One thing in the National Party’s call for a public inquiry into monetary policy that I didn’t comment on yesterday was the framing. The press release is headed “Inquiry needed into impact of tidal wave of cash”. It is a framing I have never liked, whether coming from critics on the left or the right.

My point here isn’t to bag National. They ran with a catchy headline, but the body of their release talks more generally about the overall conduct of monetary policy. But it is a framing that isn’t uncommon (loose talk of “money printing”) so it is an opportunity to restate my view – probably a minority view, but I stand by it – of the macroeconomic irrelevance (to a first approximation) of the Reserve Bank’s LSAP programme.

Rather than write something fresh, here I’ve reproduced the relevant sections of a lecture I gave to some Victoria University masters students in December 2020. Probably no more than any other commentator, I won’t stand by everything I’ve written on monetary policy since the pandemic began. but this 20-month-old view (typos and all) is largely still my view today.

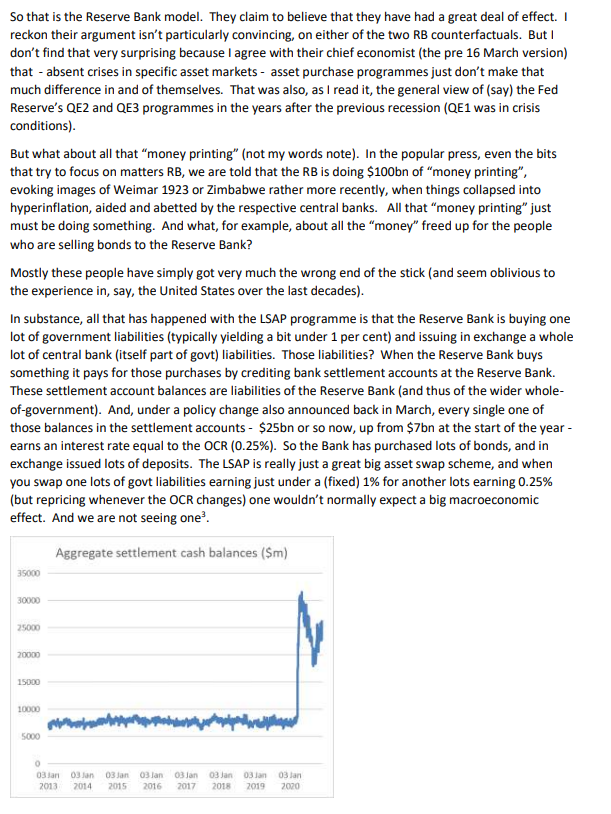

It was an asset swap that involved the central bank taking on a huge amount of risk, and there is little credible basis for supposing there was any material macroeconomic effects (lower short-term interest rates and fiscal policy did the stimulus). Banks are not, in aggregate, settlement cash constrained. Shorter-term rates are what mostly matter in New Zealand, and so even if the Reserve Bank’s purchases managed to have some sustained impact on long-term rates they just don’t matter much in the New Zealand transmission mechanism.

Oh, and that risk was taken on without any sign that any robust financial risk analysis was ever undertaken by the Bank, by the MPC, or by The Treasury. There is no sign the Minister of Finance ever asked for one. And so in something of a panic (LSAP hadn’t previously been their preferred instrument), wanting to be seen to be “doing something” they rushed into purchases, no doubt thinking they were doing good, but actually with little sustained prospect of doing so. And as the Minister of Finance put it in Parliament yesterday, in a set of answers that suggested some distancing from the Bank.

Interest rates have shifted since that time and, as with our fiscal response, there are costs associated with the measures that the Reserve Bank took. The latest estimates from Treasury of this cost is around $8.46 billion.

Or about $8000 per family of five.

The final couple of sentences in the extracts above might have raised some eyebrows. Here is what I went on to say about housing later in the lecture.

People today are quite free in attacking the Bank for lifting LVR restrictions in March 2020. I continue to believe that, in the context of other policies being adopted at the time, and the generally prevailing view at the time that a Covid economic downturn would be associated with falling house prices, lifting those restrictions was both right and inevitable. From the time LVR restrictions were first put in place in 2013 it had never been envisaged that they would be left on if house prices started falling: the original conception of LVRs was to lean against excessively liberal lending standards, not usually a problem when the underlying asset value is falling. The big change came later when the Orr Reserve Bank moved, wrongly in my view, to make LVR restrictions a permanent feature of the landscape – whether or not there was any sign of lots of poor quality lending, whether or not there were evident financial stability risks. Financial repression always sows seeds of future problems.

Not to start a lengthy new discussion, but for much of 2020 and early 2021 the problem proved to be a forecasting problem. The Reserve Bank and The Treasury, and most private forecasters, had the wrong model of pandemic economics. They (we) assumed there would be a larger element of an adverse demand shock than there proved to be. That was certainly a mistake I made: as just one example, my approach from March 2020 had been that the inevitable uncertainty (virus and policy) would act as a considerable damper on (highly cyclical) investment spending, all aggravated by the population shock wrought by the closed border. One can trace forecasts – official and private – from early 2020, and it is clear that until perhaps May/June last year the problems were forecasting failures. It was only from then, perhaps until about March this year, that the Reserve Bank’s failings were in how it responded to contemporaneous data and its own forecasts.

The LTSA positioned the banks for windfall profits-their cash balances await top reinvestment rates.They simply shovelled bonds to the RB some brokered from other holders.So they profit from selling at low rates and again from reinvesting at topout rates, as those then temper.Good to see the graph on cash balances. This was an easy référence point as the LTAP proceeded.As you say, the Bank’s didn’t need settlement cash to support the economy. Not that they did anyway – lending stats should support this.Phil Hogg0274442553Sent from my Galaxy

LikeLike

The RBA took a different approach to LSAP, namely yield-curve-control (out to three years). They accomplished the same feat as the RBNZ – lowering wholesale rates – without having to buy a massive amount of bonds (the RBA didn’t have to drive the 0-3 year curve down, just the threat to so if the market didn’t adjust was enough). Later on the RBA did buy longer-term bonds but overall they accomplished their goals at a lower cost relative to the RBNZ………Did the RBNZ consider this approach? If not, why not ?

LikeLike

Not a huge difference, really.

https://www.rba.gov.au/chart-pack/central-bank-balance-sheets-bond-purchases.html

LikeLike

A recent analysis by Westpac concluded “For the RBA we have calculated that the cost to the balance sheet in terms of mark to market is currently $37 billion. It would have been $11.6 billion higher if it had adopted bond buying from March 2020 instead of yield curve control”. As an aside, there is no mention of any indemnity; I wonder how the $37 billion loss is going to be handled ?

LikeLike

I think there is a general expectation that at some point the govt will recapitalise the RBA, but it could be done by simply not paying dividends for as long as it takes for time and seigniorage to do the job.

LikeLike

If Westpac is right the RBA saved itself $12 billion by using yield curve control for a period, then proportionately the RBNZ could have saved itself circa $2billion by doing the same …

LikeLike

Indeed. I’ve long argued that anchoring say thr 3 yr rate would have delivered thr desired mon pol effect at much less cost.

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike