On Twitter on Saturday I indicated that there had been a mistake in my post from last Thursday in which I attempted to step through the Reserve Bank Funding Agreement issues. Making mistakes (there are two) is annoying and I don’t fully understand how I did it (probably too much haste). I can only apologise to readers (and acknowledge that it was a sentence in the Herald’s Thomas Coughlan’s article on the Funding Agreement that prompted me to go back and check). The central point isn’t affected: real spending in the next couple of years is hardly cut at all from levels authorised by Grant Robertson just before the last election.

As it happens, since writing that post on Thursday morning a couple of other relevant documents have been released by the Reserve Bank. So, and at risk of some repetition, I’m going to attempt in this post to cover the full ground, focusing under three headings:

- the change in approved spending from one Funding Agreement (Robertson’s) to the next (Willis’s)

- the change in actual spending, and

- what seems to have gone on regarding last year’s Reserve Bank Budget and their bids for the new (just signed) Funding Agreement.

This post is long. I have a summary in six bullet points at the end.

From one Funding Agreement to the other

In the Funding Agreement for the period 2020-25, as varied by agreement with Grant Robertson in August 2023, two classes of operating expenses are separately provided for. A fairly large chunk of the Bank’s operating expenses (around $30m a year) is not covered by the Funding Agreement at all – for reasons good and less so. But of those that are dealt with by the Funding Agreement, the first class was what we might call “core” operating expenses (where $149.44m was the allowable expenditure for 2024/25) and the second is “net direct currency issue expenses” ($14.5 m for 2024/25).

In the new Funding Agreement released last week there is no longer a set of annual allowances for the currency issue expenses. Instead, under the “Excluded expenditure” heading there is provision for the Bank to spend up to $65m in total on this item over the full five years covered by the Agreement.

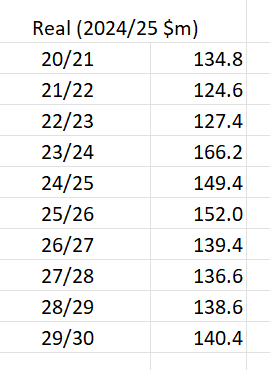

Consistent with that, in Thursday’s post I included this table, which covers the “core operating expenses” covered by the Funding Agrement in real, inflation-adjusted, terms, for the periods covered by the old and new agreements

As you can see, approved core operating expenses in the coming financial year ($152m) are actually a couple of per cent higher in real terms than those Grant Robertson had approved for the year ending in June ($149.4m). Over the remaining life of the agreement the numbers are lower (in 29/30 the approved allowance is 6 per cent below the level Robertson had approved for 24/25).

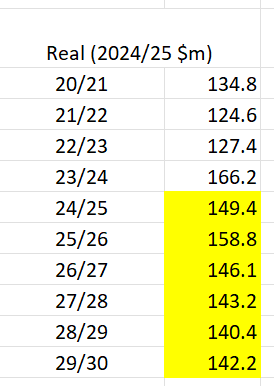

However, in the new Funding Agreement a number of new items are excluded from being counted against that spending limit. Thus, a true apples for apples comparison with approved spending levels under the old agreement would mean higher numbers for the 2025 to 2030 years. Only one of these new exclusions is quantified: an average of $5m a year for the next three years is allowed for implementing the new Deposit Takers Act (which has been being implemented gradually including over the last two years – it was part of the justification for Robertson revising up approved funding in August 2023). Other items aren’t quantified, including operating expenses associated with such potentially costly items as work on a Central Bank Digital Currency and those operating expenses associated with refurbishing or replacing the head office building. If we allowed another couple of million per annum for these other new exclusions (aiming to be conservative – low end – in our guesses), we might end up (illustratively) with a table like this

where, say, even in 2026/27 approved real operating spending would be only 3 per cent lower than the level Grant Robertson had approved for 2024/25.

Note too that the Bank’s actual and budget (for 24/25) spending on those net direct currency expenses over the five years of the last Funding Agreement was about $32 million. Although the new Funding Agreement does not provide annual limits for this item, it allows $65 million spending on it over five years in total – much higher than recent actual spending, and not very different from what was allowed in this component of the previous (2020) Funding Agreement (although note some unexpected inflation since 2020)

Overall, the new Funding Agreement doesn’t represent much fiscal restraint relative to the last approved levels by Grant Robertson in August 2023.

And it isn’t as if the Bank had been consistently abstemious over the years.

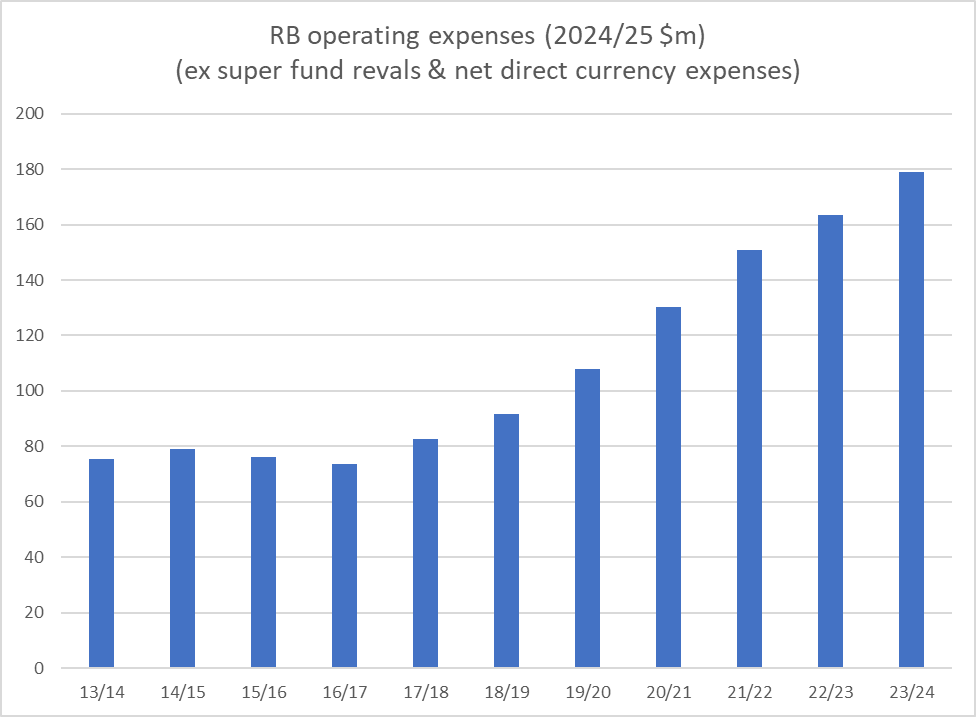

Because the definitions of what is and isn’t covered by Funding Agreements has changed over the years, it can be helpful to look at the trend in operating expenses, as disclosed in successive Annual Reports.

This chart shows actual total operating expenses in real inflation-adjusted terms (excluding actuarial gains/losses on the staff super fund, which aren’t controllable, and the net direct currency expenses item). Adrian Orr became Governor in March 2018 and real spending in 2023/24 (the last year for which we have actual data) was already more than twice 2017/18 levels.

Funding agreement vs actual and budgeted spending

The Funding Agreements cover five financial years. The Act is quite clear that when an amount is stated for each of those five financial years, that is the intended limit for that year. The Bank is not free to underspend in some years and overspend in others.

Note, however, that there is no direct disciplining mechanism. If the Bank overspends in total, or underspends in some years and overspends in others, there are no (automatic) consequences. And as I recall it, including my time on the senior management group at the Bank (long ago now), there used to be a practical view that small unders and overs in individual years weren’t too concerning, particularly so long as spending over the full five years stayed under the total allowed in the Funding Agreement.

The Bank discloses in each Annual Report how its spending on Funding Agreement items has aligned with the amount provided for each year in the relevant Funding Agreement.

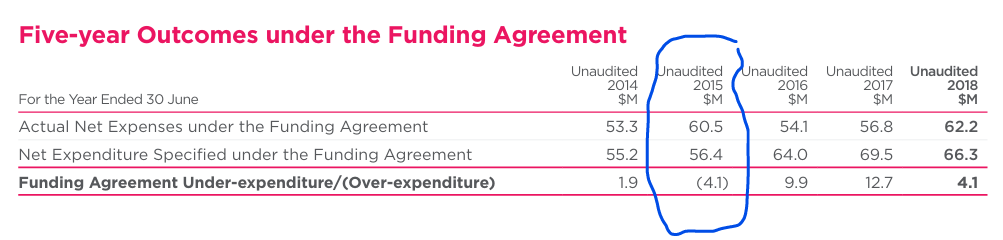

Here is an example from the 2018 Annual Report

This period happened to straddle two different Funding Agreements (and mostly Graeme Wheeler’s stewardship as Governor). Over the full five years, the Bank ran operating expenses below the Funding Agreement level. In 2014/15 they ran over the Funding Agreement amount, something that disconcerted management at the time (and prompted a round of redundancies and cost savings.

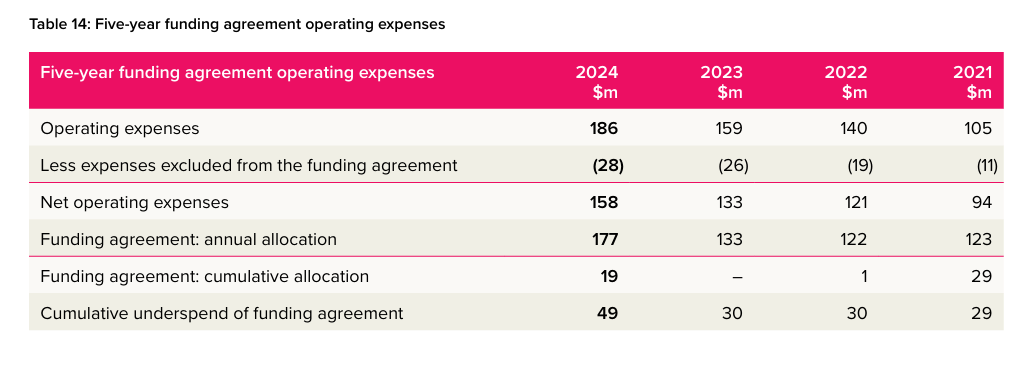

Here is a similar table from the 2024 Annual Report

Really big increases in operating spending had been allowed both in the original 2020 Funding Agreement and in the August 2023 variation that Orr, Quigley, and Robertson had signed just before the election.

You will note that in 2020/21 the Bank substantially underspent the Funding Agreement allocation (although operating spending under the Funding Agreement still increased by 13 per cent that year). In its 2021 Annual Report the Bank offers several factors as explanations for the underspend, but they mostly seem to come down to Covid (and a serious data breach the Bank experienced). I’m less interested in the specific explanations than in the final comment: “We expect this underspending to reverse in future years and the Bank to be within the five-year aggregate expenditure provided for in the funding agreement”.

Maybe that didn’t seem unreasonable at the time – Covid, after all, was out of blue for them (and all of us) – BUT (as noted above) the relevant provisions of the Act do not envisage or provide for carrying forward underspends from one year to the rest of the Funding Agreement period.

But then, as it happens, for the next two years, net operating expenses were almost bang on the Funding Agreement allowed amount (when the allowances for core operating expenses and currency issuance expenses were combined). But the Bank – management and Board – still seemed to think it was just fine to carry forward an underspend from years earlier. You can see that in the final line of the table.

You’ll also see in that table that there was a big increase (33 per cent) in approved Funding Agreement spending for 2023/24, made possible by the August 2023 variation. The Bank then underspent that allowance rather dramatically ($29m), even though they’d increased (funding agreement covered) actual operating expenses by almost 19 per cent in a single year. This was still a year (more than half of which occurred on the watch of the new government) in which they had increased actual FTE staff numbers by 91 (18 per cent). As for that delayed project spending, it doesn’t seem like great management and Board oversight given that they’d only got Funding Agreement variation approval as recently as August (ie already into the relevant financial year).

By the end of the 2023/24 year the Bank’s total (Funding Agreement) operating spending was a total of $49 million below the sum of the Funding Agreement limits for each of those four years. $19 million of that shortfall had occurred years earlier.

But what of it? Recall that under the Act, there really wasn’t discretion for the Bank’s management and Board simply to decide to shift large amounts of spending from one year to the next. (No one might have quibbled over a few million here or there – given the way the Funding Agreement system and legislation were set up – but…..this was $49 million).

And, by then, we had a new government, which had made quite a fuss in the election campaign around bloated public spending, and had started on cuts to most central government departments.

The Bank’s 24/25 budget, Statement of Performance Expectations, and 2025 Funding Agreement bids

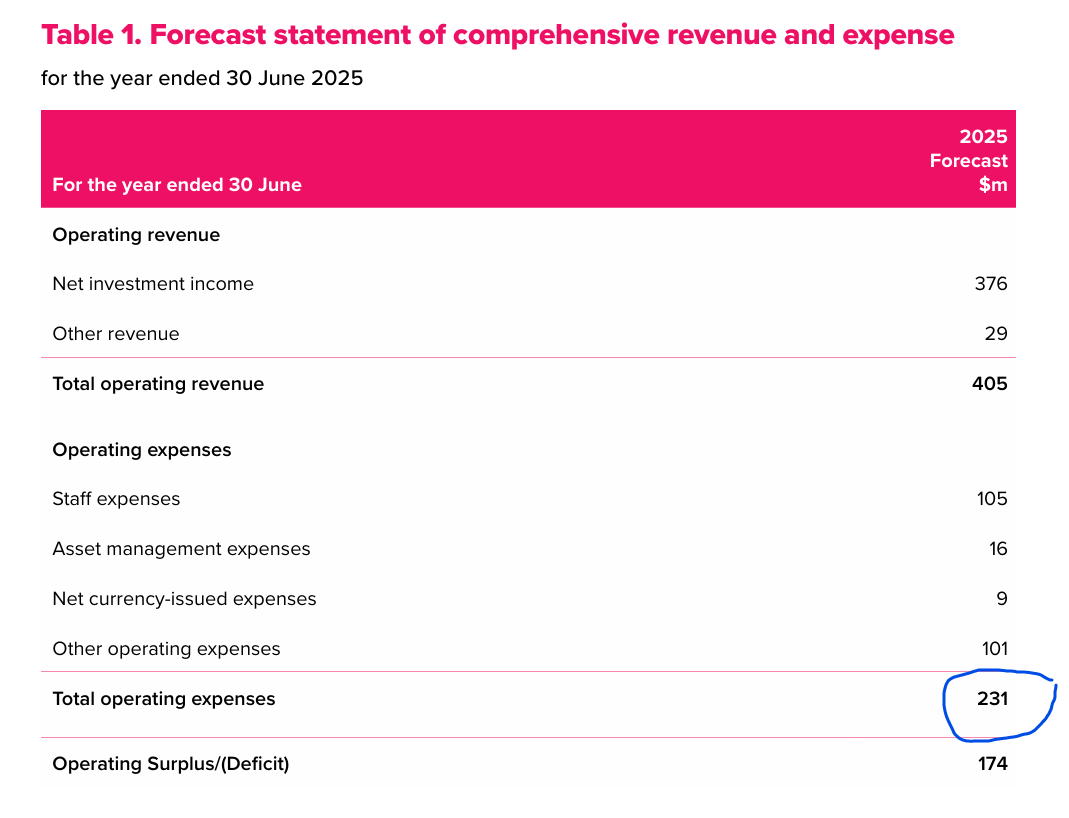

Annual budgets are set by the Reserve Bank’s Board which now has full responsibility for the governance of the institution. The high-level budget numbers are published in a document, required by law, called the Statement of Performance Expectations. Last year’s was signed (by Governor and Board chair) on 21 June and included this table.

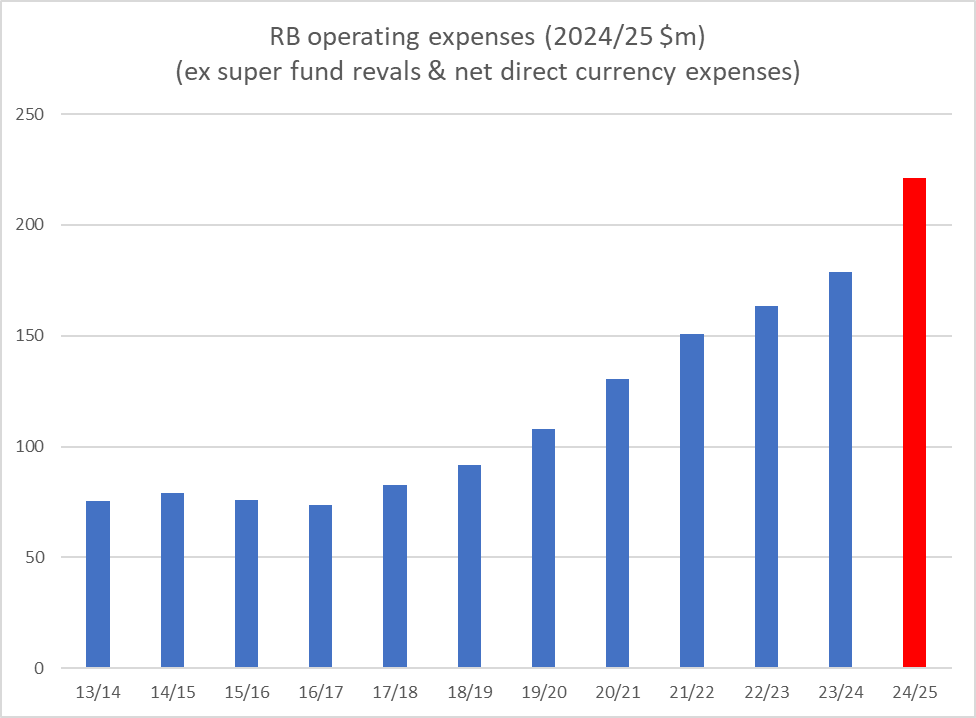

Here is the chart above updated for the Board-approved 24/25 budget

It was to be the largest percentage increase in core operating expenditure in any of the Orr (& Quigley) years (about 24 per cent in real terms).

The Bank does not report its budget on a Funding Agreement-consistent basis, but the proactively released Board minutes indicate that $31m of the operating expenses were on items not covered by the Funding Agreement. So $200 million was on item covered by the two Funding Agreement streams, up from $158m actual spending on these streams in 23/24 (the Board would not have had final 23/24 numbers when they approved the 24/25 budget on 20 June, but the estimates must have been pretty close).

How did this happen you might be wondering. After all, hadn’t the Minister of Finance handed down her overall government budget as recently as 30 May with a heavy, and very public, emphasis on expenditure savings and redirection of resources towards so-called frontline services? Those with access to the Minister might well ask her.

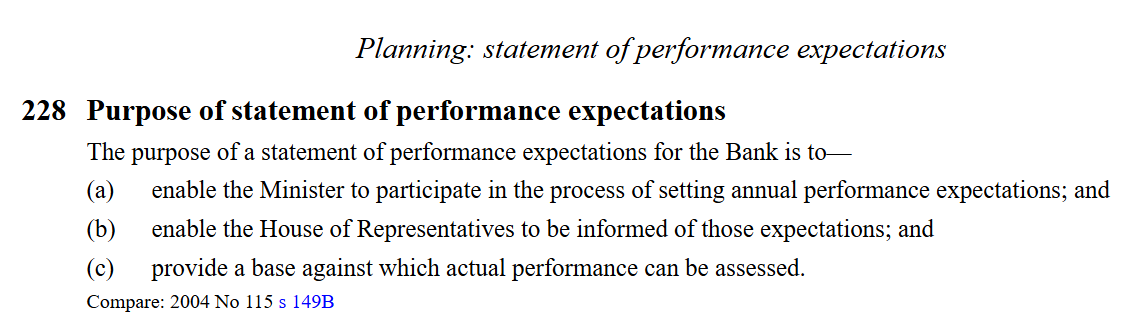

Perhaps you are wondering if the Board did all this 24/25 budgeting in secret, and the Minister of Finance simply didn’t know. But the numbers had to be included in the Statement of Performance Expectations (SPE) and the Minister had to be consulted on a draft of the SPE. In fact, the law says that a main point of the SPE is to enable the Minister to be involved

and the “how” is covered, among other sections, here

And it isn’t as if somehow the Bank overlooked the need to provide a draft to the Minister last year. The Board minutes for 20 June record that written comments (on the draft Statement of Intent and the draft SPE) had been received from both the Minister of Finance and Treasury and “had been incorporated”. There is no suggestion of any material difference of opinion, or of the Minister taking a harder line than the Board. It is really quite extraordinary…..coming just weeks after the expenditure saving and reallocating government budget. One of her agencies was going to increase spending by 25 per cent or so, in a single year.

What was the Minister thinking/doing? What was Treasury thinking/doing? (I have lodged an OIA asking for the comments from both of them on the draft SPE.)

Now, again if you were inclined to bend over backwards to excuse her responsibility you might note that the Minister of Finance could not formally stop the Bank’s Board setting the budget for 24/25 at any level it liked. The Bank has that degree of operational independence.

But…. she is the Minister of Finance and has a bully pulpit. Imagine if she’d told the Board “well, you can increase your budget by 25 per cent for this coming year if you like, but if you persist in doing so I will go public and excoriate you for a reckless and irresponsible use of public money, for operating in breach of the Funding Agreement, and for choices that are utterly out of step with the government’s wider fiscal priorities. Do we really suppose there’d have been a wave of public sympathy for the Board?

More directly, Board members are appointed by the Minister of Finance. Reserve Bank board members cannot be dismissed at will, only for cause. But the Reserve Bank Board chair’s term was due to expire on 30 June 2024. It had been widely assumed that, having been in place for many years, he’d be replaced by the new government. Being responsible for an egregiously large budget increase might have been just another reason to replace Quigley. Instead, Willis reappointed him, and as if to add insult to injury she announced that puzzling reappointment on 20 June, the very day the Board confirmed that huge operating expenses budget, that she’d had every chance to comment on.

Like many, I was genuinely mystified last June when Quigley was reappointed. Now that one realises (a) the timing and b) the huge budget increase he was overseeing I’m simply flabbergasted.

(Note that the 2024/25 Budget was so out of step with the Funding Agreement provisions/levels there would appear to have been – perhaps still would be – good grounds for the Minister to dismiss board members for cause (not one of them having recorded a dissent when the budget was adopted).)

Now, as a final effort towards trying to understand what she might have been thinking, perhaps the Minister was advised by the Board and management that the Bank was simply utilising the underspends from earlier in the Funding Agreement period. The Bank was claiming (see table above) that they had $49m up their sleeve. Add $49m to the Funding Agreement allowances of $149.4m for 24/25 core expenses and $14.5m for 24/25 net currency issuance expenses and you get $212.9m. Perhaps it looked as though the Bank’s big new budget ($200m on Funding Agreement items) was actually less than was allowed.

If the Bank claimed as much to the Minister, we might (at a pinch) excuse her. She is busy and you might assume the board of your central bank was giving you honest advice and an honest interpretation of the Funding Agreement and Act. But……she has an entire department of her own, The Treasury, supposedly expert in such stuff. And they should have told her in no uncertain terms that neither the Funding Agreement nor the Act envisaged carrying forward substantial underspends from past years to allow lots more spending in later years. To be consistent with the Funding Agreement, the Bank’s total (funding agreement covered) operational expenses could be no more than $163.5m in 2024/25. Not $200 million.

Why weren’t they (apparently) doing those basics properly? It is clear that they had seen the draft SPE and the Board minutes record regular senior-level engagement with Treasury (a couple of Treasury DCEs often attended a session with the Board, and sometimes the Secretary herself). They’d been overseeing the advice on the government budget, probably putting pressure on numerous departments to deliver savings. And yet the Bank’s Board adopted a budget with a 25 per cent or so increase in operating spending, and nothing seems to have been said or done.

All of which brings us to the 2025 Funding Agreement (bids and final settlement).

The Minister had written a Letter of Expectation to the Board chair in April stating, among other things,

The messaging seems pretty consistent with what the Minister had been saying in public (see references to the “fiscal sustainability programme”)

Here it is helpful that late last week the Bank finally get round to proactively releasing the Board minutes for the September quarter of last year. You may recall that in the paper to the Cabinet committee on the new Funding Agreement the Minister indicated that

This submission was approved at a meeting of the Board held in Auckland on 29 August late year. The minutes record as follows

It is quite explicit there that they had bumped up the 24/25 budget massively – using some illegitimate argument about carrying forward past underspending – not just to clear out some backlog one-offs, but providing a baseline for their bid for operating spending for the following five years. You’d think perhaps we were still in the era of Grant Robertson budgets. And although it is easy to focus on Adrian Orr as Governor, these bids – and the budgets – were the responsibility of the board, and particularly its chair, Neil Quigley.

But there are still puzzles. For example, note that in the paragraph above the one I highlighted the minutes record the Board’s understanding that “the Minister of Finance’s expectations for the funding proposal are met, including that multiple options for achieving savings are provided”. What, one is left wondering, led them to think that what they were bidding for had met the Minister’s expectations (presumably as conveyed not only in that April Letter of Expectation but in regular engagement with top Treasury officials)?

The Minister now is keen to highlight that she cut back the Bank’s spending relative to its 2024/25 hugely increased budget (not by 25 per cent but probably by an apples-for-apples 17-18 per cent or so) but (a) how did she let the budget happen in the first place, b) how did the board get the impression that its bid for massively increased real resources (relative to the previous Funding Agreement) met her expectations, and c) why did it take so long then to pull the Funding Agreement bid back to earth? Given that she has made clear that Orr’s resignation did not have to do with the Funding Agreement, we might reasonably also ask why no one involved has lost their job over this?

The initial Funding Agreement bid wasn’t approved, but you’d have thought the Minister – and Treasury – would have told them many months ago that a bid based on the inflated 24/25 budget simply wasn’t acceptable, and that they should go back and try again, perhaps benchmarking themselves, as a start, against the last ministerially approved level of spending (the 2023 Robertson variation). But they seem to have done nothing of the sort, and there wasn’t a revised funding proposal from the Board until a week or so after Orr left. We are left to wonder if – and one really hopes it is not so – it was not until very late in the piece that the Minister and Treasury actually started demanding some serious fiscal restraint from a Bank that was (a) far overspending its own Funding Agreement approved levels for 24/25 and b) wanted that to be the starting point for what they could spend for the next five years. As it is, even the final settlement – above what Treasury had wanted – largely validates the bloated spending and organisational size up to 2023/24, just undoing the further excess that occurred on Willis’s own watch.

(Note too that we do not know how much actual spending will have to be pulled back in 2025/26 as all the papers refer only to last June’s approved budget and not to any mid course corrections the Bank may have made. The board must have updated forecasts of actual operating expenses for 24/25 but none of that has been disclosed. That said, any such mid year savings might be small: after all, as the Cabinet paper disclosed, the Bank increased staff numbers by another 10 per cent between 30 June last year and 31 January this year. In straitened fiscal times….)

Finally, I noted in the posts late last week that the Bank was then in breach of the Act, which requires a Funding Agreement when published to

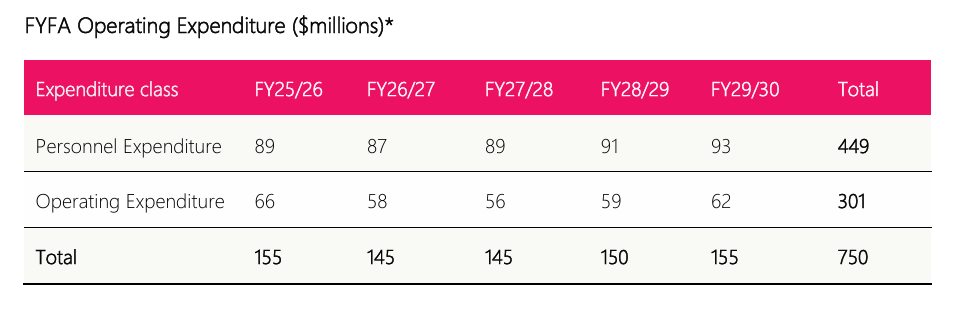

A document purporting to meet this requirement seems to have turned up on website on Thursday afternoon. On the operational expenditure side this is all there is

Not only is there is no starting point comparison (forecast figures for 24/25) but there is no information at all enabling us (public or, say, FEC) to know in what functional areas the Bank will be looking to make cuts. This document probably doesn’t meet the statutory requirements but if it does it just highlights again how deficient the Reserve Bank funding legislative framework is, including the absence of any requirement for parliamentary approval. That was an egregious omission (when the legislation was amended by the previous government) but the gap is even more stark now when considered against what the Reserve Bank Board (and management) got away with last year.

Summary

There was a lot of ground to cover. My bottom lines messages are as follows:

- the new Funding Agreement represents pretty limited cuts in the Reserve Bank’s authorised spending, using as a benchmark the previous Funding Agreement variation in 2023,

- the Minister of Finance appears to have done nothing when advised in the first half of last year that the Bank’s Board was proposing a near 25 per cent increase in operational spending for the 24/25 year, and in fact announced the reappointment of the Board chair the very day the Board gave final approval to that budget,

- the Bank’s Board was in breach of its collective duties in authorising 24/25 spending far in excess of what the Funding Agreement allowed for that year, and

- was egregious in bidding for that 24/25 grossly inflated level of spending to be the baseline for the next Funding Agreement period,

- where was Treasury in all this?

- how can we have any confidence in those involved at the Bank (board chair and members, senior managers including the CFO, the former Governor – now gone – and the Deputy Governor, currently the temporary Governor)?

Appendix: Aggregating the Two Separate Streams of Spending in the Funding Agreement

There is an aspect of the 2023 variation to the Funding Agreement that deserves a bit of attention, without distracting from the main flow of the argument.

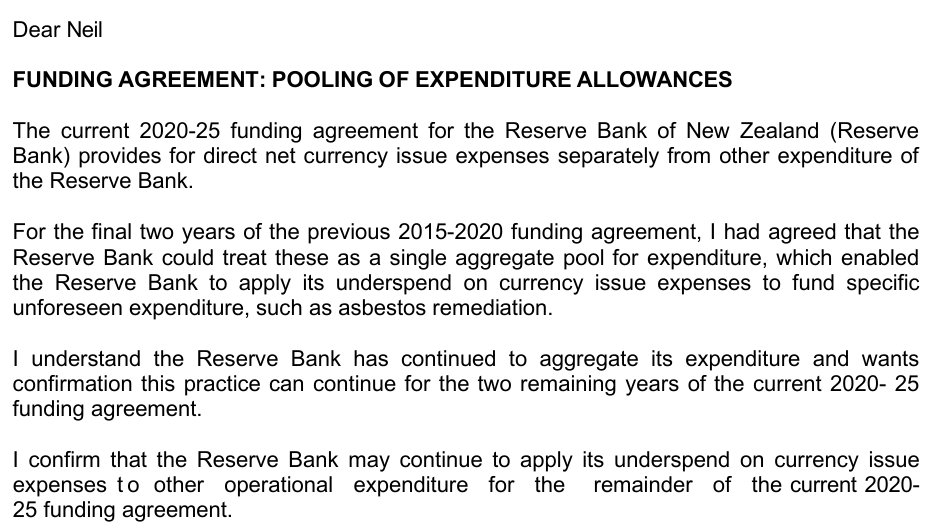

This letter from Grant Robertson to the board chair, Neil Quigley accompanied the 2023 variation to the Funding Agreement

There is a good logic to providing separately for (net) direct currency expenses, since currency issuance is a (the key) profit centre for the Reserve Bank, and we wouldn’t want any incentive for the Board or management to skimp on spending there to give them more freedom to spend on nice-to-haves.

According to Grant Robertson’s letter, the Bank wasn’t needing to spend as much as allowed (in the 2015-2020 Funding Agreement) on currency in the late 2010s, and on the other hand faced some unanticipated cost pressures in other areas (the asbestos remediation referred to in the latter). Grant Robertson’s permission then was, in many respects, equivalent to a variation to the Funding Agreement, raising the amount that could be spent in 2018/19 and 2019/20 on core operating expenses and reducing what could be spent on net direct currency issue expenses. That may well have been a reasonable call by the then Minister of Finance (and is water long under the bridge now).

But, remarkably, Robertson’s letter suggests that whereas he had given permission for the two Funding Agreement expenditure components to be pooled for 2018/19 and 2019/20 for a specific purpose (that asbestos remediation), the Bank had actually treated it as carte blanche, a general permission to pool the two buckets that had deliberately been set up separately, so as not to be pooled. It appears they had had no authorisation for doing so at all. Perhaps by 2023 someone was asking questions (Treasury, or just possibly the Bank’s Board which actually became formally responsible for the governance of the Bank on 1 July 2022)?

That 2023 Funding Agreement variation had already given the Bank a massive increase in permitted core operating spending (up a total of $79.3 million for the 2023/24 and 2024/25 years). But in addition, Robertson allowed them to add any underspend on currency issuance to their other operating spending (another $6m a year or so). Note that this aggregation was only allowed within years, and there is never suggestion that underspends can be carried forward into overspends in subsequent years.