that accompanies the research note, Wheeler does show some signs of (belatedly) accepting that he made a mistake. But even then he continues to claim it wasn’t really his fault, that the domestic economy really had been overheating, and that it was all the fault of the inscrutable foreigner (ok, he calls it “tradable inflation”, from the rest of the world.

Very little of this stacks up:

- core inflation (whether something like the sectoral core model that the Bank claimed to favour during the Wheeler years or the simple CPI ex food and fuel) was well below the midpoint of the target range throughout the Wheeler term.

- Wheeler claims that non-tradables inflation was high but (a) non-tradables inflation always runs higher than tradables, and (b) if one looks at core non-tradables inflation it was at a cyclical low when Wheeler took office, was not much higher when he left office, and was never high enough to be consistent with 2 per cent economywide core inflation, and

- Whatever the vagaries of output gap estimates, the unemployment rate lingered high (even at the end above most NAIRU estimates) throughout his term.

But read his press statement from early 2014 and you’ll see someone in the thrall of their model (at the time many people supported the broad direction of policy, but not all – whether outside or inside the Bank).

The third item on the Wheeler/Wilkinson list is “Central banks were excessively optimistic that they could successfully “fine tune” economic activity”. This is a longstanding Wilkinson theme, but is a curious one for Wheeler to have signed up to, given that he signed up to a tighter inflation target (focus on the midpoint) and after 2015 was more focused on getting inflation back up towards target. And, in fairness to our RB, their “least regrets” framework exploicitly recognises the huge amount of uncertainty that was abroad in the Covid era/

The fourth item is “Central banks took their eye of their core responsibilities and focused on issues that were much less central to their roles”. Of course, I agree with them that the Orr Reserve Bank has chased after all sorts of non-core hares (to the list WW provide one might add the “indigenous economies” central bank network), and I’ve been quite critical of that. But I just don’t think the case has compellingly been made that these fripperies really made that much difference to the conduct of policy. Take it all out and in the NZ context, Orr was still as he was, the MPC was weak and muzzled, and the Bank’s forecasts often weren’t that different from those in the private sector. Perhaps the (chosen) distractions made a substantive difference, but there needs to be a stronger case made than WW yet have (and central banks with much more talented Governors and MPC often seem to have made similar monetary policy mistakes to those of the RBNZ).

The fifth item in the list is “Dual mandates for monetary policy create conflicts”. In principle they can, in practice the case simply is not made as regards the last 12-18 months, when both inflation and employment limbs pointed the same way (here and abroad). Arguably they did so in 2020 too, at least on the forecasts/scenarios central banks, including our own, were working with. Forecasting was the biggest failure…….faced with a shock for which there was simply no modern precedent.

The final item on the list is “Did some central banks try too hard to support government political objectives in making judgements about monetary policy?”

The short answer is that WW offer no evidence whatever of anything of the sort, either in New Zealand or other advanced economies. They make this claim

which is probably true in some less developed countries, but do they have any examples in mind in advanced economies or New Zealand? I think not. In New Zealand, MPC members have been reappointed with no scrutiny, and politicians – government or Opposition – seem reluctant to focus on the central bank’s part on the inflation outcomes. There is no sign of any serious pressure on the Bank – not even much sign Grant Robertson cares much. Look at the underwhelming crew he just appointed to the Reserve Bank board – not evidently partisan, just deeply inadequate to the task (including holding the Bank and MPC to account).

And that is it.

In the end there simply isn’t a great deal there. It is good to have more voices sheeting home responsibility for high core inflation to the central banks. If you accept the assignment of responsibility for achieving an objective, you are responsible when things fall short (even if, as Wheeler argues was true of his own stewardship) you’ve done the best job possible with the information to hand at the time. How much that sort of explanation is sufficient to the current situation can and should be debated, but it probably needs much more engagement with data, and forecasts etc, than WW have room for in their piece.

Wheeler and Wilkinson end this way

I largely agree (although would put much more weight on top notch macro and monetary policy expertise, relative to financial markets). But what is noticeable throughout the paper is how little weight they appear to put on transparency or accountability. There is no call for diverse views and perspectives on the MPC, openly testing alternative perspectives, and individually accountable. But I guess – given his onw track record re dissent – such a suggestion would be too much for Graeme Wheeler even now five years safely out of office. It might after all have required more openness to stringent criticisms from people with a view different than the Governor’s

Incidentally I am pleased to see that his attitude to external scrutiny and challenge from former central bankers has moved on a little from his approach just a few years back when he claimed to believe that former staff – surely even more former Governors – owed some vow of omerta to the Bank and its mistakes, whether operational or policy.

Michael

It’s hard to take Wheeler seriously given his own shortcomings as the Governor and his then attitude to debate. Its also rather easy to say now that applying the GFC medicine was a poor response to the covid crisis. Central banking has got messier since his time. I’m more interested in your views on the following.

1. RBNZ as fiscal facilitator. I recall Don Brash and various Ministers of Finance clashing because Don saw the then fiscal policies as detrimental to his monetary policy goals. The 2020 recasting of the RBNZ’s role as “fiscal facilitator” so that Government had funds to support employment and business was a major turn around from those earlier days. As it has turned out, it was clearly based on several errors, not least being thinking that inflation was quiescent. But what do you feel RBNZ should have done in 2020? No QE? More limited QE? Faster withdrawal of the liquidity?

2. One target too many. RBNZ now has a plethora of targets as opposed to just “price stability” and presumably the 2020 QE was a fit with one of those targets. One target RBNZ seems to have endorsed (along with other central banks), without any specific commitment, is emission reduction. However, a significant causal factor behind high energy prices is under investment in coal/gas/oil production, which is being driven by institutional antagonism to such investment. “Employment Vs Price Stability” seems to allow quite a bit of wriggle room. “Restricting Energy Investment Vs Price Stability” is a pretty clear trade off, recognising that Government has embraced the former goal and is paying the inflation price. How would you recast RBNZ’s policy targets ?

Tim

LikeLiked by 1 person

Tim

I think any shift re “fiscal facilitator” was more rhetorical than real. The Crown never had any difficulty borrowing directly from the market, and except perhaps for a week or so in late March 2020 there was never really any doubt about it. So the LSAP was really pure monetary policy once we got past the disruption of the first week (and to Orr’s credit, he now defends it that way too). My view is that (a) perhaps some limited bond market intervention was warranted in late Mar 2020 for purely “settling the market” reasons, (b) beyond that there was not a good case for any extensive LSAP programme, including notably because long-term bond rates just do not matter v much here, compared to say the situation in the US where much of the mortgage market keys off them, (c) having started an extensive LSAP programme they should have called a halt by say Aug 2020 when it was evident that world was not imploding (and Tsy/Robertson should have refused to extent the indemnity), and (d) at absolute worst they should have stopped purchases by the end of 2020 and then announced a steady programme to sell the bonds back to the market over the folllowing couple of years,

On your second question, I don’t have a particular problem with the way the Remit target is expressed now, although I have argued previously (in my submission on the new law) that “lowest unemployment rate consistent with keeping inflation in the target range over the medium term” prob gets better at what we should look to mon pol to do (“run demand as hot as possible, subject to the absolute constraint that inflation is kept in check”). Having said that, I don’t think the precise wording (within that inflation/employment/output space) matters hugely, and much more will depend on (a) the shocks that come along and (b) the people who run the MPC. The Bank shld stay clear of climate change, esp as regard ,mon pol (and interestingly Adrian’s vstatement this afternoon comes close to agreeing). There will be all sorts of price shocks – whether from climate policy or whatever – but the Bank’s focus should be on the medium-term outlook, inflation expectations etc (as it was supposed to be over the last decade when say tobacco taxes were “artificially” boosting the CPI every year).

LikeLiked by 1 person

Reblogged this on Utopia, you are standing in it!.

LikeLike

[…] Michael Reddel, the goto person on NZ economy, rebuts the paper point by point. […]

LikeLike

Reserve Banks globally seem to believe their models without asking the question – how will Joe Public respond to the stimulus. Human reaction to stimulus has been very consistent over the centuries allowing for the nature and perception. At present the increasing rate of interest increases impacts payments and decreases disposable income as does the cost of tradeable & non tradeable essentials – Food/Fuel/Energy etc so it is not surprising that reaction is reduced spending, forced through lack of disposable income, or fear of future shocks – unemployment/recession/inflation so it will be no surprise if we end up in a recession and not a depression as history may well be repeating itself.

LikeLike

Still think that Orr could’ve shown a bit of restraint with his various loosening prongs. He seemed to ramp up right at the wrong time. Just my thoughts, thanks for the article.

LikeLike

I’m still convinced the LSAP achieved nothing useful, should not have been deployed, and had cost taxpayers $8bn+ to date , so am certainly not an Orr defender. But the specific critique by Wheeler and Wilkinson just wasn’t v persuasive.

LikeLiked by 1 person

Totally agree on LSAP. A “follower of fashion” stunt which I hope will be regretted.

Big puzzle for me is the theory and practice of “least regrets”. I haven’t read every word the Bank has written, but I do remember a piece by Christian which involved some dubious characterisations of some of our birdlife. Might have benefited from some Forest and Bird editing.

But nowhere have I seen how “regrets” are actually evaluated. To me the least regret is the one which has (under the current remit) inflation reverting to 2%. Are they putting other stuff into “regrets”? If so what, and what values are they assigning to them? Any trading-off needs to be very transparent.

Or is this armchair pipe-smoking central banking, without evaluation? “Trust us”

And is “least regrets” in any way supported by the theoreticians as a model for optimal decisionmaking under uncertainty?

LikeLiked by 1 person

I agree it was all rather vague, but given that they’d had 10 years of inflation below target midpoint I wasn’t too bothered about the idea that core inflation might go a bit above 2% for a while. Of course, 2%+ is not 5%, which is where we have ended up.

LikeLike

Would be interesting to be forensic about whether the failure to change course 18 months or so ago (when some of us could clearly see the need) was due to forecasting failure or decisionmaking failure

And we still have very negative real after tax interest rates….the kotuku is still asleep…

LikeLiked by 1 person

Of course if we focus on some or other measure of core inflation, retail mortgage rates are now modestly positive in real terms.

Stepping thru thru published forecasts it is pretty clear that until mid last year thr failure was almost entirely forecasting failure. The emphasis shifts from there.

LikeLike

When I see Wheeler whining about Orr I can’t help but think about stones and glass houses.

Wheeler unnecessarily held monetary policy too tight, pushing the NZD up to nearly 90c, pushing inflation persistently below target, and consigning a good number of people to the dole. The introduction of the dual mandate was a direct consequence of his intransigence and as for his willingness to entertain ANY criticism or critique…

And that criticism goes for one or two others at the Bank at the same time.

Also, its easy to throw stones at the Bank now, but I dont recall any constructive comment coming from either of these gentlemen during the COVID shock.

LikeLike

Largely agree re Graeme,but Bryce has published various pieces on mon pol throughout the Covid period (several of which I’ve written about here).

LikeLiked by 1 person