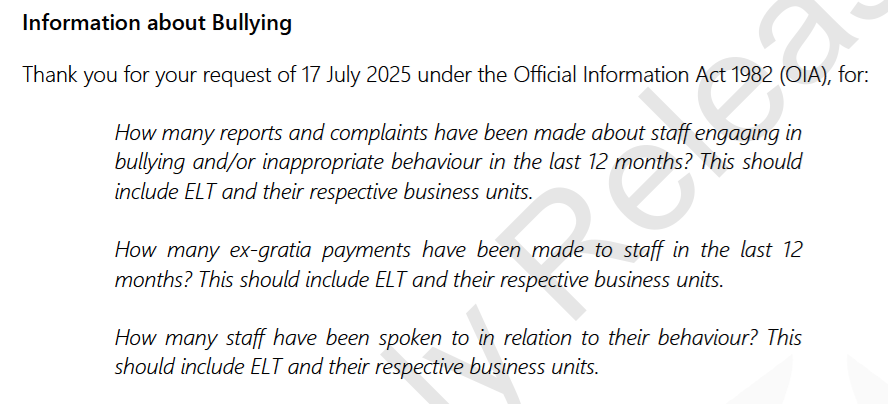

Various bits and pieces have emerged from the Reserve Bank in the last couple of days; two in the form of other people’s OIA requests, and one in a partial response from the Bank to one of mine lodged with Treasury.

First, bullying. Someone, who must have had some knowledge of what was going on, had lodged a request for this information

Perhaps the Bank is turning over a new leaf on OIAs, as the request had only been lodged on 17 July and not only did the response go back to the requester on Monday (4 August) but they put it on their website that day (the Bank is quite selective about which responses they post, and there are often quite long lags). In fact, I just noticed there is another response – to a request lodged on 24 July – sent today and posted on the website today. If this really is a change of heart it is excellent news.

Anyway, the answers were interesting, to say the least

In the words of one former colleague, those payouts were “startling”. The 20 staff being spoken to seems a lot too, but who knows quite what standard they were using. Perhaps someone had spoken disrespectfully of the tree god, or suggested that the Bank really should have stayed within its allowed Funding Agreement spending limits? But to actually write cheques, hand over money, things must have been quite serious, even in an organisation not recently known for its budgetary discipline.

We know nothing more at this stage (amounts, specific reasons, who was responsible for the behaviour for which the ex gratia payments were made). To be entirely literal it isn’t 100 per cent clear that all the payouts were for bullying (the request covers any ex gratia payments to staff), but they probably were, given that the Bank headlines the entire response “Information about Bullying” and would have had an incentive to minimise the bullying dimension if there really were other reasons for some of the payments. Were the payments made before or after Orr left, and were any of them on account of his behaviour? I gather from Twitter that someone has lodged a further OIA so perhaps we will learn a bit more in time. But it doesn’t look good – and cases rising to level of payout must only be the tip of an iceberg, as some people are likely to be reluctant to lodge complaints, and others may simply have left the organisation.

The second OIA was about the new Auckland office (also only lodged on 24 July). You may recall that my source had indicated that the Bank had signed up to a fancy new Auckland office of a size probably inconsistent with the looming budget cuts. The Bank’s response seems to broadly back that story. The new lease agreement was signed on 4 November 2024. By that time (and as far as we can tell at present) the Bank did not know that its approved spending levels would be cut a long way back from what they had bid for when they lodged their next five year Funding Agreement bid in September. However, they were well aware that they had gone out on a limb, adopting a budget for 24/25 that was 23 per cent in excess of what they were allowed by Grant Robertson for that year under the Funding Agreement then in place, and had sought to persuade the Minister and Treasury that any (modest) cuts should be only from that unauthorised high “baseline”.

And while they may have needed a new Auckland office, this was the new space

and this was what it was to replace

In other words, they committed to more than twice the floorspace, in a more up-market building, at a time of general fiscal stringency and when they had no particular reason to suppose that they’d be allowed to keep growing. I’m not a property person but it seems that 10-15 square metres per head is about normal for typical open plan office

So it looks as though the Bank had gone lavish on the per capita floor space even if the new office was to be fully occupied at some point in future (which would have been a lot larger scale than the 164 staff and contractors they had in the Auckland office as at 30 June).

It seems a lot like a cavalier use of public money, made even worse (than their general budget excess) by the no-doubt multi-year nature of the property lease. But perhaps they’ll be able to sublet some of it?

And that spilled over into the third OIA response, that turned up this afternoon. It was part of a request I’d lodged with Treasury a couple of months ago which they’d transferred (that part of) to the Bank, and covers some late-in-the-piece material from the Bank to and from the Minister on Funding Agreement matters, after Orr had left. To be honest, I didn’t even think this material was in scope, as I’d been looking for Treasury material. As it happens, when I read what came in, parts seemed familiar, and I realised they’d already released these particular documents to someone else a month or so ago and I’d used a couple of bits of it last month (end of that post). But I hadn’t looked that closely then, and the significance of other aspects is also more apparent now.

First, last Friday I highlighted the way the temporary Governor Christian Hawkesby appeared to have actively misled FEC on where the initiative lay for the review the Bank now has underway of bank capital requirements. He played down any ministerial involvement claiming it had been just a Bank decision to do the review. That it clearly wasn’t was pretty evident from the Treasury filenote of that 24 February meeting between the Bank, Treasury and the Minister.

But to reinforce the point, here is Neil Quigley writing to the Minister on 16 March basically pleading (successfully) that she not accept Treasury’s view of how deep the cuts to operating expenses should be. This was the paper in which he pleaded that the Bank’s “culture” had evolved in light of the fiscal excess of recent years and that it would take time to change the culture and save lots of money. But he also said this

Hawkesby actively misled FEC. Once upon a time that sort of thing mattered.

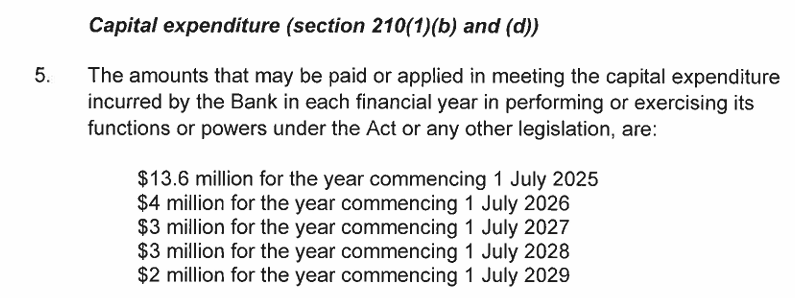

Where Quigley was largely unsuccessful at this stage was around the capital budget (not something I’d previously paid any attention to). The initial bid last September had been for $50 million over five years. At this point Treasury was proposing $26 million (which, assuming the numbers in the Minister’s Cabinet paper are comparable, was 12 per cent less than total expected capex for 2020-2025). Here was Quigley’s plea

Note that first item. If you’ve just rashly signed up to big new offices in a fancy building the fit out costs (for a lease that commenced on 1 August 2025) were likely to be large.

Quigley’s capex plea failed, and the Minister ended up agreeing to allow them only $26.3 million of capex over the full five year period. This is the annual phasing.

Which might suggest that they will be spending something close to $10 million on the fit-out of a new office that they simply shouldn’t have signed up to before they had any clear steer about the future. The 25/26 number ended up a bit higher even than the $13m Quigley had sought on 16 March – new estimates of fit out costs? – with the capex allowances for future years being slashed. (If Quigley’s plea is even roughly accurate you might wonder how sustainable all this proves – presumably the Bank will spend all its opex allowance, and perhaps they reckon they’ll come back cap in hand in a few years’ time, or degrade the existing capital and wait for the next Funding Agreement negotiations. Or Treasury might be right about what they need.)

The final observation from these papers is perhaps not of any great moment, but it is puzzling nonetheless. You’ll recall that the Bank had gone ahead and set a budget for 24/25 far in excess of what the Funding Agreement had allowed. There was never any serious suggestion that the Bank was allowed to carry forward earlier year underspends, use it all for a last year splurge, and then try to use that new level as a baseline against which any modest cuts should be set. But that is how Orr, Quigley and the rest of the board had operated (quite explicitly – it is in the Board minutes and the September 2024 Funding Agreement bid).

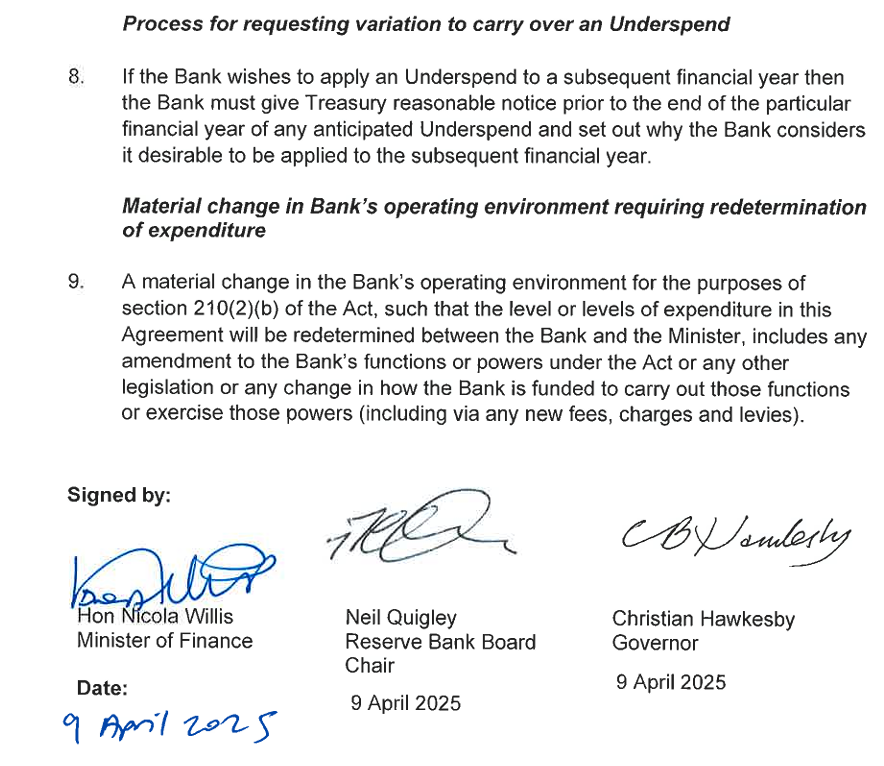

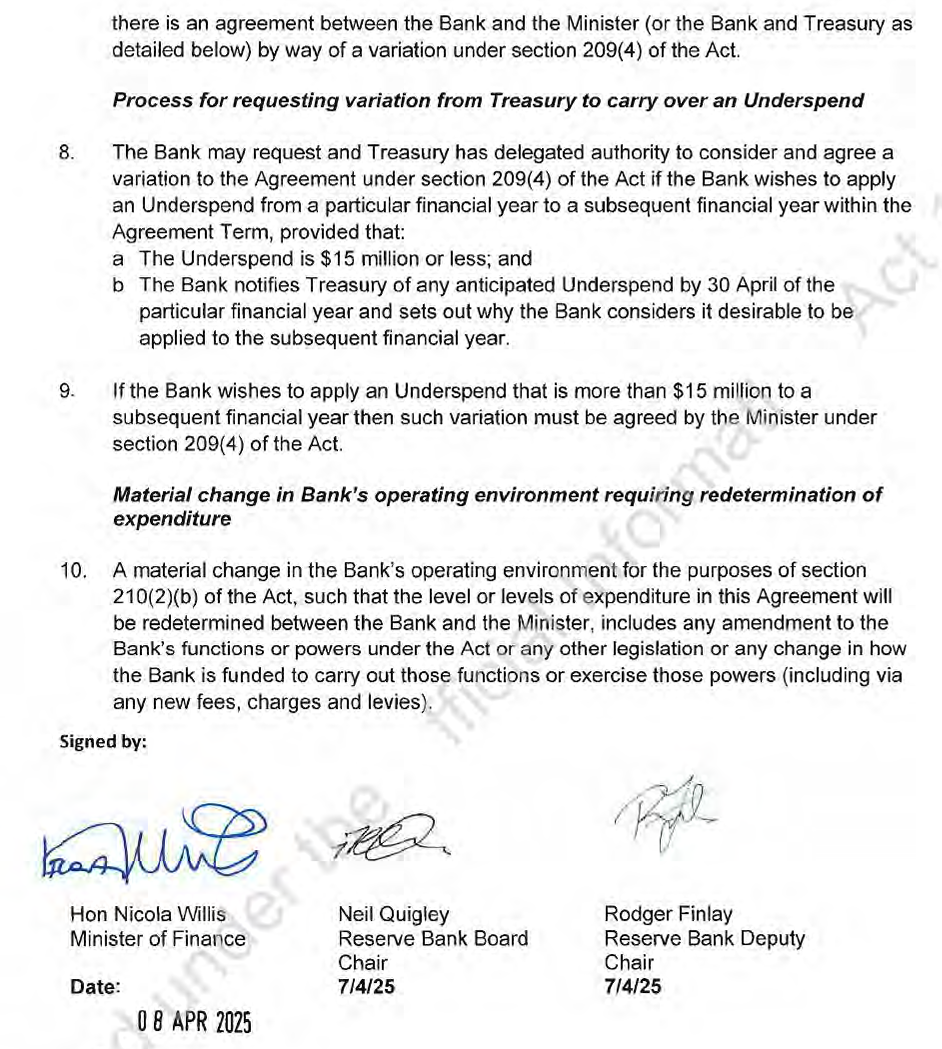

There are problems with the Funding Agreement model, which involves setting annual spending limits five years ahead. Sometimes it is hard to know when a particular cost might arise. So it probably does make sense – if this model is stuck to – to allow scope for some flexibility. It is there anyway – no one gets fired for going a bit under or over in any year (and isn’t formalised like a parliamentary appropriation), and there is always scope for a renegotiation mid-stream (as there’d been in 2023). But the Bank was keen to formalise something. I noted in a post last month that in that 16 March paper the version of the draft agreement the Bank submitted involved a model in which Treasury could agree to modest variations (up to about 10 per cent) and anything more required the Minister.

I’d noticed that the Minister must have said no to that as the final document on the Bank’s website provided only (and appropriately) for this

I included the signature block because what I hadn’t noticed before – hadn’t read to the end of the set of documents, which looked like they were just repetitions and admin paperwork – is that she seemed to agree to this only after she’d already signed up to something like what the Bank wanted.

In that OIA response there was this

All signed and dated and a scanned version sent back to Bank by one of the advisers in the Minister’s office, in a email of 10:14am on 8 April.

We are left wondering what happened. Quigley’s memo of 16 March did not touch on the variation issue at all. Was the Minister not made aware of it, including by Treasury, until the very last minute, or was she aware all along and very belatedly chose to take a harder line? Fortunately she did finally land on the best approach, but how? The original OIA to Treasury, lodged back in June but due shortly, may shed some light, but it just doesn’t look like a particularly smooth or adept end to the Funding Agreement process. And I wonder what Quigley, Finlay, and Hawkesby made of the latest, last, loss………..which couldn’t have happened to a more deserving bunch given their egregious bid six months earlier.

As for me, I guess I should read OIA responses – even other people’s – a bit more closely.