A few months I signed up to get the e-mail newsletters of US analyst Aaron Renn.

Aaron M. Renn is a senior fellow at the Manhattan Institute, a contributing editor of City Journal, and an economic development columnist for Governing magazine. He focuses on ways to help America’s cities thrive in an ever more complex, competitive, globalized, and diverse twenty-first century.

There is an interesting mix of material on urban issues. But this morning, one newsletter in particular caught my eye. The title was a warning: “Sprawl in its Purest Form, Cleveland edition”. The article began this way.

…..the image below contrast[s] the amount of urbanized land in Cleveland’s Cuyahoga County in 1948 vs. 2002. The county population was identical in both years: 1.39 million.

And the piece goes on to lament how costly the spread of suburbia is, concluding that

As a rough heuristic, development of new suburban footprint should largely be limited to the growth rate in households to avoid saddling a region with excess fixed cost.

It might be music to the ears of some of our own planners, and the politicians who continue to enforce their policies.

Renn laments the fact that, at least in this case, when cities can spread and new houses can easily be built, while the population doesn’t change much, existing houses lose value

If you keep building new homes but you aren’t adding households, then older homes at the bottom of the scale will be abandoned. And all up the stack homes are devalued.

In the same way, when we had restrictions on importing cars in New Zealand for decades, secondhand cars didn’t depreciate much. Most of us prefer access to newer cars.

I had a look at some Cleveland data. And sure enough not only has that county’s population been largely unchanged, but greater Cleveland (MSA) with just over 2 million people also hasn’t had much change in population for 50 or 60 years (if anything falling slightly more recently).

I also had a look at house prices. Demographia reports that Cleveland median house prices are 2.7 times median incomes in Cleveland, averaging US$146000 last year. Average per capita GDP in the Cleveland metro area was around US$56000 in 2016.

On the other hand, a friend had mentioned the other day a house, perhaps 150 metres from where I’m typing, that had sold the other day for $831000. It is a small house (100 square metres) on a pretty tiny section (324 square metres) – with a major construction project almost on the doorstep for the next 18 months or so – and as far as I can see nothing out of the ordinary. That is the point – it isn’t egregiously expensive for Wellington (let alone Auckland) in this day and age. It is about what one might expect, given our laws and regulatory practices. Average GDP per capita in Wellington in the year to March 2016 was around $NZ67900 – a fair bit less than in Cleveland.

Homes.co.nz records that the same Island Bay house sold in 1985 for $76500. Apply the Reserve Bank’s inflation calculator and in today’s dollars that would be the equivalent of $207000. The actual recent sale price – the real increase in price – was four times that.

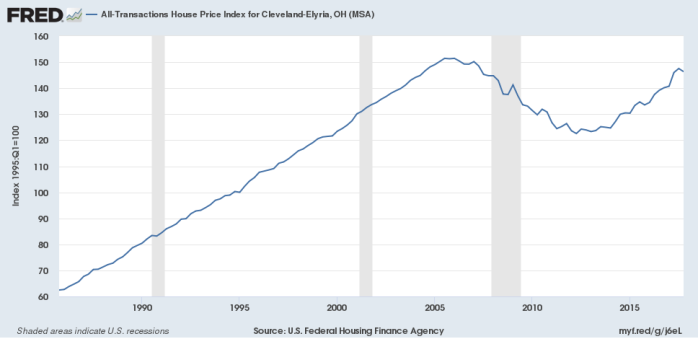

How have Cleveland house prices done over time? Here is a chart, back to 1985, from the FRED database.

Nominal prices have increased quite a lot. But in real terms, applying a US inflation calculator, Cleveland house prices have barely moved – up a bit in the boom years, down in the recession, but over 33 years virtually no change at all. Houses were highly affordable then, houses are highly affordable now. And lest you assume Cleveland is some economic wasteland, the FRED database also suggests that the unemployment rate there has been averaging about 5 per cent in the last year or two, very similar to that in New Zealand.

I usually focus on cities with fast-growing populations in discussing US examples of low and affordable house prices – eg Atlanta or Nashville. And I’ve never been to Cleveland, and have no particular idea how attractive or otherwise parts or all of it are (in Wellington, Porirua and Wainuiomata – for example – also have their downsides). But the ability of the citizenry to readily expand the physical footprint of the city seems like a success story, producing housing market outcomes that seem much more appealing – particularly to younger people trying to enter the market – and affordable than what we now seem to manage in our larger New Zealand cities.

We should steer well clear of “rough heuristics” or tighter rules that try to limit the expansion of the physical footprint of cities, or allow officials and politicians to determine which land can and can’t be built on, in what order. A competitive market for urban land – peripheral and central – remains the best prospect for once again delivering what should be a basic expectation: affordable housing.

Sadly, I noted in ACT’s newsletter earlier in the week, a link to a parliamentary question from a few weeks ago in which the Minister for the Environment indicated that “Cabinet is yet to make any decision about whether to review the Resource Management Act”. I’ve long been sceptical as to whether, even if some Labour parts of a left-wing government was willing to think about serious reform, such reform would be possible given the reliance on the Greens to pass government legislation. Sadly, for now it increasingly looks as if those fears are being realised.

House – and land prices – need to fall. This government, like its predecessor, seems at scared of such an outcome, and unwilling to take steps that offer the prospect of sustained much lower prices.

The answer is here

According to the 2010 census, Cleveland had a population of 396,815 and the racial and ethnic composition was as follows: Black or African American: 53.3% White: 37.3% (33.4% Non-Hispanic Whites) Asians: 1.8% (0.7% Chinese, 0.4% Indian, 0.2% Vietnamese, 0.2% Filipino)

Consider what isn’t there, not what is

Our daughter has just been here from San Diego on a break – she says racism is toxic right across USA

LikeLike

But that is only Cleveland city, the downtown area. The metropolitan area is about 2m

LikeLike

Cleveland recently topped a national list of “most distressed cities,” and its neighbor East Cleveland is on the verge of bankruptcy.

A google search of Cleveland brings up a long list of bankrupt articles. Not exactly a model city is it?

LikeLike

Right, but again you are talking about two specific localities within the Cleveland MSA. Cleveland city is about 20% of the MSA, and East Cleveland is tiny and depopulated.

Reading around the overall MSA, it doesn’t look like the finest city in the USA, but equally it seems to have quite a bit going for it (beyond just affordable housing). And, much as some people really like Wellington, it also has more than a few drawbacks (certainly wouldn’t top my “best city to live in” list for NZ).

LikeLike

East Cleveland – yikes

That’s one way of pushing the people to the outer suburbs

https://ru-clip.com/video/oCx9zIsUFXI/abandoned-east-cleveland.html

Look at the first few comments – that’s racism for you

The land use graphic used by Renn would seem to classify anything that is not rural as urban – guess it includes East Cleveland – the problem with the land-use graphic is the red flood-colour visually implies a constant population density right across the MSA – which is unlikely

LikeLike

If Auckland brings in Huntly East then you likely have a Cleveland East scenario. How far do you want to push outwards before people decide they do not want to live there in spite of all the infrastructure spending. But in saying that, my Huntly West 4 bedroom property bought 15 years ago at a rental at $250 a week with a current rent at $320 a week has been suggested by my Property Manager should now go to $400 a week.

LikeLike

Takes me back to my first experience of working in a foreign country about 1980 – installing software and training at Cuyahoga Community College. Seemed like a pleasant city but I was only there for 2 or 3 visits each lasting just a few days. They claimed to have the world’s first public airport and it cost a fortune (seemed like a fortune to me) for a taxi into the city until I discovered that carefully not advertised at the airport was a high-speed, clean urban railway which from memory cost 40 cents. I have always been delighted by socialism in the USA.

Land use in 1948 would have been predominately from a pre-car society and the cities expansion to 2002 reflects car ownership. It would be interesting for an Aucklander to see how house prices change with distance from the city centre and school zones. I am betting the family fortune on the new million dollar houses on the outskirts of Auckland losing value and the decrepit house we live in maintaining its value because it is only 15 minutes drive or bus to the city. If Auckland had railways like Cleveland had 38 years ago then our housing and congestion wouldn’t be half as problematic.

I suggest Cleveland may best be compared to Greymouth in NZ; I’m guessing that Greymouth has inexpensive housing. My analysis is 38 years out of date. I will be interested if anyone else has a better more informed insight.

Racism toxic – but Tiger Woods playing golf creates record crowds and increases TV view figures and the most successful actor ever judged by tickets sold to watch his films is Samuel L Jackson who has overtaken Morgan Freeman. Race doesn’t seem to greatly handicap American singers either. When people are judged by talent not appearance then the world will be a better place (not exactly an original thought).

LikeLike

Wellington with 500k population on 8,000 skm compared with Cleveland with 2m population on 10,000 skm certainly point to sprawl minimising the land price component. But sprawl increases the infrastructure costs in delivering, repairs and in maintenance. Cleveland tops the list of most distressed city in the USA and the reason directly attributable to servicing the sprawling infrastructure.

LikeLike

Wouldn’t a 10% Drop in house prices render the banking system insolvent due to fiat leverage created? It’s not like more apples bring prices down applies to houses.

Richard Werner and Steve Keen must be wrong.

LikeLike

A 10% drop in the value of houses does not affect the banks balance sheet. It is not the value of houses that is captured on a banks balance sheet. It is the value of the lending that are assets on a banks balance sheet. The balance sheet only records the amount of Lending by customers of the amount owed but does not value the future income in today’s dollars. The actual future value of the lending assets is the future revenue from the interest receivable over the next 30 years. Therefore as long as jobs are plentiful and people are paying the interest on the loans then the actual sale value of the lending assets can be worth 10 times the balance sheet recorded value.

LikeLike

Apples can behave like houses if there is a supply glut. The price for those apples can rise quite dramatically. The difference is that you have a choice whether you eat the apple of you can choose alternative fruits and because it is prone to rot hoarding the apple is not an option. Having to sell affects price. With old people taking much longer to die and a hundred years now seem quite normal, there is a element of hoarding that drives prices, land of course being limited supply and together with increasing demand leads to increase in prices.

LikeLike

So money has a store of value then? I’m a truck driver with 120k I the bank that I earned from work. I don’t own a home. If houses collapse by 40% the money I have earned is not debased or devalued by that amount is that correct? Cheers and I appreciate your feedback.

LikeLike

I’m confused sorry. So when prof werner said a 10% Drop in house prices would make the banking system insolvent what did he mean? Is he wrong or did I not understand? The fact that if house prices retract people like me lose there jobs which I did I 2009 kind of proves that. I don’t wish to lose it again due to leverage and debt. Prices dropped slightly in 2009 and loads of people lost their jobs in my field.

LikeLike

Household House values at around 1 trillion dollars. NZ household debt is $175 billion. A 40% fall in house value would still leave housing assets of $600 billion.

The breakdown of households is as follows

33% of NZ households have zero debt

33% of NZ households have less than 50% debt

33% of NZ households have more than 50% debt

First home buyers are the most indebted representing around 25% of the 33% which makes the total percentage bank exposure around 8% of total bank debt.

NZ household debt is supported by NZ Household savings cash deposits which is $170 billion. NZ households also have listed share investments of $66 billion plus Superannuation funds of $95 billion.

The rest of the debt is mainly business debt. $60 billion in Farm debt, 150 billion in Business debt and another $60 billion in investment property debt which is funded by overseas savers borrowed through largely bonds.

New Zealanders have a huge amount of assets. It takes a lot of beating up to cause a NZ banking collapse. The argument is more whether we have been too focused on debt reduction at the cost of not enough infrastructure spending.

LikeLike

Hendo, unfortunately in 2009 the RBNZ engineered a collapse of the NZ economy by pushing interest rates in excess of 10%. It was not global events that caused our recession. It was a RBNZ mistake. Too aggressive and trigger happy with interest rate rises.

LikeLike

The Reserve Bank does fairly regular “stress tests” of the banking system. Their results suggest that the banks could cope with a house price fall of around 50% – and unemployment rising to 12% for a few years – with facing the sorts of losses that would threaten their viability.

LikeLike

Michael, I made a comment above. I’d like your expert opinion on it if you would. I am 38 and a truck driver with 120k in the bank. I do not own a home. If house prices collapse by 40% does that effect the value of my savings that I earned from work? I keep getting told owning a home is not a right. Does that indicate money has a store of value and my money will hold its value.

My understanding was money originates as an interest bearing debt. If banks created the deposits backed by assets like housing I though my savings would have no value as what backs my money has lost its value.

I’m not an expert at all but prof werner has same very good arguments as does steve keen. I’m not quoting them but I’m concerned about leverage and having my savings wiped out. Even if I put it under the bed to avoid obr it could still be debased.

Cheers

LikeLike

Steve keen said that stress tests on banks make it sound like when an engineer does a stress test on a bridge and decides it’s not going to fall over. But the bank tests don’t consider that one shock is not related to another. I’m confused so you can confirm that money has value and banks don’t blow up asset bubbles to fund economic growth thus forcing governments to increase immigration to deal with inflation and grow domestic consumption. Because all western countries have seen migration booms since 2011 as well as massive asset inflation? Are they related?

My theory is why gain 30kg of weight In the gym if you can’t lift more weight.

LikeLike

So all the capital gains leverage that banks lent out is factored in and collapse does not effect my 120k that’s good to know cheers.

LikeLike

The NZD has value because the international community gives it value. The NZD is the 11th most traded currency in the world with Singapore as the 12th. It is a sought after currency because it stores value. Our RBNZ is one of the most hawkish Central banks in the world keeping interest rates always higher than the rest of the world. The National government has chosen over the 9 years to aim for a budget surplus in the face of $20 billion Christchurch and $8 billion Kaikoura disaster recovery plus navigated the GFC. They squeezed every government department for every dime of savings to get to a budget surplus. Prior to that the Helen Clarke government also got 9 years of budget surpluses and paid off most of the governments foreign debt.

LikeLike

Reblogged this on The Inquiring Mind and commented:

Much of our housing issue stems from regulatory issues, coupled with lack of competition in building supplies

LikeLike

This from the Economist this morning (in an article on openness vs ‘closedness’). The idea of “regulatory tax” is interesting, and immediately recognisable.

“Towns where knowledge workers cluster tend to be plagued by strict planning laws which limit access to one of life’s necessities. The best data for this comes from the United States. In 1970-2000 construction costs in Boston and San Francisco rose by 6.6% and 5% respectively but house prices shot up by 127% in Boston and 270% in San Francisco. Edward Glaeser, of Harvard University, calculates that the “regulatory tax”, driven by restrictions on land use, is roughly 50% of the value of a house in Manhattan, San Francisco and San Jose. But it is clearly also true of Oxford and Cambridge where house prices are soaring, and getting planning permission is a nightmare equivalent to getting a PhD thesis.”

LikeLike

Thanks

Sadly it isn’t just a knowledge workers thing. Pittsburgh does very well on keeping house/land prices modest while our cities -knowledge worker clusters(eg wgtn) or not do very poorly.

LikeLike