I wrote a post a month or so go about some comparisons between the drop in business confidence after the previous Labour government took office at the end of 1999 and the current fall. At the end of that post, I concluded that the current situation should probably be more concerning than the earlier episode which, intense as it was at the time, blew over fairly quickly. Perhaps the biggest difference, I suggested, was around the exchange rate:

The current level is about 30 per cent higher than it was in 2000, and it had fallen a long way to get to those 2000 levels (and not on heightened risk concerns etc). Those falls created a credible prospect of new business investment in the tradables sectors. There is nothing comparable now, and we’ve probably exhausted the limits of domestic demand (especially residential investment) as a support for headline GDP growth.

The Reserve Bank’s TWI measure of the exchange rate has averaged about 74.4 this decade to date, with a standard deviation of about 3.7. Thus, although the current TWI is now a bit lower (72.6) than it was at the time of last year’s election, in both cases the numbers were within one standard deviation of the mean. Those sorts of fluctuations are often little more than noise. There is nothing yet visible in the current government’s plans and policies that is likely to reverse the longer-term structural overvaluation of the exchange rate.

Another comparison I’ve seen in recent days is with early 2008. Some of the business confidence measures are back to the sort of levels we saw in early 2008. I saw one prominent journalist opining that “current conditions are nothing like 2008”. No doubt true if one has in mind the final (global crisis) quarter of 2008, but in April/May 2008 – when business confidence had weakened to similar levels to the present – New Zealand was already in recession (so the published data tell us) but few people realised it. Here, for example, was the Reserve Bank in June 2008, still asserting that GDP growth that year would be positive (and they weren’t alone in that view).

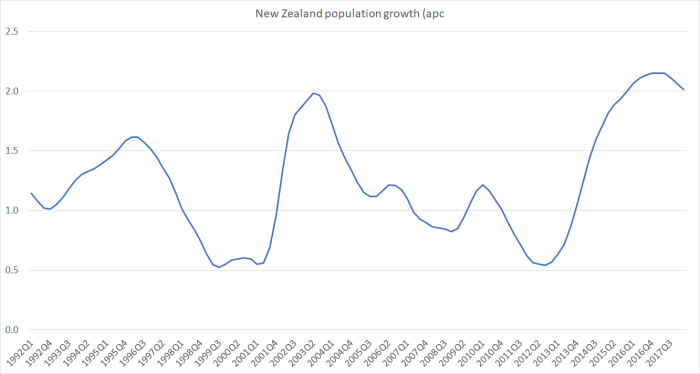

Another comparison relevant to making sense of business surveys (and the like) is population growth. For better or worse (mostly worse, on my telling), the current population growth rate is still much higher – at least twice as high – than it was in either 2000 or 2008.

When the population is growing that rapidly, business surveys don’t mean the same thing as they would if (say) the population was flat. A typical business survey will ask whether things are rising, falling, or much the same, and report the net of those saying higher and those saying lower. With 2 per cent population growth, one should expect net positive responses even if per capita activity was going backwards a bit. At present, 2 per cent annual GDP growth would be a really bad outcome.

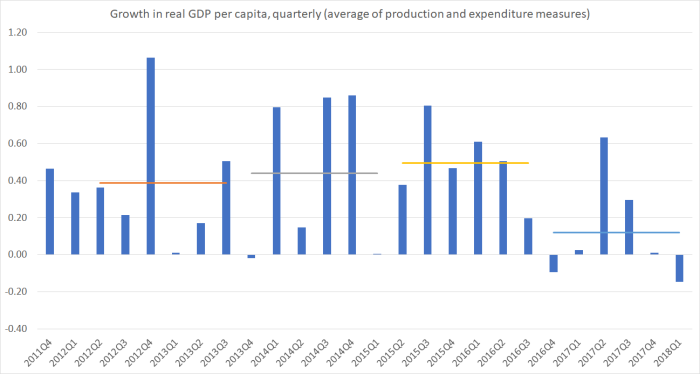

At her post-Cabinet press conference yesterday, the Prime Minister seemed to be flailing. She preferred, we were told, to look at real data to judge how things were going. Here is one such chart from my earlier post

How have things been going on real GDP per capita? Not well, and that included late in the term of the previous government. Perhaps there is some element of businesses slowly realising just how mediocre our economic performance has been. Perhaps the Prime Minister – who during the election campaign was too ready to grant that things were going well economically – should wake up to the underperformance.

What about other real indicators?

The Prime Minister talks of our “low” unemployment rate, and yet seem conveniently oblivous to the fact that among the G7 leading advanced economies, the UK (Brexit and all), the US (Trump and all), Germany, and Japan all have unemployment rates lower than New Zealand’s. Ours is better than it was, but it is nothing much to be proud of – roughly one in 20 New Zealanders keen to get a job, ready to start work next week, can’t find one (and that is narrowest definition of excess labour capacity). Labour would once, rightly, have regarded that as pretty shameful.

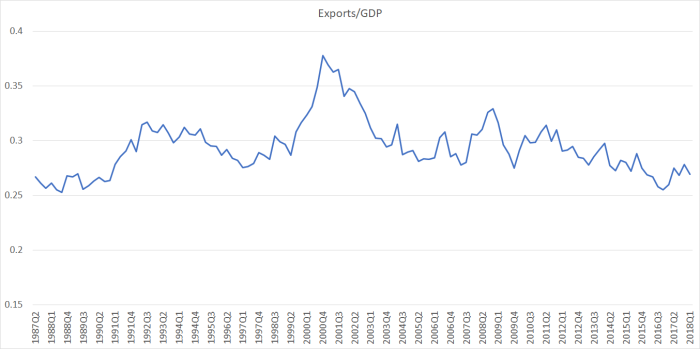

There has been very little growth in productivity at all for five or six years now, and last week’s labour market data (showing quite reasonable employment/hours growth, even as no one expects stellar GDP growth this quarter) suggests the trend has continued. And for all that we are suppposed to be impressed by yet another board, this time to consult on trade agreements (chaired by a competent former diplomat who now works for the propaganda arm of MFAT/NZTE, the New Zealand China Council), the reality remains one in which exports (and imports) as a share of GDP have been shrinking not rising. That isn’t how things go in successful economies.

Business investment has been weak too, especially once one takes account of the needs of a rapidly rising population.

The Prime Minister tell us that in a speech later this week the Minister of Finance will outline how the government expects things to be turned around, with our economy becoming more productive, more outward-oriented etc. I will, I’m sure, read the speech with interest, but there is little sign that anyone near the top of government really has a sense of what might make a useful and substantial difference to the medium-term performance of the New Zealand economy. You will, for example, never hear them talk of a real exchange rate out of line with the relative productivity performance of the New Zealand economy, or show any understanding of how that might come about. In practice, they seem wedded to much the same failed economic strategy as the previous government – notably the “big New Zealand” rapid inward migration strand – made worse, at least in prospect, by things ranging from large increases in minimum wages to aggressive headlong pursuit of net-zero emissions targets with not a decent cost-benefit analysis in sight. Whatever the merits of, say, capital gains taxes or R&D tax credits (and I’m not persuaded of either), they simply aren’t game-changing stuff.

One of the uncertainties about New Zealand economic data is what happens to the outflow of New Zealanders (mostly to Australia). Because the wage differentials are so large, the normal state of affairs is for the outflow to be quite large. Those income and productivity gaps haven’t closed in recent years – if anything they’ve widened – and as the Australian labour market has recovered, the outflow of New Zealanders has been picking up again. If things remain more positive across the Tasman we can expect that trend (growing outflow) to continue. If so, it might dampen activity here a bit further, offset by the increased sales New Zealand firms can make in a better-performing Australian economy. Then again, business confidence measures in Australia don’t seem stellar at present either (the latest manufacturing PMI number is very similar to that in New Zealand).

I try to largely avoid economic forecasting. Mostly, it is a mug’s game (the future, beyond perhaps a couple of quarters ahead, is basically unknowable), and it is a very rare forecaster who will prove right for the right reasons (and more than randomly so). Perhaps the economy will weaken from here – there is a lot running against it, and not much for it – but perhaps not. But what really disconcerts me is that lack of much sign of serious thinking of how the next serious downturn – which will happen, it is only a matter of when – should be handled. That sort of complacency, especially in officialdom, was never really excusable even when things seemed a bit more buoyant – after all, we pay these people (so they tell us) to take a rather longer-term view. But it is even more worrying now. The official view that interest rates would soon move higher again has been falsified by experience, year after year.

As a reminder, the OCR now is 1.75 per cent. That is lower than official interest rates were in every country in the world, bar Japan, going into the last recession (our own OCR was 8.25 per cent then). The Reserve Bank tells us that they agree the OCR probably can’t usefully be cut below about -0.75 per cent, which just isn’t that far away – even if people have been lulled by almost a decade in which the OCR has been in a range of 1.75 per cent to 3.5 per cent.

We’ve had a new Governor now for 4.5 months, and have not had a single substantive speech from him on monetary policy (his only on-the-record speech notes have been about climate change, for which he has no responsibility at all). And, of course, we’ve heard nothing on these issues (and threats) from the Minister of Finance or the Secretary to the Treasury. And while there is lots of talk of how much fiscal room New Zealand supposedly has, remember that revenues will drop away quite quickly in the next recession, the NZSF will be booking big losses, and the political process will almost inevitably balk at really large, repeated, fiscal stimulus. For those doubting that, look at the political limits to fiscal stimulus in the last US recession, or the UK, or….well, almost anywhere.

But if our officials and politicians are letting us down, the contribution of the leading market economists doesn’t seem to be any better. I’ve read the MPS previews (for this week’s RB announcement) of three of the four main banks, and not one seems to devote any space to the “what if” questions. They all seem to believe that we’ll get through the current confidence dip in reasonable shape, and so the real question is when the OCR will be raised. Perhaps they will be right about that. Perhaps too they are mainly interested in foreshadowing what the Governor might say or do this week (and he and his institution have been pretty complacent for a long time). But what if things don’t work out fine? What if we do find ourselves in a recession in the next 12 or 18 months? And how best should we think about the probabilities, and about the best possible policy responses, given the uncertainties and the very real limits of the OCR instrument much beyond the current level? It doesn’t seem to be something our leading market economists even want to address.

(My own view isn’t an unconditional forecast, but a conditional statement: if there is an OCR change in the next 12 months it will be a cut.)

There is a serious need for some hard thinking, and sober realisation, about the disappointing performance of the New Zealand economy. It would be a shame if the current downturn in business confidence (whatever specific mix of factors, political and otherwise, is driving it) were just used for another round of patting people on the head, and reassuring them “don’t worry, after all, we are one of the best-performing economies in the world”. In truth, we are anything but, and nothing either of our main political parties has to offer gives any reason to expect change for the better.

I agree with you regarding forecasting Mike. I think we can have a pretty good view of how the economy might evolve on a 3-6 month basis but beyond that its quite murky and no-one really can tell where the economy might head.

With regard to the ANZ Own Activity index its pointing to negative GDP prints in either Q2 or Q3 which is concerning and our back-of-the-envelope calculations suggest the RBNZ should be revising down their near-term GDP growth outlook fairly significantly. That in turn will pull down the output gap and weigh on core CPI inflation projections.

I think some commentators have been highlighting the sector factor model’s 0.1pp increase – to 1.7%y/y – as an indication that core inflation is rising. I think that’s a mistake. While we have seen a lift in rental costs last quarter, and that requires monitoring, I believe that the sector factor model is picking up the impact of the rise in petrol prices that we’ve seen. Stripping out petrol prices, CPI-X is moving on a quarterly basis more-or-less exactly in line with the past 5-years average and shows no sign of increase. Indeed, as base effects feed in, we could see headline CPI come back off. Arguments that the RBNZ will take a more hawkish line based on rising petrol prices and/or wages (driven by administrative measure) seem hard to see.

Im pretty bearish here and my guess is that the RBNZ is actually going to tilt more dovish.

As for the longer term issues you highlight, my concern is that instead of getting a through review of our growth model and a serious look at the problems we face, they will simply turn the fiscal spigot and we will get more “infrastructure” investment, further propping up the non-traded sector and the real exchange rate.

LikeLike

Re the final para, that and another round of OCR cuts (probably belated) eventually. We can keep the economy more or less employed that way, as we continue to fall behind our former global peers.

LikeLike

With the Federal Reserve holding $4 Trillion of stimulus on its balance-sheet, waiting to be dis-gorged, can anyone claim the 2008 GFC is over and out when it appears (to me) they are only half way there. That $4 trillion is a time-bomb. It has to be covered or inflated out of existence. Choose your poison.

LikeLike

Just looking at the RBNZ chart packs and it seems like the period from 2000-2004 was a bit of a golden period. Growth was faster, the RER was a lot lower and inflation generally within the bands. And the current account was a lot better.

What was it about that time that enabled the economy to come into balance?

LikeLike

(overly) broadly speaking, it was also a period of weak migration, and interest rates that weren’t always unusually high by international standards (notably in 2000, the period when the TWI reached its trough) and the hype around new economy vs old economy – which weakened both NZD and AUD. We reckoned at the time, there was an 18 mth plus lag from changes in the real exchange rate to real activity, so to the extent it was a reasonable period for the economy, it reflected the weak exchange rate from say late 1998 to 2002.

LikeLike

I agree with some of the things the Government is doing, and I like some of their Ministers such as Phil Twyford and Julie Anne Genter. But I agree with your thesis that the combination of high NZD and big wage increases will be terrible for growth.

LikeLike

I suspect Twyford’s heart is in the right place, re housing, but I remain sceptical that it will be allowed to come to much. (I guess the market shares my scepticism, or we’d be seeing peripheral land prices plummeting.)

LikeLike

I think it is disgusting that we don’t look long term and ask “what if”. I think the reason has a lot to do with a shift of focus from looking after New Zealanders to an obsession with racism: if people are against immigration they must be racist; why should we look after racists? Helen Clark told Ian Mclennan (Gandolf) that “NZ was really a deeply racist nation and she was determined to do everything in her power to change that”.

LikeLike

…hmm; seems if recent growth has been low per person, there hasn’t been much of a ‘boom’ so the chance of a ‘bust’ is likely low; and while the OCR is low relative to its own history it is high relative to quite a few advanced nations (ex US) so would think there is still room if/when demand cools..

LikeLike

[…] economist Michael Reddell says in his […]

LikeLike

Reblogged this on The Inquiring Mind and commented:

Some very interesting comments by Michael Reddell

LikeLike