Richard Prebble, once upon a time an Associate Minister of Finance, has a column in the Herald this morning which he devotes to the twin causes of bashing the Reserve Bank and singing the praises of an interesting nowcasting data project run by a Massey academic, GDP Live. I’m quite partial to a fairly critical approach to today’s Reserve Bank of New Zealand (even had a post in mind on the very subject for today), but I don’t find Prebble’s stick to beat them with – GDP Live – particularly persuasive on this occasion.

This was the abstract from the authors’ 2018 paper (on the website at the link above) on what they are doing

It is great to see people doing this sort of stuff and making the results available routinely and accessibly. It is particularly good to see economics academics in New Zealand doing some policy-relevant New Zealand focused stuff. They publish daily updates of quarterly estimates of several macro variables

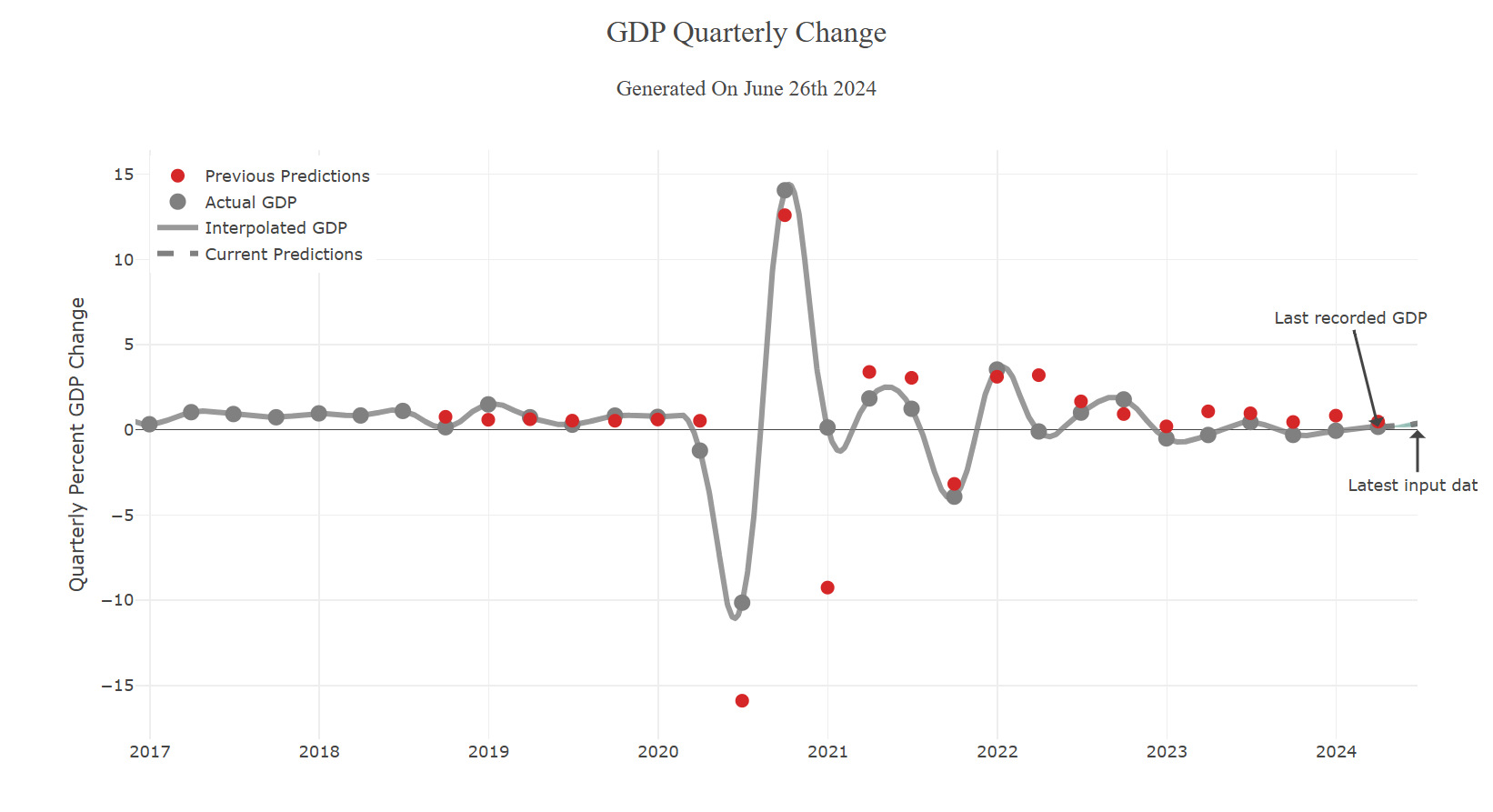

Prebble’s focus was on the quarterly change in (production) GDP numbers. Here is the GDP-Live chart for that variable

If you just give it a quick glance it doesn’t look too bad – those “previous predictions” don’t look too consistently different from the grey dots, the latest vintage of SNZ actual data (note that “latest vintage” is not innocuous, since recently published outcomes are often revised for several years as more data come available to SNZ. And while “true” GDP growth is probably what should be being aimed for, it is less use than “first release” GDP data unless users can be confident that GDP-Live is producing really quite reliable estimates of the final number that won’t settle for several years).

Here is how the “previous predictions” (red dots) are described

But scale is a bit of a problem in just eyeballing the chart. There were those two very very dramatic quarters around the first Covid lockdown, which push the scale out so far that it is very difficult to meaningfully eyeball any of the other data.

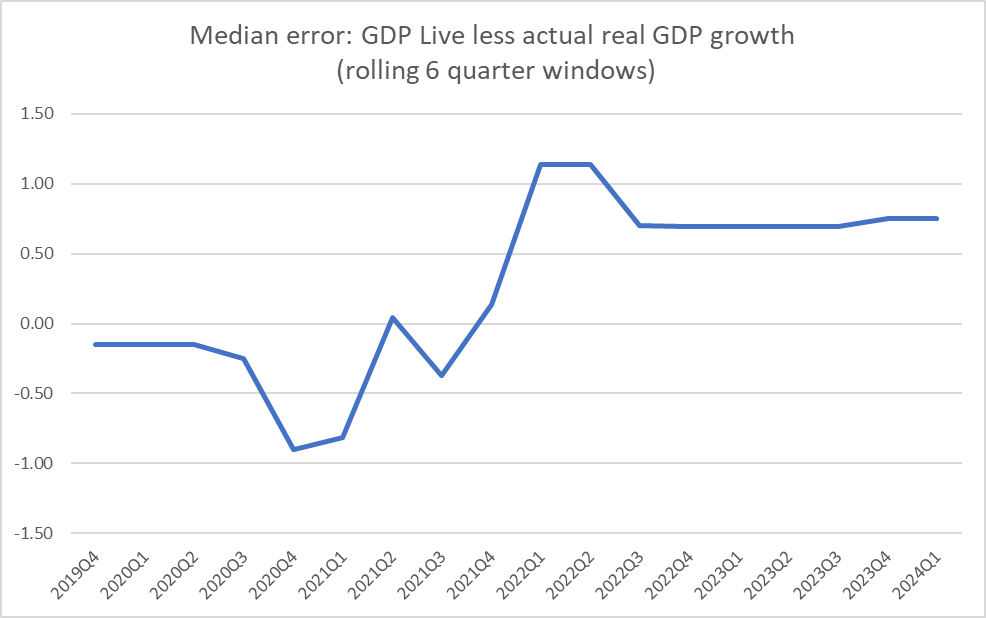

So I laboriously transcribed the red dot numbers into a spreadsheet and compared them against the latest vintage SNZ data. How accurate were the red-dot average predictions?

Well, not very at all (so far). Over the almost six years of observations the median gap between the red dot and the current SNZ estimate for each quarter has been 0.54 per cent (specifically, in a typical quarter the model has overestimated quarterly GDP growth by 0.54 per cent).

That isn’t great, but it also isn’t as if the errors have been predictably all on one side. For the first half of the sample – even through those really volatile Covid quarters – there wasn’t much of a bias at all. But in the last couple of years, the bias has been large and (it appears) quite persistent.

I did that chart using six-quarter rolling windows (slightly arbitrarily chosen horizon, but to capture some variation in a quite limited total sample), but perhaps as concerning is that in every single one of the last six quarters GDP-Live has materially overpredicted (the current vintage of) quarterly real production GDP growth. You can see this on the GDP-Live chart itself above, but the Covid scale issue makes those gaps look quite small. They aren’t. In fact, the smallest gap (smallest overstatement) is for the most recent (March quarter) numbers, but (a) at 0.32 per cent it is still far from small, and (b) who knows where the final SNZ number for that quarter will end up. (Not to ignore the fact that GDP(P) is itself only one proxy of “true” GDP, and GDP-Live doesn’t attempt to model GDP(E)).

The point of this post is NOT to bag the GDP-Live efforts. I’m only too keen on seeing more and better analysis and tools that make for better commentary and macro policy in New Zealand.

It also isn’t impossible that the GDP-Live estimates are less bad than RBNZ ones. I’m not going back and opening up 23 past MPS to get all the RB projections, but I did have look at those last six quarters that GDP-Live had done badly on. Straight comparisons aren’t easy.

As I understand GDP-Live they do forecasts every day during the quarter and the red dot is the average of 90 of them. It doesn’t update its estimates in the 10-11 weeks we have to wait before SNZ finally publishes their numbers. The Reserve Bank, by contrast, publishes forecasts only each quarter. The first quarter they are forecasting is actually the previous calendar quarter (so in the May MPS their first forecast/estimate was for the March quarter). By then, they might reasonably be thought to have some more data to hand than the GDP-Live model uses. On the other hand, they also publish in the May MPS a forecast for GDP growth in the June quarter. The Bank’s projections are finalised only about 7 weeks into the quarter so at that they have materially less data than GDP-Live has when its June quarter red dot is finalised in a day or two from now. The simplest comparison might then be to average the Bank’s Feb MPS and May MPS forecasts for the March quarter (the most recent hard SNZ estimates we have).

Over that period, the Reserve Bank also tended to overpredict (in five of the six quarters), but the median error (0.19 per cent per quarter) was materially less than GDP-Live’s error.

Should we put very much weight on any of this? I wouldn’t. The tool is fairly new, the sample is short (and the last six quarters just one – not immaterial – episode). Moreover, I am quite sure that the Reserve Bank is using a range of statistical models to do their (as we used to call them) “monitoring quarter” GDP growth estimates. It would be surprising if they hadn’t taken a look at what GDP-Live might offer, and particularly at such questions as to when and in what circumstances it might have done less badly than their other models or techniques. So the point of this post isn’t to bag GDP-Live or to praise the Reserve Bank, but more to caution readers, and potential readers, of Richard Prebble’s column.

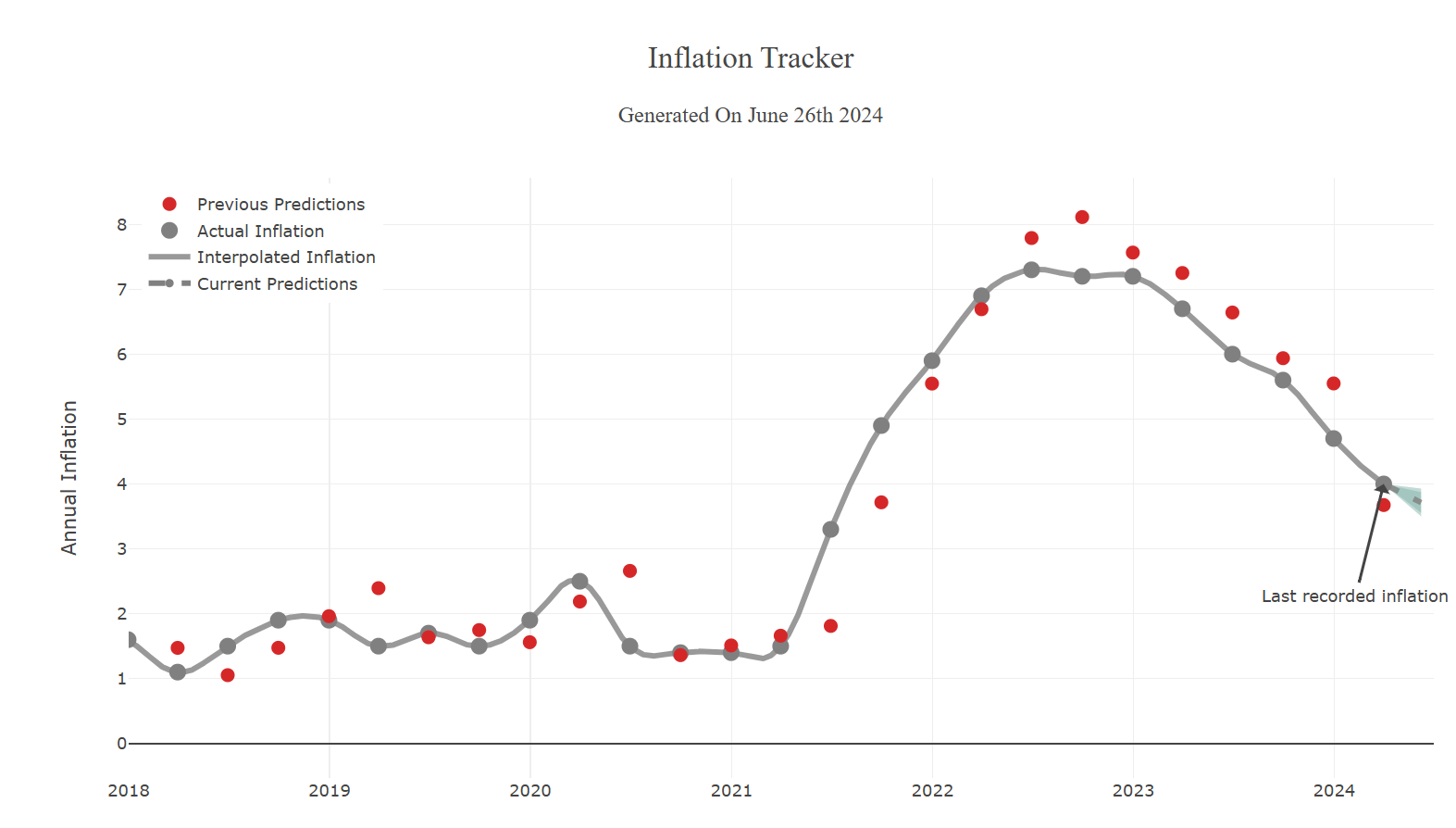

GDP-Live also does real-time inflation forecasts (and here we don’t have to worry about ongoing data revisions). Unfortunately, the model doesn’t seem to have done very well when we would have valued it most, in the worst outbreak of inflation in decades (and now the abatement of inflation). In both cases, it has lagged actual CPI data (rising and falling a quarter or so later, and reaching a peak that was higher than the actual).

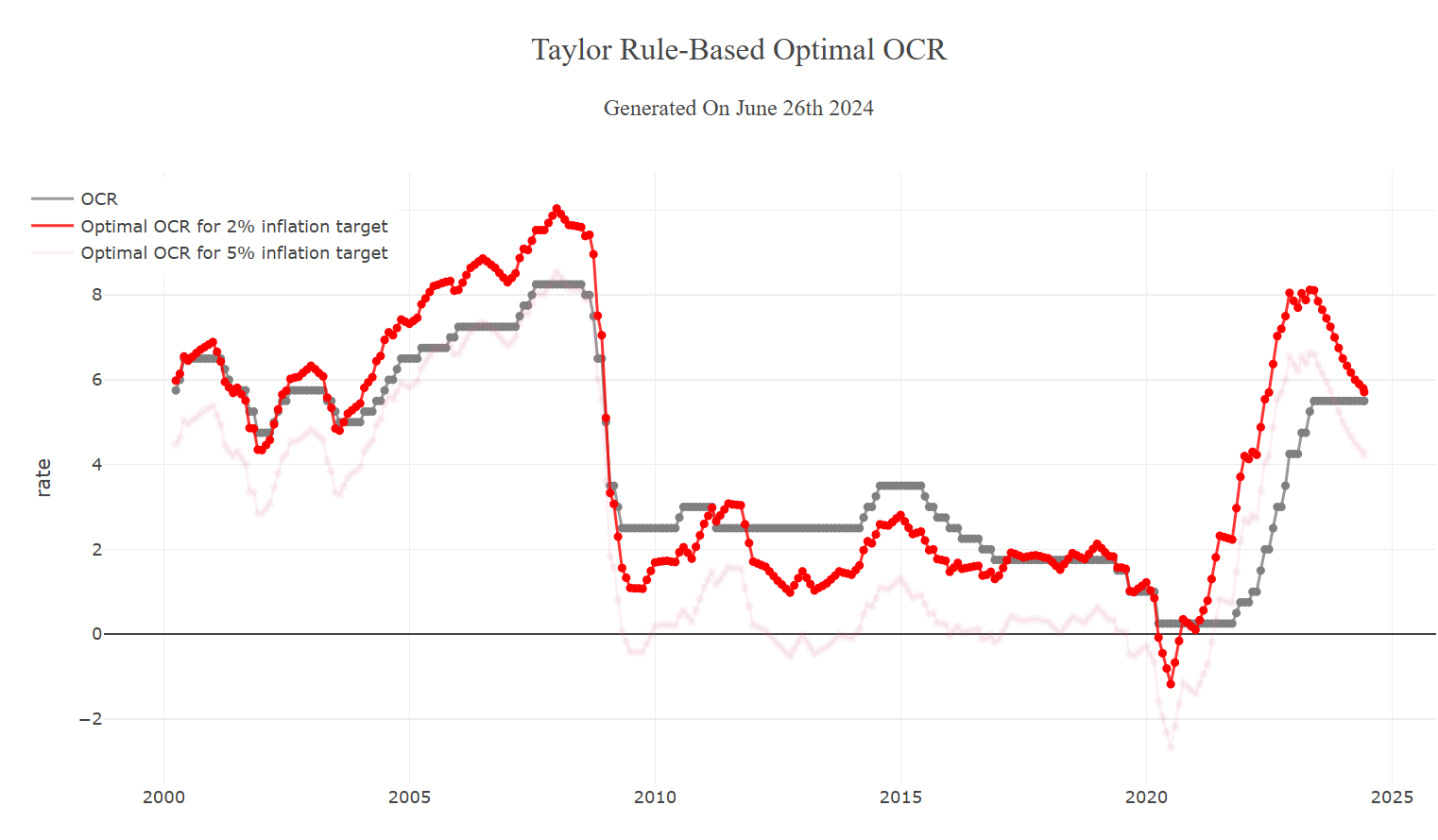

They also do a Taylor-rule based guide to what the OCR should be (over a longer period). Since one of the key uncertainties of the last 15 years has been what is, and what is happening to, the neutral real interest rate I’m sceptical of Taylor rule approaches adding much marginal value. At present, I see little external basis for thinking that the OCR should have been set at 8 per cent last June (rather than the 5.5 per cent actual), and although I was an OCRAG hawk in late 2007 – so quite like the red line being above the grey line then – I’m also sceptical that an OCR of 10 per cent then, or even 9.4 per cent by July 2008, was really what the situation called for.

But people should keep an eye on these tools, as just one piece of data to add to the analytical mill.

There was a big problem for GDP Live associated with past growth data when StatsNZ revised a whole chunk of their previous data at the end of last year. Since GDP Live’s algorithm was trained on StatsNZ official data, the model then had to “unlearn” its previous work when StatsNZ made massive revisions. That’s not GDP Live’s fault, of course, and it explains some of the deviations you might spot over the past few years. But Christoph Schumacher will be able to tell you more about that. It was a bit of a nightmare scenario for him and his team.

LikeLike

Thanks Oliver. Makes sense, altho since the annual GDP revisions are a regular event (altho the size varies from year to year of course), it is something they will have to find a way to work with in a timely manner.

LikeLike

Yes, indeed. The problem last year also that it wasn’t just a marginal correction of the data but it all added up quite a bit over the time period. And then the whole machine learning model has to be reset with terabytes of data. As I said, a small nightmare for Christoph’s team, but they seem to have updated it now.

LikeLike

Hi Michael,

Thanks for your detailed feedback. You are right, there is room for improvement. GDPLive is a reasonably new tool and we simply need more data and official values to train the algorithms.

Importantly, when Statistics New Zealand downgraded two years of official values, our forecasts got negatively impacted. We didn’t adjust our values (red dots) but left them as they were which meant that for two years, GDPLive was trained with too optimistic values and thus produced too optimistic forecasts. Given that we didn’t change our values (red dots) but downgraded the official values (grey dots), the gap between the two increased with no fault of our own. This is why you see the consistent overestimation as shown in your graph.

Yes you are absolutely right, we need to find a way dealing with these adjustments but the last round of downgrades over a two-year period were very significant and were unexpected. We are working on it.

Our inflation tracker is very new and was released in November 2022 so again, we need more data. We realised that we were overestimating inflation and will release a revised inflation tracker on the 15. July. The new tracker will include new input data which we hope will fix some of the issues we still have.

GDPLive is, above all, a research project to showcase what is possible with cutting edge technology. Your feedback will help us improve GDPLive.

We are trying to fill a huge information gap and it is challenging. We often hear that GDP is the health measure of an economy. Imagine you go to your doctor and get told that 6 months ago you were healthy. That is good news but what you really want to know is how healthy you are right now! GDPLive tries to provide this answer and we are happy to work with our government and RBNZ to make it even better.

LikeLike

Thanks for those comments Christoph. I’m entirely sympathetic with what you are aiming to do (and with the push for more frequent, less badly lagged, publication of key official data (notably the CPI and unemployment rate). Getting our read of the economy less wrong has real and tangible benefits to offer.

LikeLike

I’d love to see the thing trained on beyond-revision data (and the early estimates) to project both the first-announced GDP figure and the final revised figure.

If current projections are closer to final results, they’ll always look bad when compared to the first-announced quarterly figures. But it’s the settled figure that winds up mattering right?

LikeLike

Would be good to see estimates of both, as you say, altho I guess the model would have to identify an (as yet unknown) systematic reason for the revisions.

As I noted in my post, i think in an ideal world one is aiming mostly for “true GDP” (altho then I’d also like to see it done on say an average of the two real GDP series), but unless the model is so good that its estimate picks the final GDP numbers (years down the track) to a very high degree of accuracy, it is likely to be a bit of a voice crying in the wilderness because markets, media, politicians, and prob even the RB would focus primarily on the early published numbers. There are likely to be more customers for an accurate read on the initial number than for one on the final number.

LikeLike

As a interested but untrained observer doesn’t the RBNZ and Stats NZ calculation of inflation include an element of hedonic pricing. Surely this wouldn’t be used by GDP Live and therefore could be more accurate. I remain very sceptical in the use of hedonic pricing.

LikeLike

They will be trying to forecast the CPI as actually constructed.

On hedonics, I guess there is reason for scepticism about specific estimates but certainty that making no adjustments would be to overstate inflation.

LikeLike