Four weeks ago I noted that I was going to be tied up for the following couple of weeks. Between a busy trip to Papua New Guinea, the extremely dubious governance of the Reserve Bank superannuation scheme, various family members coming to stay, and a health relapse all that turned into a rather longer break from the blog than I’d expected/intended. But in that time, several interesting responses to Official Information Act requests turned up.

My last post was 41 Questions, in reference to the many questions still unanswered by the Minister of Finance, the Reserve Bank board, Neil Quigley (the Board chair), the temporary Governor, and The Treasury about the events surrounding that sudden departure in early March of Adrian Orr as Governor of the Reserve Bank.

A few of those questions (around one particular set of events) have now been answered, and the answers leave everyone involved in a poor light. These were a few of the questions from that earlier post that I thought the Minister of Finance owed us answers on.

The short answer (developed in the rest of the post) is that the documents show that neither the Minister of Finance nor The Treasury raised any concerns at all about the Bank’s plans to substantially increase operating spending last year, to levels far above what was permitted in the (Labour government’s) Funding Agreement. It is really quite extraordinary.

But lets go back to the beginning.

As a reminder, the Reserve Bank operates under a Funding Agreement reached every few years with the Minister of Finance. Quite a few classes of spending are excluded from the Agreement, and there is no external limit on what the Bank spends on those items, but around 85 per cent of the operating expenses were within the scope of the agreement in place last year.

When the Reserve Bank’s Board was approving the budget for 2024/25 – around the time of the government’s first Budget, where much was made of expenditure restraints (and cuts) for most core government departments – the Reserve Bank was operating under a Funding Agreement for 2020-2025 agreed with Grant Robertson in 2020, with amendments (the most recent, providing for a large increase in operating spending for the final two years, signed off shortly before the 2023 election).

Under that amendment, the Minister and Bank agreed on how much the Bank could spend on (within scope) operating expenses in the year ending 30 June 2025.

This was a very marked increase from the $118.3 million originally provided for 2024/25 in the 2020 Agreement.

Both the agreement and the Act are quite clear that these are limits for the financial year concerned. The agreement is not structured to provide for (and the Act does not envisage) a five yearly total within which the annual numbers are merely indicative.

There are two caveats. First, the 2020 Agreement had provided a separate category for spending on direct currency issuance expenses (a sensible provision because you wouldn’t want the Reserve Bank stinting on a functioning currency system to pursue some other whims). For 2024/25, this allowance was $14.5 million. However, by 2023 it was apparent that the Bank was needing to spend a bit less than expected on currency issuance, and so the Minister had agreed that for 2023/24 and 2024/25 the Bank could utilise any underspend on this item for general (in-scope) operating expenses. The Bank thus had ministerial approval to spend up to about $154.4 million in 2024/25 on general (within-scope) operating expenses.

The second caveat was this (from the 2020 Agreement)

Budgeting five years in advance is hard (like the Bank – as disclosed in recent papers – I think the Funding Agreement approach is not really fit for purpose and should be replaced; useful as it was transitionally 35 years ago). This provision recognised that in any one year the Bank’s actual spending might go over the Funding Agreement limit. It put the onus on the Bank – and the Board after new law came into effect in 2022 – to offset any one year’s excess with savings in subsequent years.

The Board sets operating budgets for the Bank. You would expect that those budgets would be in line with the Funding Agreement amounts – and two Board members (the chair and the Governor) had signed that 2023 amendment – but there are no direct or immediate consequences if either budgets or actual spending aren’t in line with the Funding Agreement. That is one of the real weaknesses of the system.

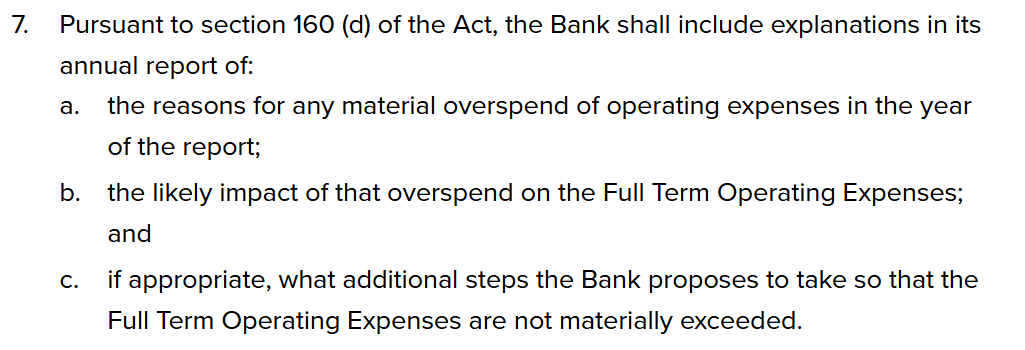

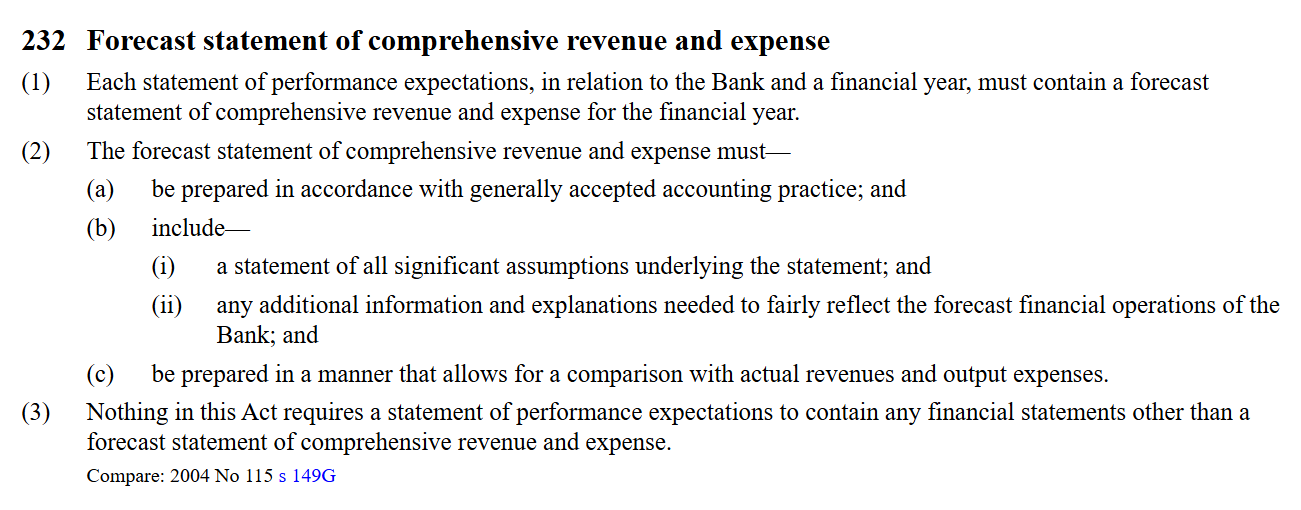

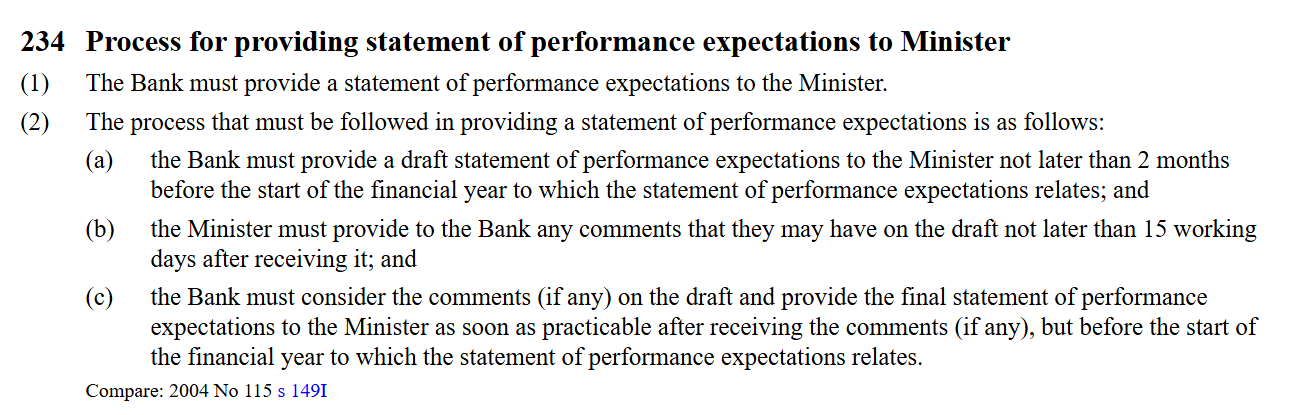

But, weak as the system is, we (the public) weren’t supposed to be left unprotected. After all, in the 2021 amendments to the Reserve Bank Act a stronger responsibility was assigned to Treasury to monitor the Reserve Bank and act as adviser to the Minister of Finance on things involving the Bank. And then there was the Minister herself. Flawed as a five-yearly Funding Agreement (with amendments) model might be, these days the Reserve Bank is required to produce a Statement of Performance Expectations each year. The relevant clause of the Act reads well.

and, yes, the financial dimension is included

and the draft needs to be with the Minister well before the finished document has to be finalised and published.

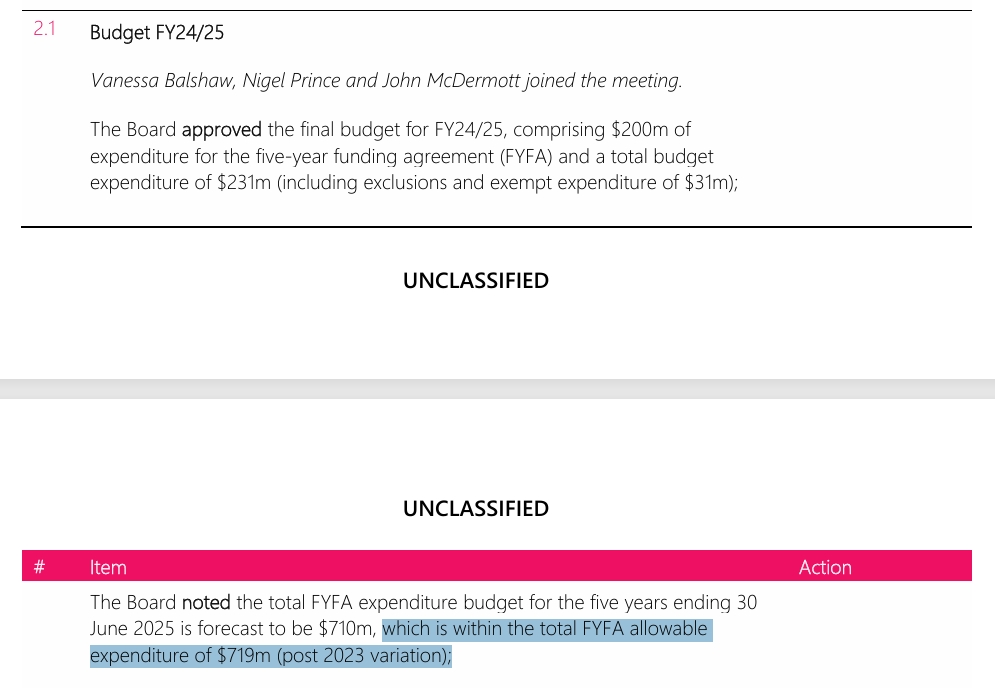

We know, from the final published Statement of Performance Expectations, that the Bank budgeted for total operating expenses in 2024/25 of $231 million. That was well up on the previous year’s budget (and on the biggest discretionary item – personnel expenses – the budgeted increase was 21 per cent, this in the first full year of a new government emphasising spending restraint).

The published Statement of Performance Expectations does not provide numbers that enable direct comparisons with the Funding Agreement limits (surely a weakness in the statutory provisions?) but material released subsequently show that of the $231 million, $200 million was on items covered by the Funding Agreement (around $9 million on currency expenses and around $191 million on the core within-scope operating expenses). Recall, that the 2023 Funding Agreement amendment allowed them to spend about $154.4 million on those core within-scope operating expenses in 2024/25. The final published budget was thus consistent with spending around 23 per cent in excess of what was provided for in the Funding Agreement.

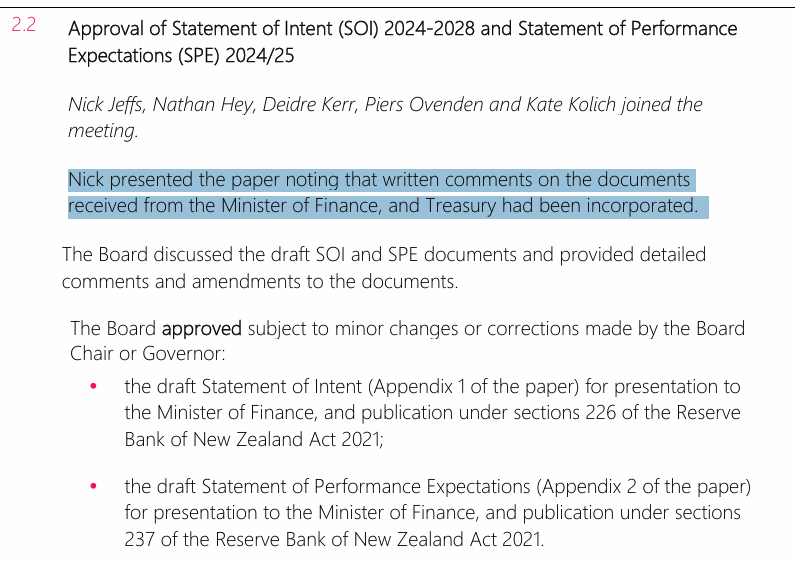

In recent years – since the Board became the primary governing body – the Bank has been published partial (and limited) minutes of meetings of the Board. We know from the June 2024 minutes that the Bank had received and incorporated comments on the draft Statement of Performance Expectations from the Minister of Finance and Treasury.

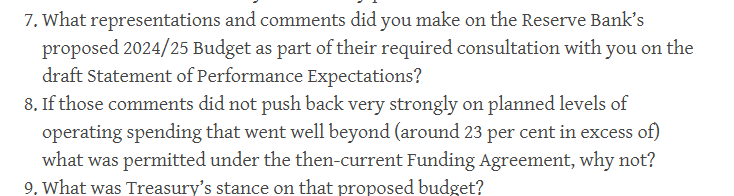

The mystery then was how such a huge blowout in operating spending had happened despite the input of the Minister and Treasury. So I asked the Bank for copies of those comments (as part of a request for several other items that, three months on, they have still not responded to). Their response was to tell me that the comments had actually been released in October last year, as part of a very long document for a standard Treasury pro-active release. The relevant pages are here as a standalone document.

These documents are Treasury advice to the Minister and a proposed letter from the Minister to the Board chair (which is, presumably, the version that was sent, since what I’d asked for was what the Bank received). There is simply nothing in the documents (even considering redactions) even mentioning the overall proposed level of spending, let alone highlighting the inconsistency with the Funding Agreement, or raising concerns. Nothing.

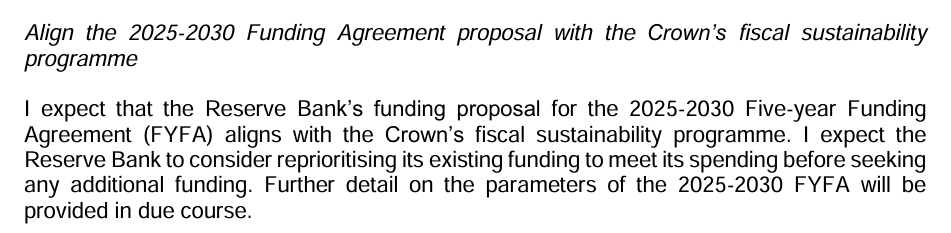

It is difficult to decide who is more culpable here, Treasury or the Minister. The Minister should be able to rely on hardnosed Treasury advice on such things. And, after all, Treasury had been involved in the previous Funding Agreement increase only nine months or so earlier, it had been fully involved in the spending cuts for agencies in the 2024 Budget, and had been involved the April 2024 Letter of Expectation sent by the Minister of Finance to the Bank’s board, which included this.

You’d think that a Treasury doing its job – in fact, a Treasury even half awake – would recognise that a big increase in spending in the last year of the old Funding Agreement, well in excess of what was allowed for that year in the Funding Agreement, was a glaring “red flag” and should be called out in no uncertain terms. Neither they nor the Minister had the power to override the Board and compel a lower budget, but they could have put a great deal of pressure on, including threatening to call out excess in public. Instead, it seems that they did nothing at all. Nothing.

At very least they might have made the point that consideration of the next Funding Agreement would start from a baseline of what had been allowed in the previous agreement and that it would be quite unacceptable for the Bank (as it went on to do) to bid for the next five years’ spending from a starting point so far in excess of what the Bank was allowed to spend in 2024/25.

And what of the Minister of Finance? If she is entitled to expect hard-nosed advice from The Treasury, highlighting all the relevant issues and risks, and giving her both recommendations and choices as to how she deals with the Bank, what on earth was she thinking herself, and what was going on with the political advisers in her office, who are there partly to protect her interests when bureaucrats aren’t doing their job? Willis, and (surely) her own advisers, had long been sceptical of Orr. They’d rightly highlighted in public some of the spending excesses undertaken by the Bank under Labour’s watch. Did it never occur to them to check what percentage change in operating spending the Bank was proposing, or to check how that spending compared to the Funding Agreement, or to line up the Bank’s plans with the spending limits Willis was imposing on most departments? If any of it ever occurred to them – and it would have been easy to go back to Treasury and get them to follow up – there is not the slightest sign of it.

It is quite an astonishing lapse (or choice) by a very senior minister, in a climate of (purported) fiscal restraint. And if the Reserve Bank isn’t the biggest spending agency (by far), the old mantra about looking after the pennies and the pounds will take care of themselves still has something going for it, including in inculcating in government entities a culture of frugal restraint. Willis let the mad Reserve Bank spending binge run on for a whole additional year, and in addition to the resulting sheer waste of taxpayer money, and the demonstrated capacity for the Bank to simply ignore (or twist) the Funding Agreement, the result was also lives badly disrupted. The Bank carried right on substantially increasing staff numbers in 2024/25, drawing people away from other jobs, only for many now to be losing their jobs (and if we needn’t sympathise even slightly with Orr’s senior managers now departed, think of the new graduates just starting out being laid off, and many others in between). Large scale restructurings are wrenching, dislocating, and hard on people innocently caught up in them at the best of times.

It is easy to blame Adrian Orr in all of this, and I’m sure he deserves his fair share. None of the excess would have occurred without him. But the Governor is not the governing body of the Reserve Bank any longer: the Board is. And who is supposed to act as monitors and checks on the board – when they let themselves be carried away by the ambitions of an over-mighty Governor, and thus simply fail to do their job? Why, that would The Treasury – premier economic advisers to the government – and the Minister of Finance, the person accountable to Parliament (and thus voters) for the Bank and both its policies and (in this case) its use or abuse of public resources.

I had wondered for a while how even a useless underqualified board, apparently in the Governor’s pocket, as the 2024 Reserve Bank board seems to have been, could have thought it appropriate or right to increase spending so much last year, so much in excess of the Funding Agreement limit. There isn’t an obvious or easy answer to that, but the Board minutes suggest they thought – and presumably were told by management – that it was all just fine. This is also from the June 2024 Board meeting minutes

Somehow, even though the Funding Agreement is very clear about annual limits, they talked themselves into believing that somehow any past underspends could be used for a final splurge in the last year. It is hard to believe that anyone of honesty and integrity could have reached a conclusion that that was either a) possible, or b) right. No doubt they would have been pointed to that extract from the 2020 agreement about what happens if the Bank overspent in any early year of Funding Agreement. But not only is there nothing in that section suggesting underspends could be saved up and spent later but (and importantly) a) spending for the first three years of the agreement was already water in the bridge by the time Grant Robertson reset approved spending levels in August 2023 for the last two years of the agreement (had he wanted them to spend even more in 23/24 and 24/25 presumably he’d have set the annual allowances even higher, b) did no one on the Board stop to think how disruptive it would be to massively increase spending and staff numbers in the final year, with no assurance that such artificially high spending levels and staff numbers would be approved for future years (it wasn’t as if the sharp increase was a specific one-off project), when c) the Minister – see letter of expectation – had already highlighted the need for fiscal restraint in approaching the new Funding Agreement negotiations.

We can only conclude that either the Board was asleep at the wheel (paying no attention no matter Orr was doing) or – more likely in my view, given the bid for the 2025/30 Funding Agreement that the Board approved a little later last year – Orr persuaded them to go along with some reckless double or quits strategy: spend up large now, get a bigger empire, and then hope we can persuade the Minister to reset the new baseline level of spending not off the previous Funding Agreement starting point, but from the (hugely in excess) Bank-determined level of planned spending for 2024/25. Either way, you wonder how they thought they were serving the public interest, or how they have had the gall to claim their fees.

Perhaps even more surprising then is that just a couple of weeks ago, the Minister of Finance – having reappointed Quigley last June for a final two year term as chair – reappointed yet another of the existing Board members, Byron Pepper, for a full five year term (while leaving another board vacancy unfilled). There is not the slightest evidence in any of the minutes that Pepper had ever (a) dissented on the reappointment of Orr, or b) dissented on the Funding Agreement blowing 2024/25 budget, or c) dissented on the 2025/30 Funding Agreement bid. And yet, such it seems is the New Zealand way, he is rolled over for a full five year term, and now chairs the Board’s Financial Stability Oversight Committee. You’d at least hope he’d be demanding evidence of better standards of governance from the institutions the Bank regulates/supervises that he displays in participating in the governance of the Reserve Bank.

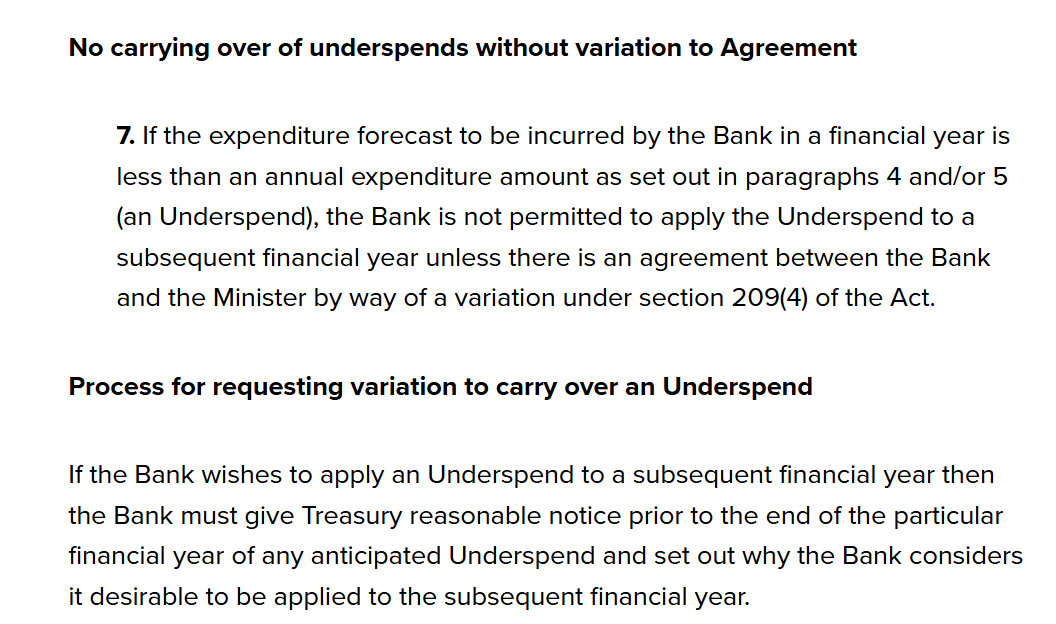

(As it happens, the “carry forward underspends” point is explicitly clarified in the new 2025-30 Funding Agreement which states

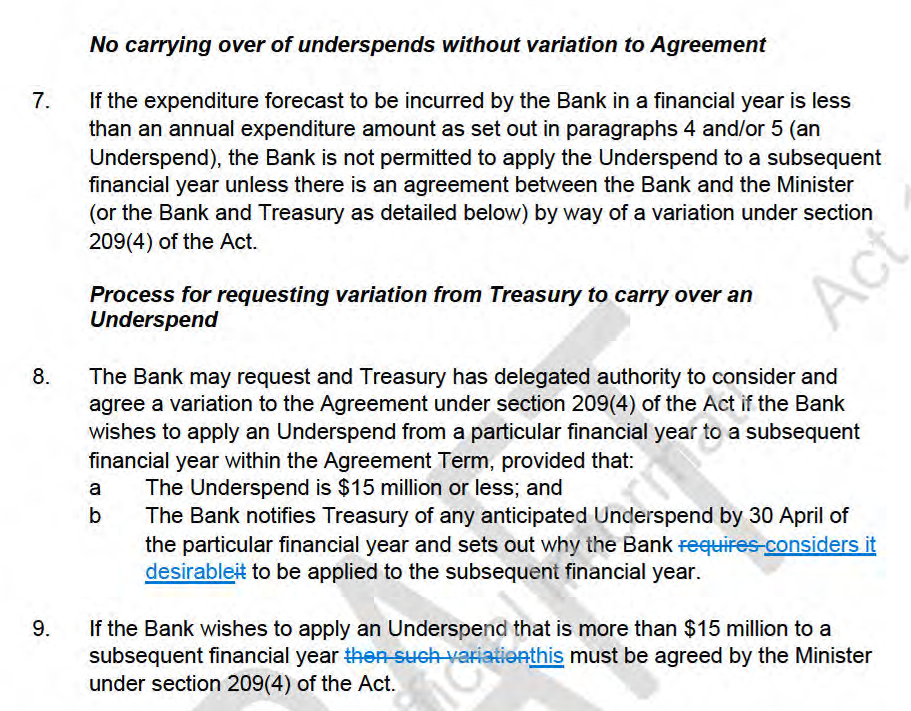

That seems sensible, making explicit what was always really the law – variations were allowed, and happened as in 2023. But is interesting that right to the end, the Bank was still championing a looser model. On their website I noticed someone else’s OIA which included a late draft of the 2025-30 Funding Agreement sent by the Bank to the Minister of Finance on 14 March (after Orr’s departure)

Presumably the Minister said no to giving that sort of leeway to Treasury. Rightly so, but where was she in pushing back on excess last year, or holding to account those – eg Board members – who nodded through the last mad wave of spending excess?)

UPDATE 17/7

Had the Bank been at all interested in transparency etc no doubt I’d already have had a response to this follow-up OIA. I expect to wait at least 20 working days.