I’ve written a few sceptical posts here over the years about the annual (or so) Technology Investment Network’s (TIN) boosterish reports on the New Zealand tech sector. The overall story was just even close to as upbeat as the reports liked to make out.

Yesterday a link to a new TIN report turned up in my email inbox. This was the bit in the email

There is a clue right there in the reference to chocolate chips. This wasn’t going to be a report about what most people have in mind when they think “advanced manufacturing” but about the manufacturing sector as a whole. All firms in the sector use technology of one form or another, some of it very advanced.

Anyway, I downloaded the full report (you have to register to get it, but it isn’t onerous, and the report itself isn’t overly long, at about 30 pages of substance). It turned out to be the product of a bunch of outfits I’m pretty sceptical of. There was TIN itself which did the work, there was the co-chair of the Advanced Manufacturing Industry Transformation Plan Steering Group (ITPs being that throwback to the 1960s that the outgoing government became keen on) who supplied the Foreword talking up both his group and document, and then there was MBIE which is said to have “commissioned this report” and presumably paid for it. Money was being thrown around in all too many areas under the outgoing government.

Both the Foreword (by Brett O’Riley) and the Welcome (by the Managing Director of TIN) are pretty upbeat. O’Riley makes the bold claim that manufacturing is “the backbone” of the economy (to which I responded on Twitter this way

After noting that the manufacturing sector will soon drop to being only the third biggest greenhouse gas emitting sector (behind households and agriculture) the Welcome ends this way

It all sounds good quite upbeat.

That is, until you read on.

There is a helpful Executive Summary. It also attempts to start upbeat

Advanced manufacturing is a critical engine of Aotearoa New Zealand’s long-term prosperity, making a vibrant contribution to the nation’s economy

But then the pesky data start getting in the way

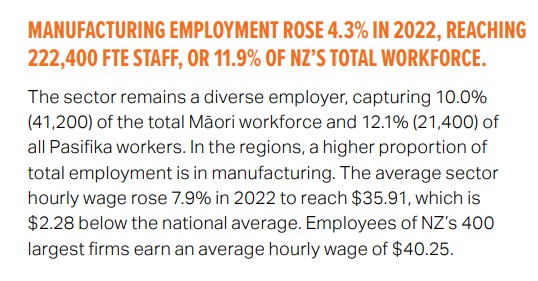

There are still lots of workers

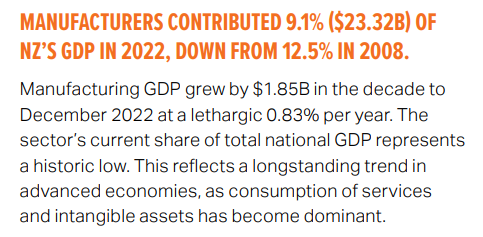

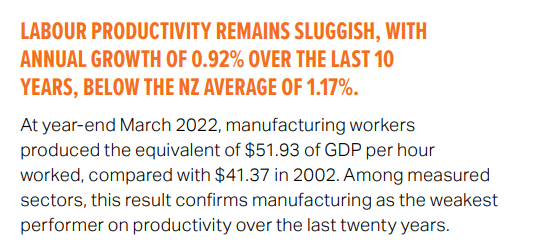

But if your sector is 9.1 per cent of GDP and 11.9 per cent of the workforce, what does that say about productivity?

Low level, and low growth rate. Ouch.

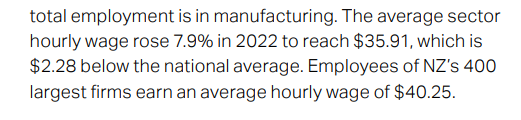

And, unsurrpisingly wage rates in the sector as a whole are below the economywide average.

You might have noticed in that clip at the top reference to 60 per cent of New Zealand’s exports. That is because many of New Zealand’s agricultural exports are processed (dairy factories really are big and sophisticated operations, even if the share of that processing in total dairy value-added is not huge). Anyway, exports….

Not exactly a positive story either.

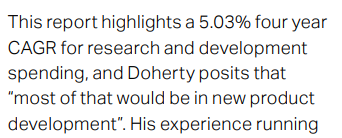

The puff piece at the front was upbeat on R&D (‘over a quarter of national R&D spending comes from manufacturing’) but by the time you get to the Executive Summary a less rosy picture emerges

So that is quite a big drop in the share of national R&D spend, and manufacturing sector R&D staff are almost the same share of total R&D staff as manufacturing employees are in the total workforce (although to be fair one has to wonder a little about whether the comparisons here are all apples-for-apples, since if manufacturing does 27 per cent of the national R&D spend with only 12 per cent of the R&D employees, those manufacturing R&D employees must be doing a lot of work/spend each).

What of FDI? Manufacturing does seem to represent a larger-than-representative share of inward and outward FDI, but…

By my reckoning that compound annual growth rate for inwards investment was less a bit less than the growth in nominal GDP over that period, so not exactly a very positive story for “the backbone” of the economy, “a critical engine” of New Zealand’s “long-term prosperity, making a vibrant contribution to the nation’s economy.

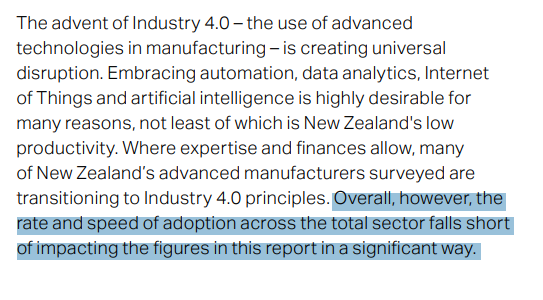

The report would really quite like to be upbeat about new technologies, but….

And those were the last words of the Executive Summary.

There are some more detailed sections that follow. A new snippets:

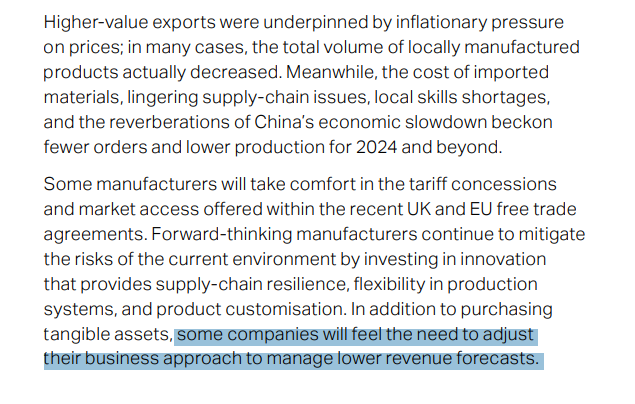

On international trade:

in addition to that wonderfully-understated last couple of lines, note “in many case, the total volume of locally manufactured products actually decreased”, and “[various factors] beckon fewer orders and lower production for 2024 and beyond”

On R&D etc:

Nominal GDP rose faster than that.

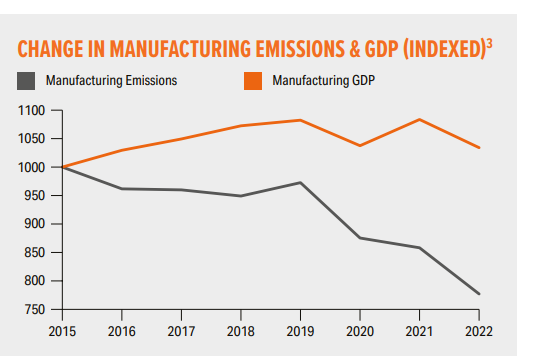

And this grim observation

The exciting news is that emissions have dropped, and not just because of a dismal GDP performance, but that is an input, not the sort of outcome firms go into business to achieve.

What of profits? They grew more slowly than nominal GDP over this period, and represent 7.6 per cent of economywide profits even though the sector is 9.1 per cent of GDP.

The best you could really say for this report is that, underwhelming as the data are, perhaps it provides some sort of benchmark against which to measure where things go from here. But why the spin upfront, and why was the taxpayer paying for the report in the first place?

None of this is intended as a criticism of any specific company in the sector. Companies that survive and thrive in New Zealand, selling to world, deserve a fair bit of admiration and in the case studies at the back of the report there are some really inspiring stories (I don’t include taxpayer-subsidised NZ Steel among them, nor perhaps the company that has been running since 1981 and has a grand total of 115 employees). In all my years at the Reserve Bank one of the best things I ever did was to participate in the regular business visits programme, and it was rare not to come away from each and every company we visited admiring people – often owner-operators – who had everything on the line to make and sustain a business (it was hard not to think they were doing something better or more useful – certainly much more risky – than we were).

But the aggregate story just doesn’t seem to be a very positive one, if such aggregates (“the manufacturing sector”) make much sense at all (the New Zealand “manufacturing sector” is a very diverse thing, including new and cutting-edge firms and legacy companies from the eras of protectionism and Think Big). Beyond the puff pieces at the start, there is a certain grim realism about many of the comments on the numbers (see above), but perhaps it would have been better to have had that upfront, grabbing the headlines.

There is no right or wrong answer as to how much of a “genuinely” advanced manufacturing sector a successful New Zealand economy might be expected to have, but it isn’t surprisingly the sector struggles here when you combine things like distance, high company tax rates, obstacles to foreign investment, and a real exchange rate that for decades has been out of line with relative productivity fundamentals