In last Friday’s Herald there was a weighty supplement headed “Dyanamic Business”, reporting/celebrating the results of the annual Deloitte Top 200 (companies that is) business awards. It seemed to be an opportunity for mutual self-congratulation, bonhomie, and a bit of virtue-signalling thrown in as well (eg the MBIE-sponsored award for “diversity and inclusion”). And a few oddities as well: the award for “excellence in governance” went to a company that is majority state-owned and subject to quite real moral hazard risks (see 2001), and I don’t suppose the Reserve Bank will have been best-pleased to see the chair of Westpac New Zealand Limited – the subsidiary just last week subject to Reserve Bank sanctions for failures of governance – as a runner-up the “Chairperson of the Year” stakes.

But what caught my eye flicking through the supplement was this table for the top 200 (non-financial) companies in New Zealand.

| Annual % growth 2016/17 | |

| Revenue | 4.3 |

| Pre-tax profits | -6.4 |

| Tax paid | 22.7 |

| EBITDA | 2.9 |

| Assets | -5.7 |

| Equity | 2.9 |

(Tax aside) those numbers didn’t look very impressive. Total revenue was up 4.3 per cent (and the accompanying article says that in the previous year revenue actually fell). Profits and total assets actually fell, and both EBITDA and total equity were up by 2.9 per cent.

And what happened to the whole economy? The Top 200 numbers use the latest audited accounts of each company, so there is a mix of balance dates. But in the year to June 2017 (the latest quarterly data we have), nominal GDP rose by 5.9 per cent. The last annual national accounts came out late last week: on those numbers, nominal GDP has risen 6.2 per cent in the year to March 2017, and 5.1 per cent in the year to March 2016. Against that backdrop, the performance of the top 200 companies was, if anything, surprisingly weak.

Big companies, in aggregate, doing less well than the economy as a whole needn’t be a concern. It could, after all, be a sign of thrusting new companies surging ahead and displacing the tired old giants. But there isn’t really much sign of that sort of process in at work in New Zealand – see, for example, the tech sector. And, of course, our overall per capita growth in real GDP (let alone productivity growth) has been pretty deeply underwhelming.

In a way, a simple list of the top 10 most profitable companies (dollar value of profits) is quite revealing:

| Fonterra |

| Spark |

| Air NZ |

| Ryman Health |

| Kaingaroa Forest |

| Auckland Airport |

| Transpower |

| Z Energy |

| Meridian Energy |

| Mercury |

Of those 10, we have four majority state-owned companies (one a natural monopoly), a chain of petrol stations, a property-boom play, and a co-op whose profits are largely driven by swings in global commodity prices. There wasn’t much new or very dynamic about it. In a way, the list of top 10 money-losing companies looks more interesting – in addition to Tasman Steel (No 1) and Kiwirail (No 2), it does feature Xero and Orion Health.

It is a very different list than, say, one of the top most profitable non-financials in the US, which does feature (relative) newcomers like Apple and Alphabet (Google) and where almost all the companies have a strong international focus.

I mentioned those new annual national accounts numbers. No doubt I’ll be using the numbers in various posts in the next couple of months, but for now just a couple of charts.

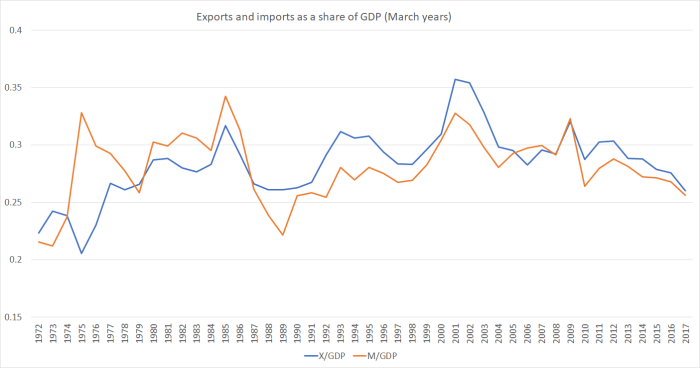

I’ve noted in various recent posts the fall in the export share of GDP over recent years. There was always the hope that some of that might have been revised away when the annual numbers were published. But no.

As a share of GDP, imports haven’t been lower since the depths of the recession in the year to March 1992. Exports haven’t been lower, as a share of GDP, since the year to March 1976 – more than 40 years ago. There was, so it was claimed, a policy focus on increasing the outward orientation of the New Zealand economy. If so, it failed.

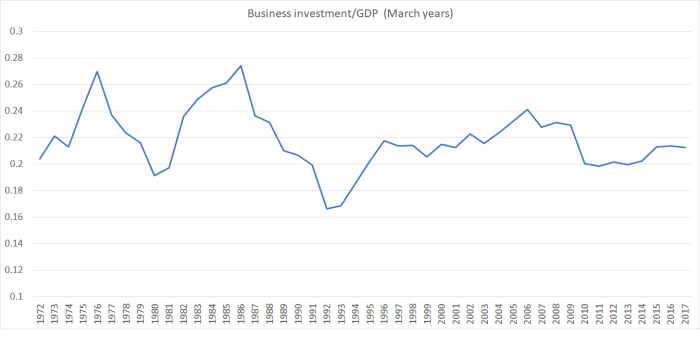

And what of business investment as a share of GDP (as previously, this is total gross fixed capital formation less government and residential investment)?

It picked up a couple of years ago from recession-era lows, but has gone sideways since, and is nowhere the rates reached in the previous expansion.

When profit growth in our top 200 companies has been relatively subdued perhaps it shouldn’t be surprising that not very much business investment is occurring. And those export/import numbers shown earlier strongly suggest that what business investment is occurring will have been disproportionately concentrated in the non-tradables bits of the economy, those that don’t (be definition) face much international competition.

Deloittes and the Herald might think this is a “dynamic economy” – and I’m sure there are plenty of small exciting firms in it – but once we stand back and look at the aggregate numbers the picture isn’t very encouraging at all. If change is constant, the change here seems – in aggregate – to more akin to drifting slowly backwards.

That was the legacy of the now-departed National-led government. That government’s policies were not, in relevant areas, materially different than those of the previous Labour-led government. The worry now is whether there is any realistic basis for expecting something different, and better, from the new centre-left government. At present, it isn’t obvious why the future should be any better than the performance over the last 20 years or so.

Fascinating summary, thanks!

All credit to Air NZ – amazing performance in a truly internationally competitive free market. To have come from the near bankrupcy situation under which the Clark/Cullen Labour government made the re-purchase in 2001 makes the story even more deserving of merit.

And of course it trades on brand NZ – something to my mind we are putting at tremendous risk due to poor governance of our society/environment across the board (i.e., local governance/planning, immigration settings, environmental governance, etc.). If we continue to trash this brand no amount of pretty brochures will make a difference.

And what a curious world it is with Xero in the top 10 money losers.

LikeLiked by 1 person

Air NZ has clearly benefited from the higher immigration settings currently another record net gain of 72,600 off a gross of 126,000 arrivals a year. 19 million inbound and outbound passengers out of Auckland Airport every 12 months certainly helps the bottom line.

LikeLike

Of course, it isn’t necessarily a problem that Xero is losing money. They have been on a massive growth path, and it cost a lot to get established in new markets, find new customers etc etc. A parallel, in that respect, is Amazon which didn’t make any money for a long time.

Xero remains a fascinating case study. It looks like a great product, and looks like it should be able to build a profitable business, but if it does – and that is still an “if” – what are the chances it will remain NZ-based in the longer-term. Not high I’d have thought (especially now that Drury has sold his shareholding down so much – no doubt prudently from his own perspective).

LikeLike

Navman did the same. The better the company the less likely they will hang around in our little backwater.

LikeLike

Xero has just reported a $5 million profit and at the same time announced the departure from the NZX.

LikeLike

Xero also highlights how expensive equity capital is. Rod Drury basically has been forced to sell out his company in order to access equity capital to expand the business. With the lack of depth in NZ capital markets growing companies have to move to offshore capital markets. NZ companies either have to stay small and grow organically or to use debt in order to grow their businesses. The cost of debt in NZ is one of the highest in the OECD therefore eroding margin and decimating bottom line profit which then forces the company onto international equity markets.

Note that there is nothing in there that indicates immigration is the cause of Rod Drury’s shift to Australia.

LikeLike

I (largely) agree, although (a) the high cost of equity in NZ is substantially about our high interest rates, which in turn are driven by population/savings pressures, and (b) if companies like Xero that succeed (and there aren’t many) can’t economically stay here, it is insane to keep using policy to bring ever more people here.

LikeLike

“Our banking sector is amongst the most profitable in the developed world. Four foreign-owned banks control 87 percent of New Zealand’s banking industry — a situation ratings agency Standard & Poor’s describe as “oligopolistic”.”

Click to access Repurposing%20Kiwibank%20%28Green%20Party%20Policy%29.pdf

LikeLiked by 1 person

I am not sure that screwing the regions and using their monopoly position to undercut start-ups is such great management – or especially good for NZ. Cullen made a huge mistake bailing out AirNZ. We would have a much more competitive industry if he let it go like Swiss Air etc.

LikeLiked by 1 person

Air NZ is a prime reason why selling state assets is actually not a bad thing. We sold Air NZ at a premium to mainly Temasek Holdings the Singapore Central Provident Fund investment company. At the time Air NZ had a monopoly on landing rights in NZ which made the company highly profitable. We then decimated the company by opening Air NZ to competition by allowing a free for all landing rights to all other airlines. At close to receivership and mounting losses, Michael Cullen bought it back for peanuts, recapitalised and now a very valuable and profitable company again ready for another sale. Brilliant strategy. Goes to show that there is nothing wrong with selling state assets, we own the country and can change the rules of the ballgame in our favour. No wonder the US wanted the rights to sue the government in a international court under a TPP agreement.

LikeLiked by 1 person

Xero has quit the NZX and is now pretty much an Australian company. This is due very much to the lack of depth in the NZ capital markets and splitting the listings has also split the capitalisation size of the company which has inevitable led to them combining the NZ shareholders and the Australian shareholders into a much bigger company now listed on the ASX as they launch into the US market. Looks more like a marketing exercise and certainly presents a larger and therefore more credible Australian Tech company to potential US clients.

LikeLike

Interesting and rather gloomy. It would be fun to open your blog on a Monday morning and read “everything is looking good – off to the beach for the rest of the year”; fun but uncharacteristic.

Looking at the top 10 performers and they all could crumble. Synthetic milk, the list of major airlines that went from hero to zero is long, solar panels continue their price trend and cheap battery storage and in a few years we might not need a power generators or national grid (it would be like all those blue chip railroad companies in the US during the fifties with savvy investors dumping their shares early) and so on.

LikeLike

Apropos your comment re Solar energy and Battery Storage

The Governments 49% exit out of the generators and retailers was an obvious overt strategic decision. Such was commented on elsewhere, at the time of the floats so it’s nothing new. Cynical but true.

LikeLike

It was certainly a very good strategic decision by the National government to be exiting large power generation and retailing of power. I had thought that a complete exit would have been better for taxpayers in the longrun with the capital profits put into taxpayer subsidies of the use of Solar energy and electric cars ie hybrids at the time.

LikeLike

In fairness, one could probably do a “they could all crumble” analysis on the top 10 companies in any country – look at the vicissitudes of IBM, ICI, Pan Am etc etc.

I’m hoping to get to the beach this afternoon, altho just as well i don’t wait for the good news – my whole life would have passed by!

LikeLike

Sometimes companies are so solid with such a depth of valuable assets that the only way they can fail is new management.For example the tragedy of Arnold Weinstock’s GEC and Burns Philp .Apparently Howard Hughes had no interest in his inherited Hughes Tool Company and that all his business ventures came to sticky ends except Hughes Tool Company just kept generating profits. More relevant to me was Bank of Scotland that was solid for 200 years until they choose new dynamic managers.

The best bets on our top ten would be Auckland Airport because politics would stop any potential competitor (If an airport depends on tourism then it ought to be in the South Island) and Ryman Health – their profits could dry up but their assets should be OK – but then again I’ve no idea how they are financed.

I once made the mistake of swimming in Lyall Bay – don’t do it, we need you back here tomorrow.

LikeLike

You must have become a “soft Aucklander” – we not only swim at Lyall Bay (mild by Wgtn standards) but at our very own freezing cold Island Bay

(and then look forward to rea holiday in the Bay of Plenty)

LikeLike

Burns Philips? The new management was I thought Graeme Hart who poured in $400 million and almost lost the entire lot when he found that the valuable assets he purchased was worth nothing? He managed under aggressive new management turned the company around and off the back of that success managed to secure $1.7 billion in loans for more acquisitions and now he is worth tens of billions?

LikeLike

Compare the make-up of the top 10 companies in Australia versus New Zealand and it becomes evident why NZ companies struggle to compete against overseas products – energy costs in Australia are around 20% of gross costs – NZ energy costs for the big industrials are controlled by contract – for the middle to small they are larger

LikeLike

Interesting in light of Bill Gallagher’s speech. We don’t know dollar wise about Gallagher’s but its odds on the their result is way better per capital and other measures than many, including your list. (As Tait electronics were).

But when he points to a large part of the problem he gets vilified by the very people who exacerbate the problem. The Nats. spent so much time and money appeasing a small sector of the community that the rest became the forgotten.

Its a tough world out there and as along as we live under the false pretenses that we do and the distortion it creates to operating an efficient economy we will remain poor.

https://www.stuff.co.nz/national/politics/99271744/sir-william-gallaghers-privileged-and-partial-view-of-history

LikeLike

And even ‘tax paid’ is unlikely to be the actual tax paid. It is more likely to be the accounting tax expense. Which like the crime rate to the prison population – is only a loose correlation.

https://letstalkabouttaxnz.com/2017/06/19/no-accounting-for-tax/

LikeLike