A slightly strange story – but one that rings very true – leads the business section of this morning’s Dominion-Post. In the story, Hamish Rutherford reports on an interview with the Reserve Bank’s long-serving chief economist John McDermott. If the interview is at all accurately reported, McDermott appears to have got himself into one of his periodic grumps with the private market economists.

I worked closely with McDermott for six years – he was my boss, and we sat directly opposite each other. He is mostly a pretty amiable guy, and in an earlier phase of his career had published a lot of research (a few years ago he was still, apparently, one of the New Zealand economists most cited in formal economics literature). But he doesn’t react that well to people disagreeing with him, especially openly (some of my other concerns were outlined in this earlier post on one of his 2017 speeches). There is often a testiness about his reactions – combined with a condescending tone of a “you just don’t understand” type.

And yet, of course, together with his colleagues he has been consistently wrong about the inflation outlook (and, thus, monetary policy) for at least the last five years. (In fairness, of course, except during the Bank’s very grudging series of OCR cuts in 2015/16, the median market economist has generally been even more wrong.)

But what of the latest interview?

A top Reserve Bank official has dismissed criticism from bank economists about his forecasts as “nonsense” saying the bank is ready to cut interest rates if growth lags.

On Thursday both Westpac and ASB accused the Reserve Bank of being too optimistic in its forecasts for economic growth.

But Dr John McDermott, the Reserve Bank’s chief economist for the past decade said the bank economists appeared to misunderstand the process creating Reserve Bank’s forecasts.

“Nonsense” is strong language. And both the Westpac and ASB chief economists previously worked in the forecasting part of the Reserve Bank, albeit a few years ago now.

Here is Westpac

However, we still think the RBNZ is expecting too much of the New Zealand economy. In our view, the recent plunge in business confidence portends a slowdown in business investment that the RBNZ has not allowed for. Furthermore, we expect the Government’s upcoming changes to the tax treatment of investment housing, the foreign buyer ban, gradually rising fixed mortgage rates and lower net migration will slow the housing market later this year. A slow housing market would, in turn, lead to slower consumer spending than the RBNZ anticipates. Finally, we doubt that construction activity will accelerate in 2019 to the extent that the RBNZ expects, even with the KiwiBuild scheme in operation. Capacity constraints in the construction industry are just too binding.

Agree or not, they sound like plausible points on which reasonable economists might disagree, without resorting to name-calling.

But – as he has often done in the past when his forecasts have been called into question – McDermott falls back on a claim of being misunderstood.

Rather than predicting what the economy will do, the bank worked out what kind of growth was needed to generate sufficient inflation. The variable in the equation is interest rates, which the bank can change.

In an interview in the Reserve Bank’s headquarters in Wellington, McDermott, repeatedly said if the economy was not growing fast enough to generate inflation, the bank will cut the official cash rate.

“It’s not about being optimistic or hopeful, it’s actually, if we don’t get that growth rate, we are going to lower interest rates because otherwise we won’t get the inflation rate.”

McDermott just shouldn’t be allowed to get away with this sort of special pleading (even setting aside the fact that he and his bosses have actually delivered core inflation well below the target midpoint for years now). He makes a partially fair point that one can’t just look at the Bank’s GDP forecasts in isolation. But that is true of anyone’s forecasts. While it is inflation targeting, the Reserve Bank will always show inflation coming back – more or less slowly – towards the target midpoint. And so, at very least, one has to read the interest rate and GDP forecasts together.

But in Westpac’s case they think GDP growth will be lower than the Bank is projecting, and that interest rates will be a (very) little lower than the Bank is projecting. Against that backdrop it seems quite reasonable for them to say that the Bank is being too optimistic about how much GDP growth is likely over the next couple of years with interest rates around where they are now, or even a bit lower.

McDermott goes on

“Our inflation forecasts are always 2 per cent, it’s always 2 per cent. [eventually]

“It is because we plan to succeed, and then you go, ‘well, how do you do this’. And so, the monetary policy statement’s objective isn’t an unadulterated forecast about what we think will happen, it’s what do we need the plan to look like to make it happen.”

The problem with McDermott’s story is that his forecasts today influence policy today. Thus it is fine to talk – as McDermott often does – about revising forecasts in light of developments. But better still, how about getting them (more) right first time round? The Bank believes that it will, with current interest rates, generate more demand and economic activity – and thus more inflation – than some of the private economists (eg Westpac and ASB) think likely. The Bank is in that sense more “optimistic” than these private economists. If the Bank is wrong, we will eventually find out, and (slowly, grudgingly) policy will be adjusted, but in the meantime we’ll have missed out on some growth (they expected) and inflation will have fallen short of the target (again). If they are indeed too “optimistic” now, it matters.

McDermott goes on

McDermott said many bank economists did not appear to understand the process.

“They sit outside, they don’t get to influence policy. We get to move [interest rates]. Inflation has to be 2 per cent, and engineer backwards, what do you need growth to be, to engineer 2 per cent [inflation].”

So if growth starts lagging, you’re going to cut the OCR?

“Yes. That’s the game,” McDermott said. “So the fact that they think we’re being optimistic is a nonsense, because if it doesn’t eventuate, we get to alter interest rates.”

It is exceedingly unlikely that bank economists did not “understand the process”. The process has been operating in basically the same way for more than 20 years now, it is extensively documented by the Bank in published material, and three of four main banks now have chief economists who started their careers in the Reserve Bank Economics Department. What is going on here is that the Reserve Bank chief economist is on the defensive, and rather than defend the substance of his forecasts he attempts to muddy the waters with suggestions that the private economists just don’t understand.

Thus, we are told, McDermott

would “remind” several chief economists of the process used

Which won’t change the fact that there is a difference of forecasts – of views.

In a way, he even concedes the point. The final sentence of the hard copy version of the article isn’t in quotation marks but here is what McDermott is reported as saying

McDermott said it would be a different situation if the banks were saying that the forecasts were too optimistic based on the OCR remaining at the current level.

So what was all the name-calling about? As McDermott knows, neither Westpac nor ASB is forecasting an OCR cut, and the Reserve Bank isn’t forecasting an interest rate increase for some time. The private economists and the Reserve Bank all have the OCR at 1.75 per cent throughout this year and well into next year, and thus their GDP forecasts for the next year or two are apples-for-apples comparisons. It is quite reasonable to say that Westpac and ASB think that Reserve Bank is too “optimistic” (and they don’t need to state all their ancillary – but rather obvious – assumptions every time they make the point).

The article also contains this observation and comment

While economists have slowly come around to the Reserve Bank’s view that the OCR will stay at its current low for at least a year, none give a significant chance that the Reserve Bank will cut.

McDermott suggested they were wrong to do so.

“The market thinks ‘you guys are never gonna [cut]. They’ve been through almost a whole year of ‘there’ll be no chance you guys are going to cut interest rates’. Well, that’s not true.”

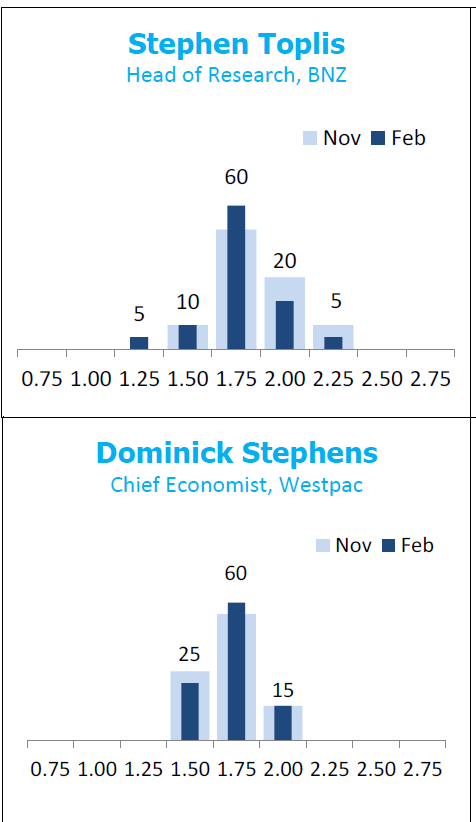

But again, this looks like a deliberate attempt to skew interpretations. The Bank – rightly in my view – has talked of the possibility of cutting the OCR, but in all its comments last week – including from the “acting Governor” – it came across as very reluctant. And its published OCR forecasts don’t have a flat track as far as eye can see – in fact the track starts edging upwards from the middle of next year. And what of the market economists? A couple of the more prominent ones are included in the NZIER Shadow Board exercise. Here were their latest probability distributions for where they think the OCR should be.

The chief economist of Westpac a few days ago thought there was 25 per cent chance that the OCR should have been lowered. Indeed, in their post OCR commentary, Westpac explicitly said

If anything, we would put the odds of an OCR reduction this year as slightly higher than the odds of a hike

(Perhaps if the Reserve Bank really wants people to stop focusing on possible OCR increases they should, at last, drop the endless rhetoric about a “normalisation” of interest rates?)

I’m also a bit sceptical of the Reserve Bank’s growth projections. As I’ve been pointing out for some time, in each set of quarterly forecasts they project a return to productivity growth. In the latest numbers, after four years of basically zero growth in their “trend labour productivity” measure, they forecast a steady pick-up in productivity growth such that by 2020/21 they expect 1.2 per cent annual productivity growth. In a single year, they expect as much productivity growth as the total productivity growth they show for the six years to March 2019. Without any material productivity-enhancing micro reforms, and without any substantial reduction in the exchange rate, if that isn’t “optimistic” I’m not sure what is. I really hope they are right, but it looks too optimistic at present.

No doubt the private bank economists will just grumble quietly, and their view of McDermott will be adjusted another notch downwards. After all, they’ve seen what happens to those of their number who too openly criticise the Reserve Bank – recall that McDermott was one of those deployed by Graeme Wheeler last year in his heavyhanded attempts to silence BNZ chief economist Stephen Toplis.

But we – the New Zealand public – deserve better. We need a reformed Reserve Bank, a properly independent statutory monetary policy committee, not simply staffed with bureaucrats, and we need quality senior staff of the Reserve Bank who are capable of engaging openly, and authoritatively, on the sort of issues and uncertainties we face in making sense of the economy, without resort to name-calling or rather desperate attempts to suggest that people who disagree with the Bank just don’t understand, and that they need to be called in and “reminded” of the process.

There is certainly a process that the RBNZ is not clarifying and that includes variables like macroprudential tools and interest rate competition with bank licensing and its effect on interest rates. Effective from January 2018 the RBNZ lowered the equity restrictions on LVR from 40% to 35%. They have not clarified what impact that actually has on inflation. Also the recent changes to the banking license rules allowing China Construction Bank to leverage local lending against its Group parent trillion dollar balance sheet and whether than loosening would apply to the other Chinese banks currently operating as embarrassing tiny banks against our giant Australian monopoly banks. It is clear that they have these 2 significant changes that will affect credit liquidity and its availability to the local NZ economy which will impact on NZ GDP in the longer term. It is probably this loosening in macroprudential tools ie easing the 40% equity to 35% and perhaps 30% and increasedinterest rate competition in relaxing the banking license caveats that the RBNZ intends to use to boost economic activity rather than to drop the OCR further.

LikeLike

Reblogged this on The Inquiring Mind and commented:

Most useful commentary. Pleased you chose to comment, as I was hoping you would.

LikeLike

I would have thought the last 10 years reflect pretty badly on whoever is overseeing the economic modelling effort. If you are running a hedge fund and there is a paradigm shift, you need to try and come up with an algorithm that fits the new world.

LikeLike

[…] in the week I wrote about Reserve Bank chief economist John McDermott’s rather strange attempt to distract […]

LikeLike