Earlier this week, the Reserve Bank published (almost all of) the submissions it received on the Governor’s proposal to increase very markedly the share of bank balance sheets that need to be funded by equity.

Welcome as it is to have the submissions – it is easy to forget that not four years ago the Reserve Bank was still reluctant to publish any submissions it received at all (even though it was the norm for government agencies, parliamentary select committees, and so on) – the Governor sought to use the occasion for some more spin in support of his proposal (on which he alone will, a few months from now, make the final decisions – the rest of us, whether Minister of Finance, banks, businesses or citizens will simply be stuck with the results of his whim, with no mechanisms for appeal or review.)

Instead of just releasing the submissions – which could have been done weeks ago, very shortly after submissions closed – the Bank chose to release a 22 page document labelled “Summary of Submissions” and a lengthy and argumentative press release in the name of the Deputy Governor.

I haven’t read all the submissions, or even looked at them all, but one reader – distracting himself from other stuff he should have been doing – did look at them all, and sent me a spreadsheet with the names of the submitters, the length of each submissions, and broad tenor of any comments.

A good consultative process draws out perspectives or comments or evidence that the consulting agency may not have thought of, may have chosen to ignore, may have interpreted differently, may have missed the point of, or whatever. Having received that material, the consulting agency would carefully consider those perspectives, (in principle) looking to make the best decision, open to a revised perspective. Of course, that sort of openness is rare – it runs against human nature, particularly where the people making the final decision are the people who proposed the scheme in the first place.

And a consultative process shouldn’t be thought of, or presented as akin to, a public opinion poll. If one wanted to make such decisions by public opinion poll then I guess (a) we wouldn’t delegate them to a specialised agency, and (b) we would commission a properly structured poll. Apart from anything else, (a) people who are opposed to what is proposed are typically more likely to submit than those in favour, and (on the other hand) (b) especially when the numbers involved are small, it is easy for a handful of low-information submissions to be generated on either side of the issue.

The Reserve Bank, however, has tended to present the submissions as something of an opinion poll. There was the silly line that “in general, submitters support the Reserve Bank’s objective to ensure that New Zealand’s financial system is safe” – yes, and we support motherhood and apple pie too. The issue isn’t whether the system should be “safe”, but how safe, and at what cost, on what assumptions. And then

There was significant and wide-ranging media and public interest in the How much capital is enough? (PDF 545 KB) paper, with written feedback from 161 submitters.

Yes, 161 submitters is a lot more than the nine submissions they received on the previous paper in the longrunning capital review but in the grand scheme of things – considering the scale of the changes the Bank is proposing – it isn’t many. And more than 20 per cent of the submissions turned out to be six lines or less: whether the submitter was for or against what the Governor was proposing (and in some cases it really isn’t clear) there is no useful information for a proper consultative process in submissions that short (unless perhaps one of the big banks had submitted “Dear Adrian, We agree. Do start soon.”, which they didn’t).

Thus, when the Deputy Governor says

Many submitters, particularly from the general public, support the proposed higher capital requirements for banks.

He is correct. Many did. Very briefly. Usually without much engagement in the argumentation and issue (although one of the Governor’s mates did write in to offer support and some argumentation, although strangely even he referred to some evidence that capital ratios should be 13-14 per cent, which led him to the view that the Bank’s proposed (minimum) ratio of 16 per cent was “acceptable”.)

And look at this attempt to play the populist card – the public versus the banks – a bit further

Some submitters, in particular banks and business groups, question whether the proposed increases are too large and too costly.

As they know very well, there were a variety of other serious – more than half a dozen lines long – submissions from people with no vested interests who were very sceptical of the Bank’s proposal, and of the argumentation and evidence in support of it.

You also have to wonder how well the Bank would be able to defend a claim (perhaps in a judicial review) that the consultative process was a sham. The Deputy Governor again

Increasing the amount and quality of capital can be reasonably expected to mean that banks can survive all but the most exceptional shocks, Mr Bascand says. “We think the costs of doing so are outweighed by the benefits – someone’s cost is for society’s broader benefit.”

(do note the attempt to play vested interests again: “someone’s cost”). Isn’t it still months until the final decision is supposed to be made? And yet the Deputy Governor can confidently declare not just ‘in putting out the consultative document we thought it likely benefits would exceed costs”, but (present tense) “we think the costs…are outweighed by the benefits”. And if the Deputy Governor already knows perhaps he could release that cost-benefit analysis that so many submitters and other commentators have been calling for. I guess they haven’t yet back-fitted the numbers to suit the Governor’s conclusion yet.

Continuing with the spin, the Deputy Governor moved on to invoke support from the International Monetary Fund and the OECD, both of whom released comments on the New Zealand economy last week.

Following its recent mission to New Zealand, the International Monetary Fund has released a Concluding Statement that highlights the need for strengthening bank capital levels and that the proposals appear commensurate with the systemic financial risks facing New Zealand. The Organisation for Economic Co-operation and Development’s latest Economic Survey of New Zealand expects increases in capital will likely have net benefits for New Zealand.

It is hard to make much of the IMF comments at this stage. They are not much more than a couple of sentences in a press release, with no published supporting analysis. And the Fund almost always backs the authorities – who are the people they talk to most – especially when central banks and regulators want to put more restrictions on banks. Why wouldn’t they? Any economic costs don’t sheet home to them. But the IMF’s support isn’t without its problem for the Reserve Bank. Here is what they said

The new requirements would increase bank capital to levels that are commensurate with the systemic financial risks emanating from the dominance of the four large banks with similar concentrated exposure to mortgages, business models and funding structures.

Which, by logical deduction, appears to be saying that current levels of capital are grossly inadequate to the risks the New Zealand banking system faces. But there was no hint of these serious risks in past Financial Stability Report from the Reserve Bank (although they amped up the rhetoric in the latest one), and – perhaps more to the point – no hint of that in past IMF Article IV staff reviews or Executive Board discussions. This snippet is from last year’s Article IV report, published as recently as June last year.

Not a word from staff, from the Board – or, indeed, fron the New Zealand authorities in their published comments – of a pressing need for a huge increase in minimum capital ratios.

The Deputy Governor also attempts to deploy the OECD in support. They typically aren’t particularly expert in such matters, but here is what they actually said:

The Reserve Bank has proposed large hikes in bank capital requirements. High bank capital requirements reduce the cost from financial crises, but might also dampen economic activity through higher lending rates. On balance and nothwithstanding considerable uncertainty, increases in bank capital are likely to have net benefits, but the impacts should be carefully monitored.

Take it from me – I negotiated line by line wording on numerous OECD reports – that is about as tepid as it gets. It doesn’t even endorse the huge increases in minimum capital the Governor is proposing – the comment is simply about “increases”, and there is a long way from current levels to what the Governor has planned.

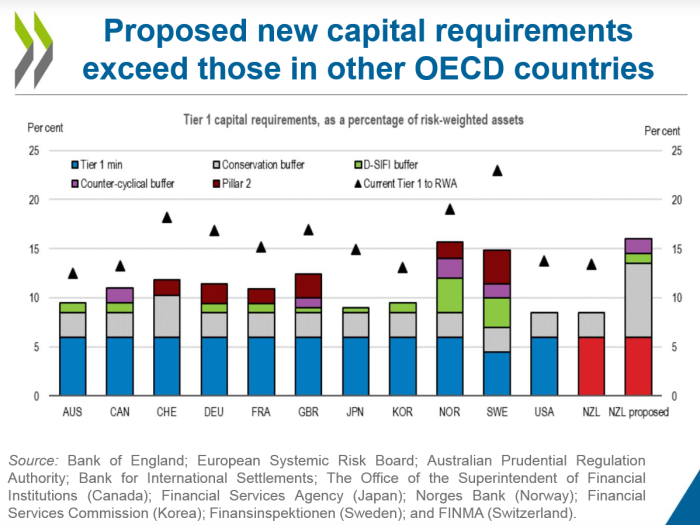

And if you doubt my take on the OECD, here is their own slide from the presentation when they released the report in Wellington last week.

And these comparisons are just of headline required ratios (triangles are actuals I presume), while part of the Reserve Bank proposal is to materially increase the calculation of risk-weighted assets for the big 4 banks, to an extent that would, in effect, add another three percentage points or so to those New Zealand numbers, which already – in the OECD’s words – “exceed those in other OECD countries”.

So, spin all the way down. Complete with the observation about their continuing consultation – fishing around to find some supporters perhaps

It is continuing its stakeholder outreach programme, which includes conducting focus groups to understand the public’s risk appetite, and engagement with iwi, social sector and industry groups, financial institutions and investors. It has also engaged three external experts for an independent review of its proposals.

They elaborate a little in the document that supposedly summarises the submissions. On the iwi point “a workshop with Maori service providers” – but why, what specific issues might there be for “Maori service providers” (whatever they are) from any others – Catholic, Pacific, or whatever? And the workshop they plan with “social service providers and NGOs” really looks like an attempt to drum up support for the shonky “social costs of crises” material they’ve run previously, and which Ian Harrison (in particular) has comprehensively demolished. I will be lodging an Official Information Act request for the reports etc from any focus groups – again it looks a lot like an attempt at distraction, a populist Governor trying to summon a mandate from “the people”, rather than from Parliament.

Also from that Summary of Submissions, this attempt to spin the issue (wasn’t this supposed to be a summary of submitters’ view and analysis?)

It’s about keeping New Zealanders, their investments, and the economy safe from the disastrous impacts of financial instability and the failure of a registered bank, which historical evidence suggests can be very long-lasting and go beyond just the financial costs for people.

Loaded language (and not even particularly well written). Nothing like a bogeyman to scare people with I suppose, but surely only fairly geeky people even read a document like this. Who is the Governor hoping to impress? Not much sign of calm, balanced, detached and objective consideration, that’s for sure.

(Having said that, it was noticeable reading through the Summary itself how few arguments staff managed to find from the submissions in support of what the Governor was proposing.)

The other person who has weighed in this week is the Minister of Finance, with a rather plaintive appeal to everyone to get on and talk nicely, as if he was a harried parent pleading with children to just play nicely (“pleeeeeeease”) at the end of a long tiring day. The Minister is reported to have called for a “mature debate”, observing

“I want to remind all parties that we are still in a consultation process. I am calling on all interested participants to listen to and work with each other constructively as this work is carried out.”

It wasn’t exactly authoritative.

Perhaps he might address his concerns specifically to the Governor, including via the Acting Secretary to the Treasury and the Bank’s Board (whose job to work for the Minister and the public to monitor and hold to account the Governor). And perhaps he needs to wake up to the power asymmetries here: we have a single unelected official (largely appointed by some other unelected board members, all appointed by the previous government), championing huge increases in minimum capital requirements, having made no effort to socialise thinking or test reasoning before settling on a view, and is now judge and jury in a case he himself is prosecuting. And the “defendants” – not just banks, but the wider economy – have no rights of appeal. And the way the Governor has conducted himself – dismissive of sceptical comments, strong elements of pre-meditation, no cost-benefit analysis, no serious analysis of the transition, no serious engagement with the Bank’s preferred resolutiuon tool (the OBR), “independent” experts handpicked by him to review the proposal (but barred from talking to anyone else without his permission) and so on – doesn’t exactly inspire confidence. He talks a lot about “making banks safer”, but all independent analysis – and their history – suggests the banks are fairly safe already: we could reduce lots of risks in society to near-zero (the road toll for example) but the costs just aren’t worth it. He simply hasn’t made the case that this proposal – which he cannot commit would even endure beyond his governorship – is worth the risks and costs.

The Minister of Finance does not have formal powers to stop the Reserve Bank. It is right and proper that the Minister should not be able to interfere with supervisory decisions or judgements involving individual institutions, but what is going on here is probably the largest policy initiative (bigger than, eg, outsourcing/local incorporation) around bank regulation in many decades. Big policy calls – in areas where there is huge uncertainty (as the OECD, among others, says there is here) – really should be a matter for politicians. At very least, they shouldn’t be a call for a one-man band with a bee in his bonnet (and without even any particular specialist technical expertise).

If the Minister really wanted to display some leadership he would call in the Governor (in consultation with the Secretary to the Treasury) and strongly urge that the entire review be put on hold. There are several and sufficient reasons to do so:

- the government has made provisional decisions around deposit insurance, but there has been no attempt to link that initiative and the bank capital proposal,

- Phase 2 of the review of the Reserve Bank Act is well underway, and the provisional intention is that the Governor should no longer be the sole decisionmaker on matters of prudential policy, and that in future Treasury should play a stronger review role,

- there is absolutely no urgency about doing anything about bank capital now (as every one recognises banks are strongly capitalised and have strongly capitalised parents, and it is only a few years since capital ratios were increased),

- if anything, there is a strong case for doing nothing right now: the looming economic slowdown and diminished inflation pressures that are leading to OCR cuts remind us again of the approaching limits of conventional monetary policy. The last thing we should be doing in that climate – when stress tests etc show that bank balance sheets are sound – is throwing more sand in wheels, potentially impeding credit availability over the next few years.

Of course, the Governor could refuse such a request, but he would be very unwise to do so. The Governor has no public mandate, no independent source of legitimacy, and this is not an issue about the supervision of an individual institution – it is about overall economic management, where the big parameters (eg inflation targets, debt targets……and financial stability goals, which are harder to pin down) should be made by those we elect, and can toss out again. It should hardly be controversial if the Minister were to suggest to the Governor that he would be prepared to legislate so that in future changes in bank conditions of registration – the lever the Bank uses – could only be done by Order-in-Council, not simply on the Bank’s whim. After all, that is how the prudential regime works for non-banks (and you’ll note there is no proposal in front of us to markedly increase capital requirements for non-bank deposit takers).

We need expert advice from the central bank – something we aren’t getting at present – and expert independent adminstration of the rules, but the big policy calls (which involve significant risks, which no one can determine definitively) need to be the responsibility of the elected government.

For anyone interested, my own submission is here.

PS. As Martien Lubberink at Victoria has pointed out there is another international agency paper out just recently that really doesn’t help the Bank’s case much if at all. I might touch on that tomorrow.

with one or two exceptions (who had other agendas) the non – ‘members of the general public’ were opposed to the proposals’

Overall supporters were in a minority.

Even amongst individuals there wasn’t a strong majority.. Many people say through the Bank’s spin and were worried about the costs.

LikeLike

The amounts demanded of the banks is far too damaging. Contrary to what some commentators believe banks can’t magically create money. It acts as intermediaries and every dollar they have belongs to someone else. Even every dollar they earn they pretty much distribute to shareholders.

Increased capital buffers mean that there is more dead weight cash sitting around waiting for a disaster and not deployed earning more profit. Less profit equates to a higher risk bank rather than a lower risk bank. Adrian Orr is creating bank instability by the size and speed of his demands.This is getting ridiculously dumb and stupid because he is in effect fear mongering. Fear mongering equates to a run on bank deposits and we all know what a run on bank deposits mean. No amount of capital buffers is going to be sufficient to cover a fall in confidence in banks which brings us back to government deposit guarantees.

LikeLike

Thanks Michael,

In case you want to know which other agency that was, see the blog post on capitalissues.co

Cheers!

LikeLike

Tane Mahuta has commanded that capital requirements must increase. Orr has no option but to obey.

LikeLiked by 1 person

I think Adrian Orr thinks he is Tane Mahuta.

LikeLike