On Friday morning I picked up my copy of The Post to find on the front page a story clearly handed to Stuff’s political editor Luke Malpass, about a shiny new intervention that ministers were to announce later that morning to help out residential property developers. It was, we were told, going to offer free downside price/liquidity insurance to large and established property developers. It would be sold as strictly “time-limited” except that there would, in fact, be no time limit specified.

My reaction on Twittter was “What…….” and it brought to mind that old jeer about business-friendly (as opposed to pro-market) governments and an enthusiasm among some of their supporters to “capitalise the gains and socialise the losses”. Little did we imagine that this would in fact become declared and intended policy of this National/ACT/NZ First government (not in the midst of a crisis, where sometimes these things happen, but as a whole new policy tool). I’m not generally an ACT fan, but……you have to wonder what the point of an allegedly pro-market anti-intervention libertarian party is if they wave things like this scheme through Cabinet (and not even their backbenchers have issued statements of disapproval, they being rather freer than ministers).

Malpass’s report was quickly proved accurate, with the announcement later that morning by Chris Bishop and Chris Penk (ministers of housing and of building and construction respectively) of the Residential Development Underwrite scheme.

The fact that it appeared to replace but considerably extend schemes in place under Labour was not a point in its favour

Funding for the RDU will be redirected from unused funding from the Kiwibuild and BuildReady Development Pathway programmes. Both of these programmes are now closed to new applications.

This government (rightly) having made much of inheriting a large structural fiscal deficit, and wanting to get government out of business, instead jump in boots and all. And all apparently on the basis that a couple of Cabinet ministers and their MHUD officials know better than the market what should be built when, where, and by whom, and thus who will win the benevolence of the free government underwrite.

There was more information on the MHUD website, but it was no more reassuring. There was no sign of any analytical framework behind any of it (no analysis at all, let alone anything serious or rigorous. of market failures or any sort of cost-benefit analysis or risk assessment). In fact, there was a distinct sense of something that had been rushed out. Some property developers had presumably been bending the ears of ministers. As the Herald put it “the government is riding to the rescue of stressed property developers”, in a distinctly picking-winners approach to the recession. Plenty of people and firms will have undergone huge stress in the last couple of years, as inflation was squeezed back out of the system. It was and is a necessary adjustment. But most apparently didn’t enjoy the favour of ministers.

And will no doubt do so again. In one article on Friday, Bishop was quoted thus

Bishop said the scheme wouldn’t be in place forever and Cabinet would make decisions about when to “turn it on and off” depending on demand and construction activity.

So that would no predictable and rigorous framework, but rather a great deal of trust in ministers’ ability to forecast construction cycles and housing demand, or to respond to pressures of the electoral cycle or developers bending their ears. Good regulation – like a good tax system – is stable and predictable, not turned on or off at the whim of ministers. This is poor policy, done poorly. And isn’t it simply dishonest for a government department to repeat ministerial spin about the intervention being “time-limited” (and MHUD does exactly that upfront) when there is no time limit at all? After all, in the grand scheme of things every policy intervention will eventually be altered/amended.

In essence what the scheme involves:

- the government will guarantee to purchase at an agreed (in advance) price houses that don’t sell at an (approved) market price within an approved period of time,

- only large-scale developers will be eligible for this assistance, preferably those building in Auckland, Wellington, Christchurch, Hamilton, and Tauranga [a little surprised Queenstown wasn’t on the favoured list),

- no fee will be charged for this put option that is being granted to the developers

The rationale appears to be that banks and other potential lenders aren’t sufficiently willing to take risks on this projects, even at high fees/interest margins, but……government knows better/best. Quite why we are supposed to believe this self-delusion (ministers and officials falling for it is perhaps more understandable – if no more excusable – given the nature of their incentives) is never made clear. Minister are, it appears, blessed with some special insight into the state of the economy and the timing/speed of the recovery, and instead of just (say) publishing that analysis, they prefer to give handouts (and that is what free price/liquidity insurance is) to developers.

In the MHUD document there is this statement upfront

The secondary objective never seems to get another mention, but the ‘primary objective” is almost worse, for being functionally meaningless. You minimise the cost and risk to the Crown by simply not offering free insurance, and if you must offer such insurance you should do so with a disciplined and transparent model (to, for example, estimate the economic price of the option). But there is nothing of that sort in any of the MHUD material, just a lot of mention of the (extensive) discretion afforded to officials, of whom we may be left wondering both what their expertise is and what their incentives are. Why would we back them to make better choices than financial market participants? And as for “maximising housing supply”, there seems to be no analytical framework there either, including around incentives on developers (who will, of course, prefer free insurance and can be expected to try to game the rules). Will there be any material impact on supply, will any impact be any more than timing, and how will MHUD rigorously evaluate claims put to them by developers? Oh, and isn’t developers finding themselves with overhangs of houses and land part of the way that much lower house prices actually come about?

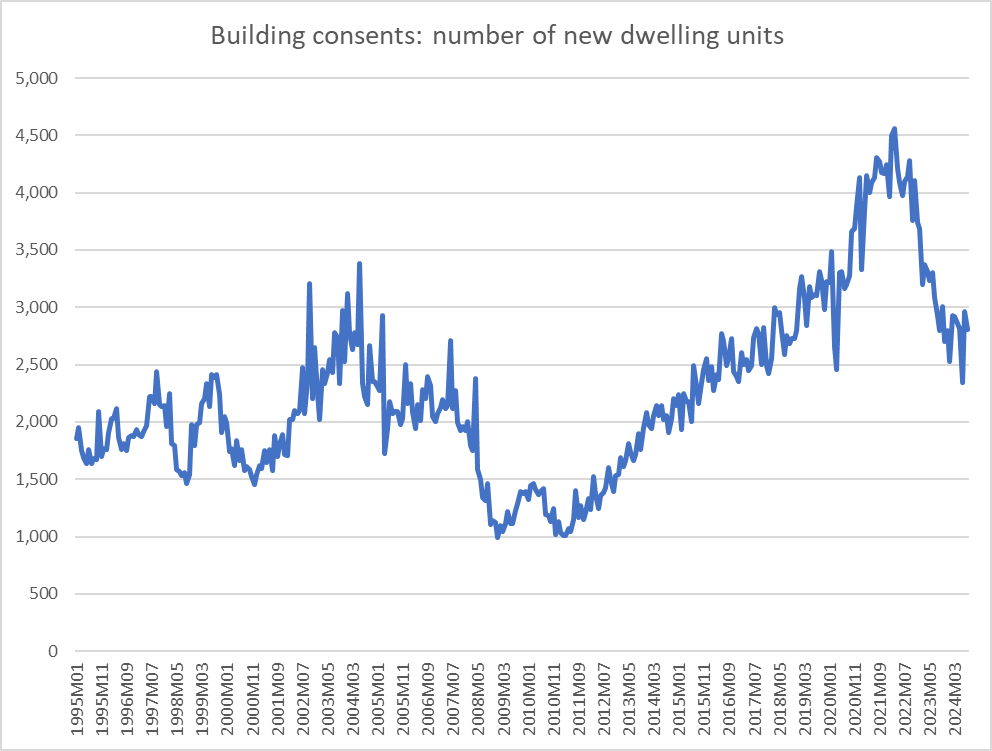

It is possible the scheme won’t end up being hugely costly. After all, house prices might take off again as interest rates fall. Or officials might err on the very cautious side and very few underwrite grants might be made (or at such deep discounts that the real insurance cost is cheap). But there is just no good or compelling analytical foundation for any sort of intervention of this sort (none provided, none readily conceivable). Even the business cycle argument seems rather flakey. Ministers seem to lament the cyclicality of residential construction (globally, it tends to be one of the most cyclically variable components of GDP), but when they lament the state of the industry, they don’t mention that new residential dwelling consents are still running around twice the level at the trough of the 2008/09 recesssion.

There is also talk about helping to get the cyclical economic recovery underway. Pretty much all the arguments against using fiscal policy for that purpose – I’ve outlined them here repeatedly – apply at least as much to discretionary sector-specific interventions like the Residential Development Underwrite. And, of course, were the Reserve Bank to regard this scheme as being likely to make a material difference it should, all else equal, make them more reluctant to, with less scope to, cut the OCR a lot further.

It is a rather sad reflection of how the quality of New Zealand policymaking has fallen. Perhaps we should be grateful that exchange rate cycles aren’t what they were – and that past governments were less prone to scheme like this – or who knows what sort of free insurance the government would be dreaming up for exporters.

Who knows what the relevant government agencies thought of this scheme. I’ve lodged OIA requests and am particularly interested in any analysis and advice from The Treasury and the Ministry for Regulation.