Bernard Hickey, of Newsroom, had a passionate piece out the other day lamenting the fiscal conservatism of the Prime Minister and the Minister of Finance, and calling for a large increase in New Zealand government net indebtedness (albeit over “the next decade or two”) under the ambit of something he calls the “Re-Engineering New Zealand” project.

It was a curious article because it seemed to throw together a variety of different things that don’t necessarily belong together: the cyclical on the one hand (potential limits of monetary policy in the next recession, at least on current technologies) and long-term structural issues (climate change, skills, productivity, infrastructure, housing etc) on the other.

On the cyclical side, Hickey’s case isn’t helped by the claim that monetary policy “did little to solve…the short term…problems facing the economy”, which simply has to be not true. Unemployment rates, which shot up sharply during the last recession are as low as, or lower than, they were just prior to that recession in most advanced countries (not too far away even in New Zealand). I wouldn’t recommend the alternative – places like Spain, Greece, and Italy that had no nation-specific monetary policy open to them. Central banks were often too slow to ease, and too often looking towards the next tightening (see NZ with two lots of pre-emptive, soon-reversed, tightenings) but monetary policy worked when it was embraced and given a chance.

But, of course, in many of those countries the limits of conventional monetary policy were reached, which slowed the recovery in some countries. In New Zealand and Australia the limits weren’t reached, but as we head towards the next severe downturn – whenever it is – almost every advanced country now needs to be planning on the likelihood of monetary policy reaching its limits (on current laws and technologies). There are monetary ways through that obstacle – which I’ve been drawing attention to here for years – although for reasons not entirely clear central banks globally have been reluctant to embrace those sorts of options. If central banks won’t do anything to free-up monetary policy leeway, then it seems quite likely to me that in the next recession there will be significant discretionary fiscal stimulus – if politicians are not totally indifferent to the plight of the unemployed.

Since we are not now in a recession in New Zealand (well, we may be, but not a single forecaster is suggesting we yet are), and since conventional monetary policy has probably 175 basis points of leeway to go – and the real exchange rate is still so high – now isn’t the time for rushing to temporary counter-cyclical fiscal stimulus. Do it now – on the promise of being temporary – and you might well find that when it was actually needed the political pressure was already mounting to tighten up again, to unwind the stimulus, just when it might do some good. It was, after all, the Governor the other day who was openly worrying about additional government spending now either crowding out private sector activity, or being unable to be implemented because private sector activity crowded it out.

I’m sure Hickey is quite sincere about his cyclical point – and the next serious downturn globally is going to be very tough to get through for many countries – but his real argument seems to be a structural one. He is a bigger-government man, and one who favours much larger government debt (the two are, of course, separate issues). He wants governments that do more, and seems pretty confident that he knows what they should spend our money on (and is quite dismissive of anyone complaining about potentially injudicious use of public money). Interest rates are low on his telling primarily because of quantitative easing – a strange story to tell in a country where there has been no quantitative easing and yet where five year real government bond rates are now zero or slightly negative – and thus represent a windfall opportunity for borrowers.

Here is his list of what needs doing

Productivity, which is the only thing that matters in the long run, is slowing globally and has been stagnant here for more than five years. Housing affordability is collapsing in most developed countries because of rising house prices, restrictions on new developments and, tragically, falling interest rates.

Real climate change action is scarce because it requires massive public investment in public transport and new medium density housing close to city centres. Our skills, economies and cities need re-engineering massively if we’re going to restart productivity, make housing affordable for the young and poor and achieve net zero emissions by 2050.

It is a global problem, but even more acute here because we have among the worst housing affordability, productivity and climate change emissions figures in the world.

Massive investment in transport, health and housing infrastructure, education, workplace skills, business technology and research and development is required everywhere, but the central and local governments who are the only ones with the authority and balance sheets to do it are frozen in the headlights of politics and 30 years of austerity and smaller Government dogma.

And yet one was left wondering whether there might not be at least some connection between weak productivity growth and low interest rates – firms just don’t see the profitable opportunities and so aren’t looking to invest heavily. And if – as is so – regulatory restrictions limit land use and housebuilding why not get on and get government out of the way: remove or greatly ease up those restrictions (as some in the Labour Party suggested they might) and let the private sector get on with building the sorts of houses people would prefer when they are free to choose (rather than the sort some experts might prefer them to adopt).

Quite how this proposed large scale government investment was going to solve the productivity problems wasn’t clear – when private firms aren’t investing it has the feel of the old line about “fools rush in where angels fear to tread”. We’ve been that before in New Zealand – not that long ago with the Think Big programme. And – all else equal- big government investment programmes will push real interest rates and the real exchange rate further against the prospects of large outward-oriented private sector investment. Perhaps it might be helpful to see some robust empirical evidence or argumentation about the past ability to New Zealand governments to do these sorts of projects wisely and well, in ways that make us consistently better off.

And I’m always uneasy when people suggest that the relevant cost of capital is the borrowing rate on (even the longest-term) government debt. It isn’t. The cost of equity has to be factored in, and just because the government doesn’t have a share price doesn’t the issue less relevant. When the government undertakes projects it is using your money and mine to do so – either actual (already taken) or potential (the power to increase taxes whenever it likes). No commercial operation is going to be undertaking projects that seek a zero or one per cent real rate of return – even if they can raise at that price – and the standard Treasury advice, which I endorse, is that governments should not do so either. Given that the incentives on the governments to get things right are relatively weak, and the disciplines when they fail are weaker still, I’d argue that the required rate of return on government projects should be higher than those on a comparable private project. The relevant hurdle rates are lower than they were, but the cost of capital is still by no means trivial.

Hickey makes quite a play of a claim that the entire New Zealand political and official class is still living under the shadow of the potential double credit-rating downgrade in 1991. I don’t fully buy that story. It isn’t that long – how soon we forget – since people used to talk a lot about the desirability of the government running a low level of debt as some of counter-balance to the large negative net international investment position (ours still among the more negative in the advanced world), in a country with a fairly modest rate of national savings. Sure, there was a credit-rating dimension to that story, but it wasn’t the whole story by any means. Perhaps one can run some sort of over-savings story in places like the Netherlands or Germany (or Singapore) – and some might even find the argument for more government debt in those places persuasive – but this is New Zealand we are talking about. Savings rate haven’t suddenly gone stratospheric, and – low as our interest rates are now in absolute terms – the implied long-term forward rates are still higher than those anywhere else in the advanced world (while, as Hickey notes, our productivity growth record is terrible). And don’t forget the argument that if you run as pay-as-you-go age pension system – something most New Zealanders support – there is a good argument for also aiming to keep net government debt lower than one might find in other countries with different state-sponsored retirement income systems.

None of this is to suggest that the world would come to end if, instead of the current level of net general government financial liabilities (about zero on the OECD measure, and a little above the median advanced country rated AAA by Moody’s) we had net public 20 percentage points of GDP higher. It wouldn’t. All else equal, interest rates would be a little higher. But, equally, we can only say that we would be better off by doing so with some really hard-headed realistic analysis of the sorts of specific projects people would propose to use the debt for. I’m sure there would be beneficial projects – as there are daft and costly ones that happen now – but across the gamut it is as well to be very cautious. We’ve been this way before.

(As an alternative we could look at getting out of the way of private investment: freeing-up urban land use, foreign investment law, resource management act constraints, prohibitions on GE, prohibitions on offshore oil and gas drilling, and lowering our company tax rate which – from a foreign investor perspective – is among the highest in the advanced world. And here I’m not even going to my story on immigration: since short-term demand effects of immigration outweigh the short-term supply effects even I would be wary of large cuts to immigration right now – helpful as they would be in the longer–term.)

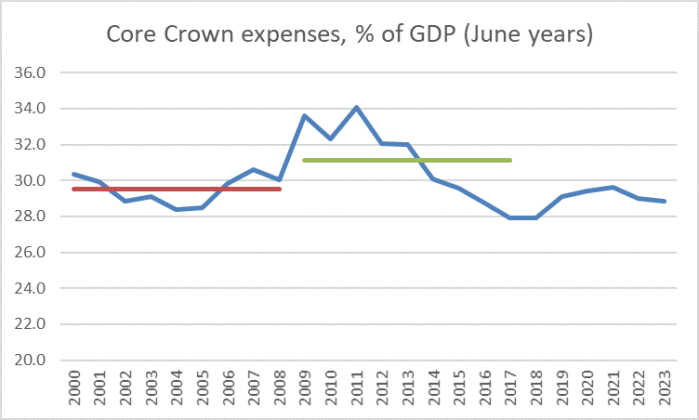

Having said all that, I come back to what has puzzled me for at least the last couple of years, and where perhaps my story overlaps to a much greater extent with Hickey’s. It is about how small a share of GDP the current government is spending, and is planning to spend. Here is core Crown operating expenses as a share of GDP, using Budget numbers out to 2023.

Spending in every year under this government (or on its fiscal plans) would be smaller as a share of GDP than the average under the previous government – mostly smaller than the average under the previous Labour government. By the year to June 2023, spending as a share of GDP would be lower than all but the last two years of the previous government. And yet in the run-up to the last election we kept hearing talk of critical underfunding in all sorts of areas of government. I guess the swing voters who just thought it was time for change weren’t looking for lots more government spending, but it is hard to believe the base in Labour and the Greens (and true believers among the journalists) weren’t looking for material increases.

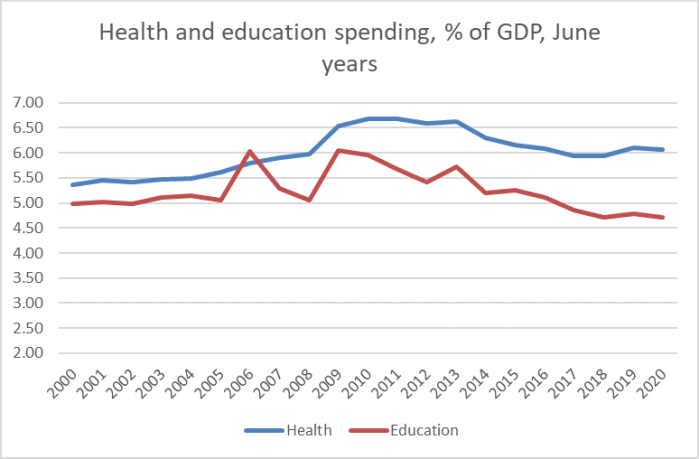

In a way, what staggers me more is this chart. All that talk about underspending was focused on health and education. But here is core Crown health and education spending, only to 2019/20, because budget operating allowances haven’t yet been allocated for later years. The first version goes all the way back to when Treasury’s data start (1972)

and this version just for this century

Education spending this year was last this low in 1988. Health spending has increased a little, but the share of GDP spent this year is lower than in all but the last two years of the previous National government. And this in a sector where the ageing population – and, arguably, advances in technology – could probably make a case for a rising share of goverment spending in GDP. At least if you were a party making the sorts of arguments Labour was making at the last election.

There is something about their fiscal choices that – based on their professed values and rhetoric – doesn’t make a lot of sense to me, a mere centre-right economist.

Of course, one reason why government spending no longer needs to be quite as high is that interest rates have come down. Finance costs (mostly interest) were almost 2 per cent of GDP in 2000 and were still about 1.5 per cent in the middle of this decade, but are projected to fall to only 0.9 per cent of GDP by 2023.

On the other hand, there is the fiscal burden of New Zealand Superannuation, the age of eligibility not now having been changed for many years, even as more of the baby boomers got to 65 and the life expectancies more generally increased. In 2008 – just as the last recession began NZS cost 3.9 per cent of GDP, in 2015 4.75 per cent, and in 2023 the cost is projected to be 5.04 per cent.

Strip out both finance costs and NZS costs and all the rest of the stuff governments do, operating spending as a share of GDP in 2023 is projected to be 2 whole percentage points of GDP less than it was when Labour ended its previous term in government (year to June 2008), and about the same as in 2015 and 2016. It is a curious achievement for a party that talked so much about underfunding, generational change etc etc. Perhaps it would be one thing if it were genuinely the result of winnowing out wasteful programmes etc, but there has been little real sign of that. Perhaps – whatever your view on the extent to which health should be funded by the state – it is one reason why our national statistics agency, something close to a public good, appears so badly underfunded.

So sceptical as I am of the Crown taking on another $150 billion of debt – as Hickey calls for – with net general government liabilities at zero, real interest rates basically zero, and the budget in surplus throughout the forecast period, one could make a reasonable case for a slightly higher level of government spending (or lower taxes). A small deficit – consistent with a small primary surplus – is consistent with keeping net debt at around its current level (share of GDP) in normal times, while providing plenty of leeway to handle the next serious recession (some mix, probably, of automatic stabilisers and discretionary stimulus).

The “normal times” are coming to an end. We have done well to keep net debt to its current low level but the government has faltered when it comes to spending on essential infrastructure vital for improving productivity, in particular roading. These projects have a long lead time. There is a large labour force and much valuable plant and machinery which will fall idle as major projects like Transmission Gully draw to a close over the coming year. It seems ideology has prevailed here too.

LikeLike

I’m a bit ambivalent. I was never that keen on Transmission Gully, but I’m told the economics look materially better now (higher population, lower interest rates) than when it was first approved.

But our masters – central and local in league – don’t think we should be driving and don’t approve of new roads, even ones that would pass a robust economic test. Of course, previous govts provided gifts to the Greens by trying to build some roads that never stacked up on decent economic grounds.

LikeLike

Michael, do you have a view on the school of thought that low interest rates exacerbate low productivity because it’s keeps ‘zombie’ firms afloat (and profitable, but barely) rather than resources being made available to younger, more productive firms? That’s a line of argument I’ve heard more in Europe and Japan (where NPLs are much higher) than places like NZ though.

LikeLiked by 1 person

I don’t have a very systematic answer, but I suppose in a sense the story line has to have something to it. In a way, it isn’t a bad thing – better than the alternative – because the alternative would be an even weaker economy. If the myriad of new innovative firms were starting up and investing they would be pretty pressure on available resources, in turn squeezing out those (so-called) zombie firms.

Much better if there were lots of new firms wanting to invest and doing so successfully, but better some economic activity than none (that is what lower interest rates do – encourage a bit more consumption, keep some firms going, get a bit more investment, and make exports a bit more competitive – but in some ideal worlds (really fast productivity growth, huge demand for new good investment) interest rates would be high. But you can’t put the cart before the horse: high interest rates won’t create highly productive economies.

LikeLike

Well Hickey is all about Keynesian styled big Government and ramping up the debt. What he forgets of course is the cyclical natures of the economy and capacity constraints. Unemployment as measured by the official method is low.

To ‘Novice’ there is a well established concept in economics called the Natural Rate of Unemployment which in effect takes into account the fact that labour markets are not exactly smoothly flowing at times. Further, if you are underemployed I would strongly suggest you work for some form of Govt agency, either Central, Regional or Local or an arm of one of these.

Hickey also make the classic error of the left of conflating the rate of interest on borrowing as the cost of capital because the rate of interest/return on equity is not seen (it has to be derived). The cost of capita has fallen as interest rates have fallen, which has increased the value of equity across the economy, and why the share market continues to rise. its not becuase firms are magically more profitable; its just a structure of interest rates effect.

On productivity… the issue is whether firms are willing to spend the capital. As an example I am assessing a small production line for an export business. The capita cost of the high labour/low capital is c$350k, while the low labour/high capital is $1.4m, so a diff of $1m to make the numbers easy. My impression of how NZ business managers think is that they would much prefer the $350k option because that is less $ up front. However, the numbers show that the payback period on the $1.4m option is about three years – which means that if you have confidence in your market then this is the better option. A quick NPV will show that over 5 years the $1.4m will create more value for the firm.

But NZ managers will say… but its too expensive and we will make do… thereby cutting their noses off despite their faces. its almost the reverse of the sunk cost fallacy.

LikeLiked by 1 person

Reblogged this on The Inquiring Mind and commented:

An interesting post by Michael Reddell on current fiscal policy and where Labour’s rhetoric departs from reality. This post draws attention to some intriguing facts, some of which are very much at odds with Labour’s mantra of 9 long years of underfunding.

LikeLike

The immigration economy… that’s going to end well, obviously, with a significantly higher proportion of migrants relative to base population than either Trumpland or Brexitland… obviously there is zero correlation between massive population growth through neo-colonial immigration and stratospheric house price rises and wage suppression… clearly, if the 40%+ of Aucklanders born overseas vanished overnight, house prices would not collapse, but simply rise further…

LikeLiked by 1 person

You are right. 25% of NZ are born overseas replacing the 1 million that have left to live overseas and the end result has been increasing house prices. Even with a significant slower approval rate of residency Visas under this government, the number of temporary foreign workers continue to rise.

LikeLike

The strange thing about foreign workers is they somehow end up married with a New Zealander and all of my mothers health care groomers are now pregnant with a child.

LikeLike

Anyone that thinks the government can change the climate and should borrow billions in the attempt should be listened to with great caution.

Cancelling worthwhile roading projects (that were already in the pipeline), replacing them with harebrained ideas like cycle lanes and slow trams to Wellington airport or shutting down the oil and gas exploration is an indication of of the ideologically driven nonsense this fool of a government indulges in; it would be better if they did nothing.

Hooten on the Wellington debacle: This is a story about the allocation of $6.4 billion of public money and a Green Party that wants to cover up why particular decisions were made. It underlines that the Official Information Act (OIA) is broken.

Contradicting the Wellington City Council, the Greater Wellington Regional Council and the NZ Transport Agency that had worked together on the plan for some years, Twyford’s package delayed a new Mt Victoria tunnel until the 2030s.

Instead, the money would be allocated in the 2020s to — you guessed it — a billion-dollar-plus tram from the railway station to the airport. The tram would be slower than the airport bus, which currently takes only 25 minutes to the CBD yet is underused.

https://thebfd.co.nz/2019/08/hooton-on-genter/

LikeLiked by 1 person

I find it hard to believe the inflation figures. My farm just had an %18 rate increase, my insurance has gone from $5800 to $6800, Road user taxes up %10, plus another %10 next year. Almost all my costs are up so i suspect CPI figures are a load of bull.

LikeLike

I guess those increases are netted out by continuing falls in our imported China and India manufactured products like clothing and plastic goods, Huawei smartphones, TV sets, cameras. Also I have seen alot of food items have fallen in price.

LikeLike

“Steven Joyce’s discovery of a $11.7 billion hole in Labour’s proposed Budget at the last election, or John Key’s “Show us the money, Phil” taunt to Phil Goff in 2011 were great attack weapons at the time, but in the absence of independent verification voters were left none the wiser as to their accuracy.

A politically independent statutory office, able to verify or debunk such claims, to help resolve voters’ uncertainties about the veracity and accuracy of claims like these, would have been welcomed at the time.” Peter Dunne.

Given that 7 so called independent economists got it wrong at the last election which benefited Labour’s extravagant lies, I do not think a independent statutory office is going to be effective. They will have a bias towards keeping the Labour government that appointed them in government. Steven Joyce’s estimates have been proven to be correct and 7 economists proven wrong.

LikeLike