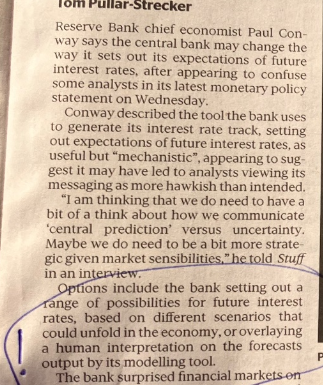

An article in this morning’s Post, reporting comments from Paul Conway, chief economist of the Reserve Bank, prompted me to go and listen to the Governor’s MPS press conference. I’d largely given up watching them.

This was the most interesting bit of the article

although it was followed with more comments trying to reframe what the Bank had published in the MPS only a couple of days ago.

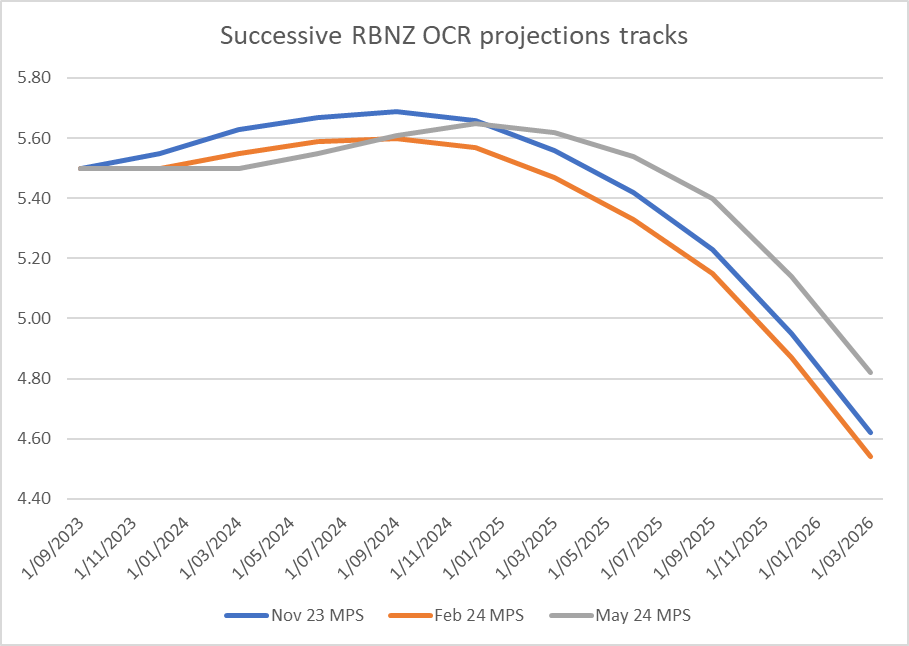

The Bank has been publishing a so-called endogenous track for short-term interest rates, as a central indication of what it believes to be required to deliver inflation at or near target 1 to 2 years ahead, for more than 25 years now. If the current crop of MPC members doesn’t yet understand how their numbers will be interpreted, that is more of a reflection on the MPC, and their chief economics adviser, than on the tool. (I’m not a big fan of publishing medium-term interest rate projections – never have been – but it is hardly a new or unfamiliar tool).

So when you published an OCR track that is revised up and out

you know the likely reaction, likely questions etc. And when you complement that numerical track by explicitly stating that the MPC actively considered raising the OCR at this very meeting, you shouldn’t be surprised you are going to be challenged. On a central track, where the OCR is averaging 5.65 per cent in the December quarter, that is consistent with a high probability of an OCR increase later this year.

If the Bank didn’t want people to take that interpretation (and both Conway’s comments in this article, and his and Orr’s comments at the press conference suggest they didn’t), they should have published different numbers. The comments from Conway in the Post article suggest that somehow the OCR projection track was outside their control – product of “its modelling tool” – when it has always been clear that the projections are the MPC’s, not some staff model (which itself has considerable human interventions pretty routinely). Perhaps it is different now, but in the many many years when I sat on the equivalent of the MPC, we used to spending huge amounts of time (arguably at times inordinate) on those last tweaks to the interest rate track, bearing in mind how any numbers would be read by outsiders. There was never a time when any published forecasts – and particularly for the interest rate track – were just some sort of machine-generated product.

Listening to the press conference for the first time in a while just confirmed a sense of how inadequate the MPC, and its chair, are for the job they’ve been charged with. They didn’t have a straight story to tell, and they were trying to back away from the clear implication of numbers they’d chosen to publish. To which one could add yet another appearance saying nothing of substance from the deputy chief executive responsible for macroeconomics and monetary policy at the Bank, or a Governor who chose to opine on productivity growth or the lack of it, suggesting that things were different (better) in Australia, even though recent productivity growth there has been just as weak as in New Zealand. Why are these people – having delivered us the inflationary mess in the first place – still in office? New Zealanders deserve better from officials – supposedly expert ones – delegated so much power. Apart from anything else they deserve real expertise and real accountability.

But then there was also a sense of how weak the media scrutiny was. Was it really the case that no journalist had wondered quite how economic growth was supposed to rebound, on these projections, with real interest rates already restrictive and set to rise further, fiscal policy restrictive, no help from the world economy, and with an expected further downturn in the net immigration impulse? In any case, none asked. None asked why if the OCR had helped lower the output gap by almost 5 percentage points so far, a continuing high OCR, rising further in real terms (as inflation and expectations fall but the OCR doesn’t), was only going to lower the output gap by a little more than 1 percentage point.

And remarkably no journalist asked, and no central banker mentioned, the very real lags in monetary policy. If the real OCR keeps rising to at least the middle of next year, won’t that be acting as a material drag on economic activity and inflation for a couple of years after that? And yet, on the Bank’s projections – the ones the Governor was presenting and journalists were supposedly questioning – quarterly inflation is back at target midpoint by the middle of next year, and – on the Bank’s telling – goes no lower from there.

The puzzles are real.

Clearly RBNZ doesn’t have a strategy to communicate consistently and now resorts to “trust us we know what we’re doing” stuff.

I know you’re not a fan of NGDPLT – mainly as I understand it for measurement reasons? and because NLGDP should just be one of the considerations for effective MP, but David Beckworth’s 2019 short article on it makes I think a couple of good points:

Right now we seem to have persistent non-tradeables inflation supported by persistent Government spending – I.e a demand problem. Keeping the OCR up will affect (delay) investment for future growth and supply and productivity – and NGDP has slowed in Dec 2023 already (its distressingly late waiting another month for the April quarter figures), while broad money is still growing at 4.0%. No easy fix for this mess.

LikeLike

Note that price level or nominal GDP level targeting would, all else equal, require a much longer period of tight monetary policy, to reverse the past big policy error. Of course proponents would argue that a different regime might have reduced the chance/size of the initial big error, but I’m sceptical of that in this case because much/most of the error was forecasting mistake (the Bank didn’t realise how much pressure was building up).

LikeLike

A forecast is based on the assumptions. Predicting the future is difficult but nevetheless you must forecast. That gives you a baseline to work with. As time passes and events change then the assumptions will adjust will affect the forecasted outcomes but it allows a investigation of what actually happened versus what was assumed that will happen but did not.

LikeLike

There are no puzzles. This is a tea leaf operation. You could do this from your kitchen table.

The Mcbank has no other function than to facilitate the governments desire to spend without raising taxes immediately. It is there to put lipstick on the socialist pig.

The constant modelling and regurgitation of breathless thoughts about the future serve only to remind us that the reason we have this tiny tot McMoney franchise is to keep faith with other equally insolvent uniparty governments. Close it down , no one will notice its gone.

LikeLike

The future is inevitably a tea leaf operation or crystal ball gazing. Only God knows what will happen in the future. Mere humans will take a best guess approach. Lay out the assumptions and forecast the future based on the assumptions. If the modelling tool works and with the computational power that computers have these days then if all the assumptions laid out happens, the forecast should neatly tie in with actuals.

I have to say that I am more inclined today to be impressed with the RBNZ. Somehow with QE and its washout, our government has ended owning Kiwibank 100%. What other Central bank has managed to achieve this outcome from QE?

Our Financial institutions look rock solid. With only around $100 billion in export trade and $400 billion in NZD traded, our NZD is backed by nothing more than Monetary policy discipline is the 11th most traded currency in the world. It allows us to buy anything we want from anywhere around the world.

LikeLike

Perhaps the RB intent is to say “yes we know we have to do more to reduce inflation but really we are nice people that don’t want to raise the OCR !.

Never mind that, unpalatable decisions some times have to be made.

What is their reply to broad money increasing at 4%? ( is this an official figure? )Given the productivity decline that points to a needed OCR of 5.65 plus!

And a new government deficit yet to be announced.! It seems today everyone and their dog have cast iron cases for more largesse from the taxpayers.

The upcoming budget will answer some of these questions but again most budgets are usually wrong before they have been signed off

Inflation is still with us.

LikeLike

Rather stupidly to worsen productivity, Mike Hoskings calls for the Australia to return crime ridden New Zealanders bred in Australia to compulsorily return to New Zealand.

This morning, Mike Hoskings was on about Australia has the right to kick back New Zealanders that have overstayed their welcome in Australia after having committed crimes and that the Albanese government had done the wrong thing in keeping crime ridden Kiwis in Australia rather than kicking them out back to New Zealand.

Mike Hoskings quite stupidly forgets that New Zealand is actually a named founding state of Australia on the Australian Constitution. New Zealanders have every right to stay in Australia if they choose to live in Australia. It is more ridiculous that a founding state of Australia cannot freely come and go from Australia. It is the birthright of New Zealanders.

LikeLike

I have often asked how to interpret RBNZ forward OCR track.

Current OCR is 5.50% and has been for some time. Absent change, the quarterly number should stay fixed at 5.50.

If a future average quarter level is 5.65% this surely suggests a change upwards during that quarter.

The history of NZ OCR is that it has been changed in increments (plus or minus) of 25 basis points. A 15 basis points change in the quarterly average suggests a +25 bp change for 60% of the quarter – 2 months ie about the beginning of November. {A 50 basis points increase at the beginning of December would yield the same result but I don’t want to muddy the argument I’m about to make).

So the next quarter would start with an OCR of 5.75%. No change during the quarter would see the average as 5.75%.

But RBNZ track for March 2025 quarter is less than 5.75% which prima facie suggests a reduction somewhere in the March quarter.

And so on.

LikeLike

Fair point, altho I suspect on this occasion they haven’t engaged in the sort of normal smoothing (that would have been sensible), and thus the rates above 5.5% should be mainly seen as a probability (less than 1) of a OCR increase. Since few people actually expect an increase then to me it still makes sense to think in terms of the first easing being when the OCR track first drops below 5.5%. Apart from anything else, if they really did increase the OCR further in say November, it would be quite a quick turnaround to start cutting as soon as mid 2025 (would generally only happen that quickly if they realised they’d made a mistake). In 2007 we restarted a tightening cycle, in the face of surprisingly high inflation, and it took a full year before we then made the first cut.

LikeLike

The introduction of the Loan to Income restrictions of 6x and the relaxation of the LVR restrictions seem to suggest that the RBNZ’s interest rates are poised to drop which the RBNZ would have concerns that drop has the risk of reigniting the property market.

LikeLike