Yesterday’s post was a bit discursive. Sometimes writing things down helps me sort out what I think, and sometimes that takes space.

Today, a few more numbers to support the story.

I’m going to focus on what the experts in the macroeconomic agencies (Treasury and Reserve Bank) were thinking in late 2020, and contrast that with the most recent published forecasts. The implicit model of inflation that underpins this is that even if the full effects of monetary policy probably take 6-8 quarters to appear in (core) inflation, a year’s lead time is plenty enough to have begun to make inroads.

Forecasts – and fiscal numbers – in mid 2020 were, inevitably all over the place. But by November 2020 (the Bank published its MPS in November, and the Treasury will have finalised the HYEFU numbers in November) things had settled down again, and the projections and forecasts were able to be made – amid considerable uncertainty – with a little more confidence. And the government was able to take a clearer view on fiscal policy. The Treasury economic forecasts in the 2020 HYEFU incorporated the future government fiscal policy intentions conveyed to them by the Minister of Finance. The Reserve Bank’s forecasts did not directly incorporate those updated fiscal numbers, but…..the Reserve Bank and The Treasury were working closely together, the Secretary to the Treasury was a non-voting member of the Monetary Policy Committee, and so on. And, as we shall see, the Bank’s key macroeconomic forecasts weren’t dramatically different from Treasury’s.

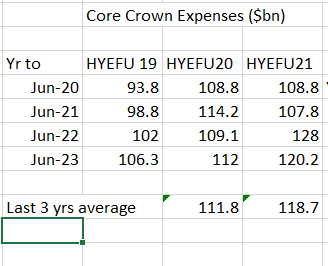

The National Party has focused a lot of its critique on government spending. Here are the core Crown expenses numbers from three successive HYEFUs.

From the last pre-Covid projections there was a big increase in planned spending. But by HYEFU 2020 – 15 months ago – Treasury already knew about the bulk of that and included it in their macro forecasts. By HYEFU 2021 the average annual spending for the last three years had increased further. But so had the price level – and quite a bit of government spending is formally (and some informally) indexed.

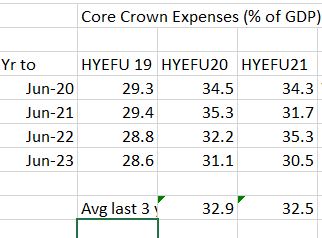

Here are the same numbers expressed as a share of GDP.

By HYEFU 2021 the government’s spending plans for those last three years averaged a smaller share of GDP than Treasury had thought they would be a year earlier. (The numbers bounce around from year to year with, mainly, the uncertain timing of lockdowns etc).

There are two sides to any fiscal outcomes – spending and revenue. The government has been raising tax rates consciously and by allowing fiscal drag to work, such that tax revenue as a share of GDP, even later in the forecasts, is higher than The Treasury thought in November 2020. And here are the fiscal balance comparisons.

Average fiscal deficits – a mix of structural and automatic stabiliser factors – are now expected to be smaller (all else equal, less pressure on demand) than was expected in late 2020.

Fiscal policy just hasn’t changed very much since late 2020, and the fiscal intentions of the government then were already in the macro forecasts. Had those macro forecasts suggested something nastily inflationary, perhaps the government could have chosen to rethink.

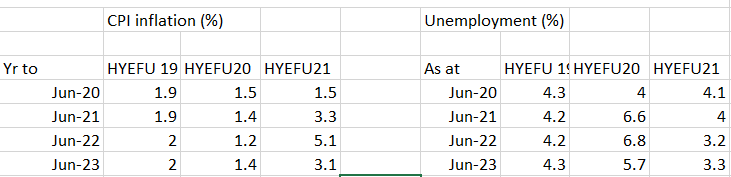

But they didn’t. Here are the inflation and unemployment forecasts from successive HYEFUs.

In late 2020, The Treasury told us (and ministers) that they expected to hang around the bottom end of the target range for the following three years, with unemployment lingering at what should have been uncomfortably high levels. If anything, on those numbers, more macroeconomic stimulus might reasonably have been thought warranted.

There were huge forecasting mistakes, even given a fiscal policy stance that didn’t change much and was well-flagged.

That was The Treasury. But the Reserve Bank and its MPC are charged with keeping inflation near 2 per cent, and doing what they can to keep unemployment as low as possible. For them, fiscal policy is largely something taken as given, but incorporated into the forecasts.

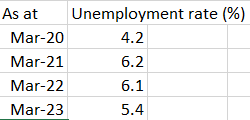

Their (November 2020_ unemployment rate forecasts were a bit less pessimistic than The Treasury’s, but still proved to be miles off. This is what they were picking.

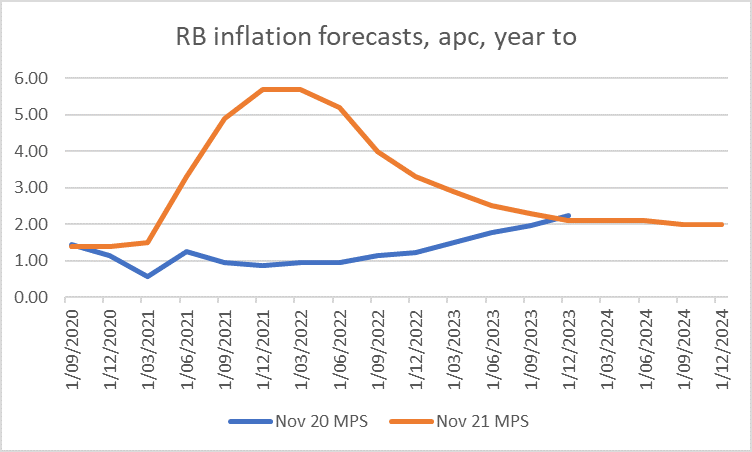

And here were the Bank’s November 2020 inflation forecasts, alongside their most recent forecasts.

Not only were their forecasts for the first couple of years even lower than The Treasury’s, but even two years ahead their core inflation view was barely above 1 per cent. (The Bank forecasts headline inflation rather than a core measure, but over a horizon as long as two years ahead neither the Bank nor anyone else has any useful information on the things that may eventually put a temporary wedge between core and headline.) All these forecasts included something very much akin to government fiscal policy as it now stands. Seeing those numbers, the government might also reasonably have thought that more macroeconomic stimulus was warranted.

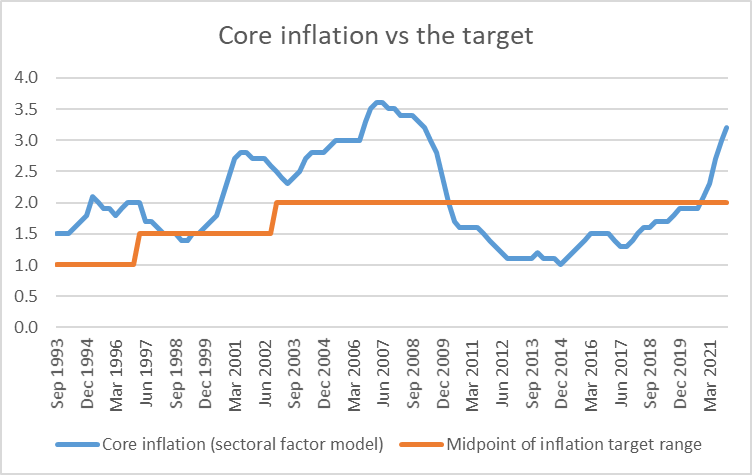

As a reminder the best measure of core inflation – the bit that domestic macro policy should shape/drive – is currently at 3.2 per cent.

There were really huge macroeconomic forecasting mistakes made by both the Reserve Bank and The Treasury, and – so it is now clear – policy mistakes made by the Bank/MPC. You might think some of those mistakes are pardonable – highly unsettled and uncertain times, not dissimilar surprises in other countries etc – and I’m not here going to take a particular view.

But of all the things Treasury and the Bank had to allow for in their forecasts, fiscal policy – wise or not, partly wasteful or not – just wasn’t one of the big unknowns, and hasn’t changed markedly in the period after those (quite erroneous) late 2020 macro forecasts were being done.

I guess one can always argue that if fiscal policy had subsequently been tightened, inflation would have been a bit lower. But Parliament decided that inflation – keeping it to target – is the Reserve Bank’s job. The government bears ultimate responsibility for how the Bank operates in carrying out that mandate – the Minister has veto rights on all the key appointees (and directly appoints some), dismissal powers, and the moral suasion weight of his office – but that is about monetary policy, not fiscal policy or government spending,

Reblogged this on Utopia, you are standing in it!.

LikeLike

A little bit on a specific point: with retail mortgage rates moving higher and a sizable stock of mortgage debt up for renewal, the crimp on NZ household demand could, arguably, happen well ahead of an OCR increase? (and factoring the current hit to real incomes via petrol pumps etc). Is 12-18 months lag a good rule of thumb or is ‘this time different’…

LikeLike

Yes, it is a fair point, and one the RB likes to make. Of course, in all tightening cycles fixed rates tend to move ahead of the OCR. And today’s inflation expectations survey results already implicitly factor in both the fixed rate rises we’ve already seen and the OCR increases respondents expect over the coming year. And of course the economy ran so hot last year that we don’t just need household demand growth to slow back to normal, but to undershoot (perhaps materially) to get core inflation back down again. Perhaps it will happen of its own accord – I’m not one of those making big calls about where the OCR will end up, just looking at the immediate situation and thinking we needed (and now need) quite a bit more tightening early.

LikeLike

Thanks. Just read there are almost seven sequential rate hikes priced into NZ money markets: that seems nuts – not many things are linear, especially a future economy…..!!

LikeLike

I think the Fed went more than a dozen times in a row…so possible, but one should be careful about putting much money on such a view.

LikeLike

One can forgive the forecasting errors ( after all they were not alone), and one may then rationalise the policy mistakes (expensive as they are), but to seemingly have not done any requisite/robust analytical work would be the most egregious aspect of all of this.

LikeLike

it is the overall Orr/RB story that should be so damning: bad forecasts, poor policy, weak analysis, lack of transparency, massive losses, the exodus of top staff, the dodgy new appointees, and so on.

But apparently of no concern to MoF.

LikeLike