The Governor’s press release this morning, leaving the OCR unchanged, was no surprise.

But it continues to seem out of step with the data, and with his responsibilities under the Policy Targets Agreement. The statement has the feel of being written by someone who really really does not want to cut the OCR, but who won’t explain why. It is if the current level of the OCR were being treated as an end in itself, or being held up in pursuit of some other goal, rather than being a tool for influencing the (rather too low) medium-term rate of inflation.

Fortunately, the statement corrects what must have been a mis-step in John McDermott’s speech last week. Today the Governor states that:

It would be appropriate to lower the OCR if demand weakens, and wage and price-setting outcomes settle at levels lower than is consistent with the inflation target.

Last week, that criterion was expressed in terms of lower than the “target range”.

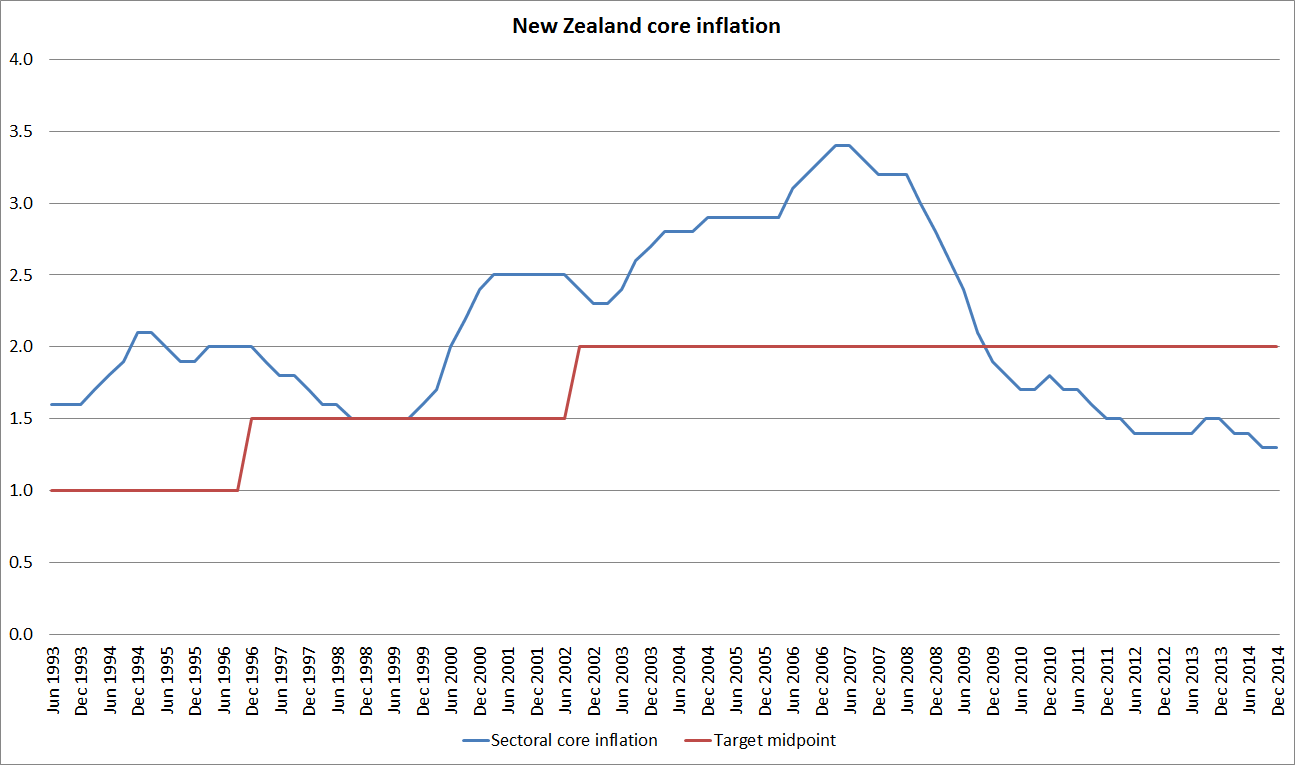

But there is no reference anywhere in the statement to the 2 per cent midpoint, even though the Governor and the Minister explicitly agreed that the midpoint should be the Bank’s focus. And wage and price-setting outcomes are already inconsistent with the target midpoint and have been now for some years. This statement offers no tangible basis for expecting that to change, just the limp observation that underlying inflation “is expected to pick-up gradually”. Why? When? What is about to change that will now reverse a slide in core inflation that has been underway, more or less continuously, since 2007? It has to be something more than just a belief that monetary policy is “stimulatory”.

Once again, the Governor anguishes about the exchange rate. I agree totally with the substance of his references to New Zealand’s long-term economic fundamentals and how out of step the exchange rate is with them (it was the heart of this paper I wrote for the Treasury-Reserve Bank forum on exchange rate issues in 2013). But……this is a press release about the nominal OCR, not about the real factors that shape New Zealand’s longer-term competitiveness. And while the Governor observes that “the appreciation in the exchange rate, while our key export prices have been falling, has been unwelcome”, he seems unwilling to take the obvious step in response. Exchange rates are largely influenced by expected relative risk-adjusted returns, broadly defined. When New Zealand interest rates have been rising while those in most of the rest of the world have been falling, and we have a Governor who appears very reluctant to cut those interest rates, it is hardly surprising that we end up with a cyclically strong exchange rate. Cutting the OCR won’t solve the long-term economic challenges: they are about real factors, not monetary policy. But a strong sense from the Bank that the OCR was heading back towards 2.5 per cent over the coming year, or perhaps even lower, would be likely to make a useful difference.

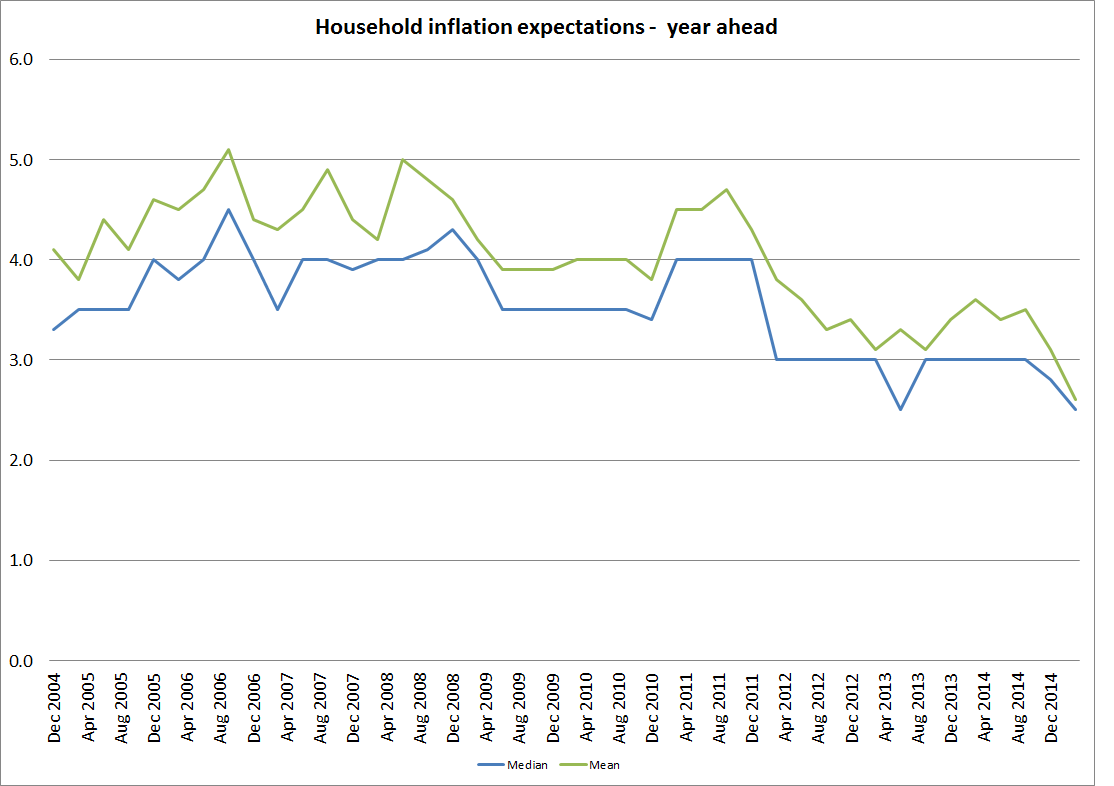

And why not do so? Core inflation is very low, the number of people unemployed (and underemployed) lingers uncomfortably high, inflation expectations are falling, farm incomes are falling, credit growth is pretty modest, and so on. So why not cut? Of course, no one can be totally certain that, with hindsight, cuts will prove to have been the right policy, but on the New Zealand and global data as they stand today – and without a compelling case to suggest the inflation picture is about to change materially – not doing so increasingly looks negligent. In time, it is the sort of stance that also risks further undermining public and political support for the broad monetary policy framework, and the Governor of the Bank’s powerful position within it.

The Bank’s take on the rest of the world, as reflected in the press release, is both puzzling and disconcerting. The Governor reiterates what appears to be one of his favourite lines, that trading partner growth is around its long-term average. This is true, but largely irrelevant. First, it simply reflects the fact that China is a more important trading partner than it was, and its growth rates are higher than those in our other trading partners. But even China is slowing, probably quite sharply. And commodity prices – a key way the rest of the world’s economy affects New Zealand – have fallen a lot.

In addition, in almost all of our trading partners – and in most countries that are not our trading partners – GDP remains well below pre-crisis trend levels. Not all of that is excess capacity, but a significant proportion is likely to be. Again, the Governor makes much of the low interest rates abroad, but seems not to put much weight on why those rates are so low. There are all sorts of idiosyncratic factors in individual countries, but across the world interest rates are low and falling not because central banks have arbitrarily put them there (it isn’t some “monetary policy shock” in the jargon), but because markets and central banks both judge that underlying demand and inflation pressures require interest rates be at least as low as they are. That is a very worrying perspective on the world, not a comforting one.

Finally, the Reserve Bank likes to claim that it is highly transparent, citing for example its scores in papers like this one. But in many of the more transparent central bank we could look forward to the minutes of the meetings that led to the decision being published. In some central banks, even the range of views is extensively outlined. The Governor has noted he now makes his OCR decision in the so-called Governing Committee, with his three senior colleagues. But we do not have access to the minutes of these meetings, even with a lag, or to a summary of the advice provided to the Governor by his wider group of advisers, including the external advisers. Transparency and open government are not just about announcing and explaining final decisions, but about the process whereby those decisions were reached. Some other New Zealand government agencies are quite good at pro-active release of background material (for example, papers leading up to the Budget). It is a model the Reserve Bank could look at emulating. In the next few days, I am expecting a response from the Reserve Bank to my OIA request for background papers to an OCR decision from 10 years ago. It will be interesting to see how they interpret the Act is deciding how to respond.