Alex Tarrant, at interest.co.nz, has done a couple of interesting interviews, one each with the current Minister of Finance, Steven Joyce, and with the man who would replace him, Labour’s Grant Robertson. There are various things in each interview that I might comment on in the next few days – including in particular Robertson’s comments on his plans re the Reserve Bank.

In the interview with Joyce, this blog even got a mention, as the Minister was forced to concede that five years of no productivity growth (at least as measured at present) might perhaps be something that should be taken seriously.

“Productivity has been a struggle everywhere. If you look across the eight years – and let’s be clear, these people that talk about productivity measures over a year, they’re really…”

I cut in: former Reserve Bank economist, and Croaking Cassandra blogger Michael Reddell’s talking about the last five years, when productivity growth has been negative by most measures.

“Five years is getting more like it,” he accepts. “The thing about measuring productivity is it’s generally measured more effectively a couple of years after the fact, which is very frustrating for those us who are focussed on it,” he said.

So now, apparently, we are reduced to just hoping that the last few years’ data end up revised away? Maybe……

But today I wanted to focus on Joyce’s comments around the New Zealand export performance and the government’s export target, partly because on this occasion he has articulated his perspective more fully than I’ve seen previously. Here is the heart of that section of the interview

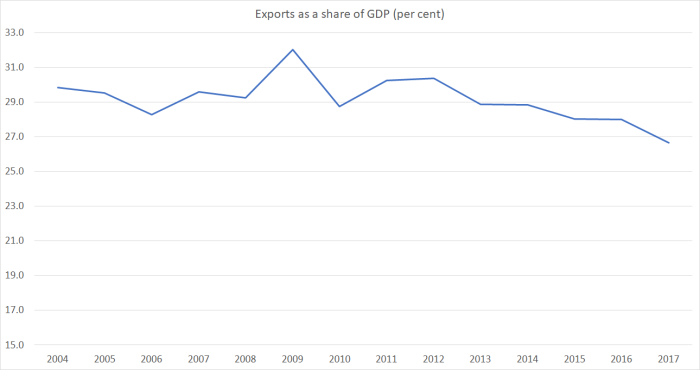

I ended by putting a couple of numbers to Joyce – one was on the goal to increase exports as a proportion of GDP from 30% to 40% by 2025. It hasn’t shifted from 29% since 2008. Is he disappointed?

“I’d like to see more growth in that.” He couldn’t really have said much else. “But you have to go and look at what’s been happening under the hood. And under the hood, world trade intensity has dropped.

“So, if you look at New Zealand relative to say, your Singapores, your Denmarks or so on, which are the big traders, they’ve gone back a bit, because we’ve had an extended period of a decline in world trade,” he says.

“We’ve held our own. Again, it’s nothing to write home about necessarily, except that we haven’t slipped back the way other countries have.”

Another thing New Zealand had been dealing with was our biggest export had been “down a bit of a hole over the last two or three years,” Joyce said (about dairy).

Actually, Tarrant’s introduction is a bit generous. Exports as a share of GDP in New Zealand were 29.2 per cent in the year to March 2008, rose quite a bit when the exchange rate plummeted in the following year, but were down to 26.7 per cent in the year to March 2017. The last time the export share was lower than that was 1990.

What of the Minister’s claim about what’s gone on in the rest of the world? It isn’t entirely clear how relevant it is to New Zealand anyway, given that the government has set, and regularly updated, the New Zealand target, including in the Business Growth Agenda refreshes as recently as this year. But set that to one side for the moment. What do the data show, and how do we compare?

For the whole world, the best source of data is the World Bank. Often it is only available with a bit of a lag.

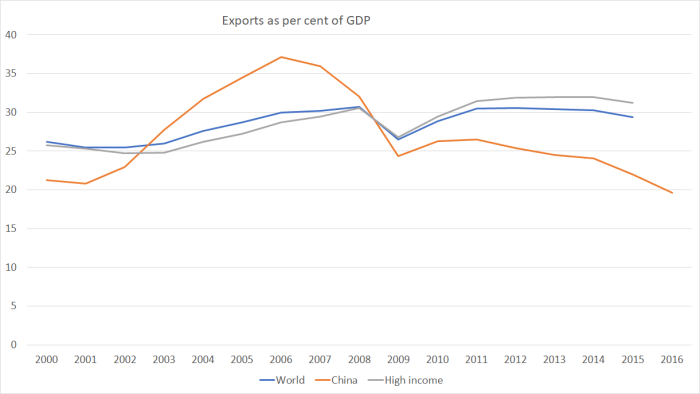

For the world as a whole, exports as a share of GDP have indeed dropped slightly since 2007 or 2008. But that is very largely a China story – after a couple of decades of very strong export-led growth, the story of China in the years since the 2008/09 recession has been a domestic credit and infrastructure phase. The foreign trade share of GDP has fallen back a long way – and is probably still above what would expect in the long-term for a country the size of China. For high income countries (a World Bank category) exports haven’t grown markedly as a share of GDP, but they have grown. Of the Minister’s other examples, Singapore’s export share is very high and quite volatile, and has fallen back somewhat – as I illustrated in a post a few months ago, they’ve had a huge increase in their real exchange rate – but Denmark’s hasn’t.

The usual group we compare New Zealand against is the other advanced economies in the OECD. Here is how New Zealand has done relative to the median OECD country.

The shifts aren’t dramatic but (a) we’ve done less well than them, and (b) we were the country whose government set a target for a dramatic change.

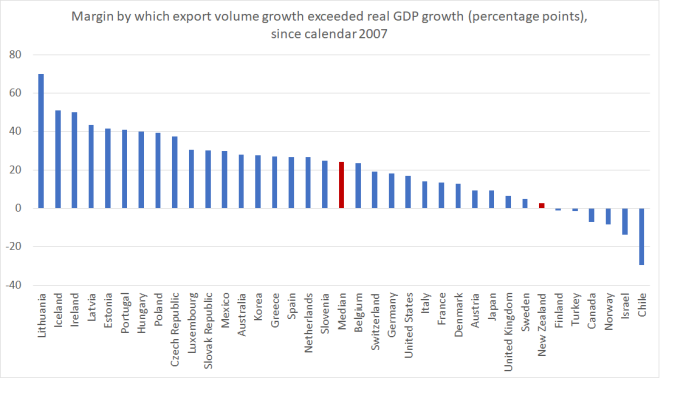

If we use calendar year 2007 as a reference point (the last full year before the recession), there are a few countries whose (nominal) export share of GDP has dropped by materially more than New Zealand’s. They are Chile, Israel, and Norway. Of them, Chile and Norway have experienced very substantial falls in their terms of trade – sustained falls in copper and oil prices. By contrast, New Zealand(despite the ups and downs in dairy prices) and Israel have had the largest increases in the terms of trade of any OECD country over that (almost) decade. All else equal, a rising terms of trade should have tended to lift a country’s export share of GDP relative to those in other countries (matched, in time, by a higher import share of GDP, as the proceeds of the better prices are spent).

All of these numbers to date have been measures of the nominal value of exports relative to nominal GDP. The government has expressed its export target in terms of volumes. As I’ve noted before, ratios of real variables don’t make a lot of sense, and Statistics New Zealand advises against using them. But one way of looking at volumes that does make some sense is to compare the volume growth of exports to the volume growth of GDP over a reasonable period. In this case, I’ll look at the most recent year (to March 2017) relative to that last pre-recession year, calendar 2007.

In this chart I have calculated the total percentage growth in the volume of exports since 2007 and substracted from that the total percentage growth in real GDP over that same period. (It might be more proper to do this multiplicatively, but I’ve checked and it doesn’t change the rankings.)

There are OECD countries that have had a weaker relative export volume performance than New Zealand over this period, but not many. And the median country’s experience is very different than ours has been. And that is even with all those subsidised additional education exports and (as the Opposition parties might note) additional unpriced water pollution and methane emissions associated with the growth in agricultural exports.

Recall too that the whole logic behind the government’s export target was about closing some of those income and productivity gaps to the rest of the advanced world. As Mr Joyce noted elsewhere in that same interview “productivity has been a 30 to 40-year issue for New Zealand” (longer than that actually). One of the ways in which sustainable success of an economy tends to manifest is in the ability of firms based in a country to sell more stuff successfully abroad, enabling us to purchase more stuff from them.

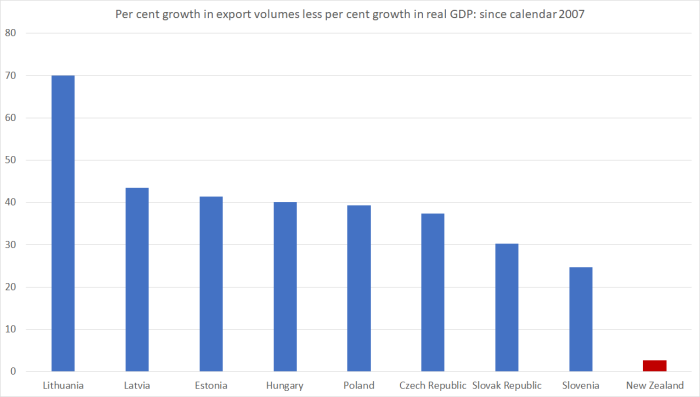

In a post the other day, I highlighted our experience relative to a bunch of other countries that had been setting out to catch up, eight (now) fairly-advanced central and eastern European former communist countries.

Here is how (nominal) exports as a share of GDP have done in New Zealand and in those countries since 2007.

and here is a chart showing the gap between the growth rate of export volumes and the growth rate of real GDP (again, latest 12 months compared to calendar 2007).

And, drawing this towards a close, in case anyone was hoping (against hope) that the services sector might provide a more encouraging export story (death of distance as technology advances etc) here is the chart of how services exports as a share of GDP have done.

But no.

Were I trying to make a case for the defence, I would highlight two relevant considerations that Steven Joyce didn’t mention:

- first, the impact of the Canterbury earthquakes. Real resources have had to be used for the repair and rebuild process that simply couldn’t be used elsewhere (eg to build export industries), particularly as much of the cost was covered by offshore reinsurance (which gave people cash, but not more real resources to do the rebuilding with). As that phase passes, resources will be freed up and we might expect them to flow back towards the tradable sectors of the economy,

- second, the unexpected sharp and persistent reduction in interest rates which (for a country with a large private external debt) represented a considerable windfall. We have been able to consume more without having to produce (or export) more. It is a windfall, but in the longer-run it is no substitute for a policy climate that supports productivity growth and the growth in both the export and import share of our economy.

And, on the other hand, you might have noticed that I mentioned earlier that Israel had been somewhat like us. Exports as a share of GDP had fallen further than in New Zealand, and the terms of trade had increased over the last decade by about as much as New Zealand’s had. The other thing that constantly marks out Israel is the rate of population growth, from a mix of high (but falling) birth rates and high rates of immigration. Israel’s population has increased by just over 20 per cent since 2007 (New Zealand’s population has increased quite rapidly by international standard, but “only” by about 12 per cent).

Just like the earthquake story, real resources required to build the considerable infrastructure (houses, road, offices, factories, schools etc) associated with a rapidly growing population aren’t available for growing other industries. In New Zealand’s case that rationing process works through a persistently high real exchange rate and real interest rates persistently high relative to other advanced countries. I’ve written previously about Israel’s underwhelming long-term productivity performance, and suggest that, as with New Zealand, rapid population growth in an unpropitious location, has made it hard for firms based in either country to take on the world (economicially) and succeed. The experience of recent years – remember, no productivity growth at all in New Zealand for five years now – looks like another straw in the wind in support of that suggestion.

Relative to the government’s target, export performance in New Zealand has been poor. Relative to other advanced countries, it has also been poor. And all that notwithstanding very favourable terms of trade. Exports aren’t everything by any means, but the only OECD country in the last decade that has had a worse overall export performance than New Zealand and had a good terms of trade has been the one advanced country with a consistently faster rate of population growth. Export volumes have grown quite a lot in the last decade – just over 20 per cent – but they’ve barely kept up with overall GDP growth (in most countries, there has been much more export volume growth), and even then only through new subsidies (export education) and unpriced environmental externalities. It is a flawed strategy. And it is an unsustainable one.

It is our over reliance on the primary sector that has been our downfall. For many decades our NZ economists have misdirected our productivity investments as having more cows and growing more food. 90% of our primary produce is exported. I still remember our silly NZ economists calling milk, white gold.

We do not need to produce so much food as our small population does not need it. We are just subsidising other countries food production requirements with free irrigated water, and excessive methane gas, polluted waterways which we will have to fund for some other countries food requirements.

LikeLike

I wonder about the use of the metric of export share of GDP. What if GDP goes up a great deal and exports stay the same? Then the share is reduced. The metric alone does not tell us the complete picture. I would be interested in how absolute export earnings have changed. My own experience as an exporter is that indeed trade dropped a lot in October 2008, and has still not recovered.

LikeLike

The volume of NZ exports is up about 23% (yr to March 2017) over calendar 2007, while real GDP rose 20% in that period.

In nominal terms (ie straightforward, non-deflated, NZD terms) exports are up 33% and GDP up 44%.

As I noted in the post, total exports have risen quite a lot, but (on the volume measure) 23 of the OECD countries managed faster growth than we did (and almost all had slower population than we did). It just isn’t enough, despite the “subsidies” – export education – and unpriced environmental externalities.

LikeLike

With Dairy export revenues dropping from a high of $15 billion to $11 billion due to the fall in dairy prices by 50%. You would expect a fall off in export revenue against total GDP. If you compare that with the fall of oil prices and what that has done to countries like Venezuela. NZ economy is actually very resilient. We have to thank John Key for that as Tourism Minister. National Party and Prime Minister pulled NZ out of a very nasty recession engineered by a reckless Allan Bollard when he senselessly drove the OCR to 9% and interest rates to above 10% when the rest of the world was facing a GFC.

LikeLike

Perhaps you missed my observation that of all the OECD countries we (and Israel) had the largest increase in our terms of trade over the last decade or so. That is “increase”. Sure, there has been plenty of volatility in individual sets of prices, but overall the TOT have been a tail wind, helping us over the decade.

LikeLike

I guess that’s my point. Exports are up = good. GDP is up = good. Export share of GDP is down = bad. It’s a conflicting narrative. There’s no stone tablet with any edicts on it about export share of GDP, why even use the metric for anything?

LikeLike

It isn’t sensible to use it in isolation. After all, one can get exports/GDP up with export incentives, or by crashing the domestic economy. So one has to read it together with other indicators. Our GDP per capita growth hasn’t been great over the decade, and our productivity performance (GDP per hour worked) has been really bad over the last five years in particular. If, as successive govts state, they want to close those income and productivity gaps, history and cross-country experience suggests that that is only likely to happen when, as part of a successful overall strategy, exports/GDP is rising (thru market forces – not subsidies). Indeed, that is the logic behind the govt’s target, so I’m trying to address them on their own terms.

LikeLike

International students and Tourism which is a growing $15 billion export industry feeds back into the local domestic economy. The conversion rate is 100% from export GDP to local domestic GDP. All other export industries like Dairy, Meat, Wine have only about a 30% conversion rate to local domestic GDP. It is mathematically impossible to have an export revenue increase in a booming International student and Tourism sector outstrip GDP in the local domestic sector.

LikeLike

I found your post very interesting. I may have missed something, indeed I am sure I probably have, but what impact did manufactured goods have on the overall statistics as compared to agricultural?

LikeLike

SNZ only release export components (at the national accounts level) for “goods”, “services” and “total”. Same goes for the way the OECD presents natiional accounts data (for the cross-country comparisons). The more disaggregated data are around in various formats, but I’m not so familiar with them (my macroeconomic biases showing). I might see what i can dig out for a post at some stage.

LikeLike

I would like to see more journalists talking about the impact of the capital account, and national savings, on export performance.

LikeLike

….agree; liberal capital flows are worthy of investigation e.g. the flow of money into NZ ‘land’ markets vs. businesses over the past decade? no one has a Scooby Doo (clue) but even the IMF has suggested capital controls are less evil than once thought; funny how China cottoned on to this many years ago…

LikeLike

China, of course, remains hugely poorer (per capita) than the more liberal economies of the West…….

I’m more sceptical of any (adverse) macro effects of open capital markets. The pressures in NZ – high real exch rate and high real interest rates – are largely the result of domestic choices, and real resource pressures, rather than autonomous global forces.

But national savings choices are a different matter. Lower than average saving rates tend to raise real exchange rates (relative price of non-tradables to tradables).

LikeLike

Hi Michael, again you have very clearly articulated the issues but what are the best policy responses?

NZ to me seems to be in a catch 22.

a) We are already some of the most efficient farmers in the world so the marginal productivity gains would seem limited for NZ overall

b) NZ faces risks with agricultural emissions, synthetic meat, and disease outbreaks

c) Our economy is so small that domestic firms in other sectors struggle to reach economies of scale to be able to expand overseas successfully. I can think of numerous failures.

d) The deeper capital bases and larger economies of scale have seen many NZ firms being taken over by Australian firms. We are effectively a state of Australia whether we like it or now.

e) We need a larger domestic economy if our other sectors are to get to economies of scale which implies high immigration of which we are currently seeing the downside of (high real exchange rate, high house prices, infrastructure deficit).

f) Alternatively, as you have suggested we seek a low immigration rate and try & maximize gdp per capita growth off the back of our current productive sectors – that has some risks like b)

g) NZ will always face the tyranny of distance issue, although the growth in tourism has partially compensated.

h) Even for online selling of NZ products we would need to be selling boutique niche products unique to NZ so that we are not outdone by the air and sea freight costs.

So in terms of policy responses?

1) Lower immigration rate which will lead to lower real interest rates and lower currency boosting exports competitiveness

2) Adjust the tax status (land tax?) of housing to increase incentive for more NZ savings to into shares etc, increasing the NZ capital base

3) Personally I’d like to see kiwisaver made compulsory – while I don’t like compulsion its human nature to (over)consume. This would increase available savings to go into the capital base (housing equity in reality is locked up and would seem to really only be available as capital to small businesses, not business which are going to grow to international scale)

4) Reduce the taxation on savings with a risk free rate of return

5) Negotiate as many free trade agreements as NZ can

6) Have a trade & enterprise office in every overseas country

7) ??? what else does NZ need to do

LikeLike

Not so sure about “the most efficient farmers in the world” – there is a great article in the latest National Geographic about Dutch agriculture.

Mostly, I’d just start with your 1). That would, through the lower interest and exchange rate, also make it more feasible to price water use, regulate water pollution, and (for those who care about such things) price methane emissions, without severely compromising the competitiveness of the farm sector. We might perhaps have come close to “peak cow”, but James Shaw’s talk of a 30% cut in the number of cattle is a recipe for reduced material living standards.

With a relatively static population, we’d see more resources devoted to exporting. in some cases, capital intensive agriculture (see Holland), in some cases tourism (again appropriately priced), but also some of the other manuf and services sectors would be able to overcome the disadvantages of remoteness and succesfully export from here.

On tax, my ideal would be a shift to a progresssive consumption tax. Short of that I favour a Nordic system – lower tax rate on capital income than on labour income. I don’t have a great in-principle problem with a land tax, but with global longer-term real interest rates still near zero (see US 10 yr), the feasible rate of tax is so low that (a) there isn’t much revenue in it, and (b) any price impacts will probably be quite limited. Land, after all, in Akld is so highly priced that AKld local rates are increasingly approximating a land tax already (the land component of the capital value is so large).

I remain a bit sceptical of preferential trade agreements, for reasons outlined in post when TPP was still alive. https://croakingcassandra.com/category/tpp/

LikeLike

Great post, Michael. I think you’ve demonstrated another hole in National’s election spin about how well we’re doing.

LikeLike

How is it a hole when Labour is planning to use Nationals hard earned surpluses to spend on Jacinda’s pet projects?

LikeLike

Very useful analysis, thanks. Not good, by any measure. I always thought it a ridiculous target – all puff, no plan. Surely the answer has always been innovation through science, but not science directed at a volume/commodity sector. In other words, it seems to me all the money/emphasis put on reducing methane emissions in ruminants is an entire waste of time, as the end product of all that innovation isn’t an innovative end product.

LikeLike

3% annual increases on GDP, a fast growing economy is much better than Jacinda’s tax on investment property, tax on shares, tax on business sales, tax on inherited property, tax on the holiday house. The previous tax working group wanted a tax on unrealised capital gains. Looks like Jacinda wants to tax unrealised capital gains as well.

LikeLike

Michael

I suspect that were you to call tourist income an export then your figures would tell a quite different story and it would be one that would make English/Joyce look a great deal better.

And really, is there any practical difference (in a GDP sense) between exporting to China and having 400,000 Chinese come to NZ and spend $2B here?

Tim

LikeLike

But Tim, tourist income is already fully included in those export numbers – the largest chunk of our services exports. In a sense, that is the disconcerting point: for all the recent genuine upsurge in tourism, services exports in total had been so weak in the previous decade that as a share of GDP even now they are below the levels of 15 years ago. By contrast, in almost every other OECD country the share of GDP accounted for by services exports has increased over that period.

LikeLike

All your comparative tell me is that New Zealanders are more likely to spend and convert Tourist export dollars to domestic GDP than other countries which is a great effort by the government rather than to ship those export dollars overseas. Perhaps other countries have more phillipino maids/workers that transfer their billions earned back to the Phillipines.

LikeLike

What??????????? (apart from anything else, the earnings of temporary workers count in the GDP of the country they are working in. Remittances are a different issue – a transfer abroad, or a use of GDP – and never show up as an export.)

LikeLike

Exactly, thats why service Export GDP in many other countries it does not show up in Domestic GDP because it is not spent in that country but transfered out to be spent in another country. In NZ clearly Export GDP is spent entirely in NZ and very little is transfered out. Thats why export GDP in NZ against total GDP is declining.

LikeLike

In my recent book Innovate! , I present a detailed analysis of the state of our fifteen export – focused sectors, their prospects for growth, current thinking on being innovative and how our government supports exporters. I find that our advanced manufacturers, the key to genuine technology development of economies, are being threatened by new manufacturing technologies and processes, and by large multinational companies who are adapting their businesses to tackle the very niche markets that our manufacturers supply. I also find we have exciting but unrealised opportunities in medical technologies, ICT, textiles, and in minerals developments, but our manufactured food, agritechnology and biotechnology sectors are fragmented and underperform. I assess our sophisticated exporting sectors to be fragmented, that there is little real growth, that the science and innovation system that supports them is outdated and ineffective, and that opportunities for new investments are being missed. In short your analysis supports what I see out there.

Richard

LikeLike

Michael

Thanks for that piece of info about tourism’s inclusion in the export basket. That does rather leave the export figures looking pretty lame.

It’s hard to escape the conclusion that NZ’s poor rate of non residential investment is the culprit.

I note our own propensity to prefer allocating capital outside of NZ rather than at home.

It feels as if NZ’s level playing field isn’t enough when compared to better growth and scale opportunities elsewhere.

Tim

LikeLike

Of course, I”d argue that our “level playing field” isn’t – despite intentions – level, in that it is delivering the highest real interest rates in the advanced world, and a persistently high (out of line with the underlying competitiveness of the economy) real exchange rate. That skews things against business investment generally (which has been weak for decades as % of GDP) and particularly against investment in the tradables sector.

As another economist recently put it, “the business of Akld is (largely) building Akld”, and sadly it isn’t so far from the truth for the economy as a whole (the “building” bit more than the Akld-specific ref.)

LikeLike

Michael

I’d be totally aghast if the level of interest rates had any appreciable impact on investment.

I do think the RB rules are making credit a bit harder to get, but generally the issue isn’t the supply of debt or equity. It’s a lack of investable propositions. NZ’s small scale opportunities and the cost and delay caused by regulations adds a layer of overhead which is quite discouraging.

It will be interesting to see if the Government in October has a real effort at considering ways to lift this key metric

Tim

LikeLike

TIm

Any effect will always be hard to identify. In cyclical terms, interest rates tend to be high when the economy is cyclically strong and investment opportunities are relative more abundant, and my story has been that the interaction of rapid population growth (needing lots of investment) and modest savings rate helps explain why real interest rates have been persistently higher than those abroad.

On the other hand, a typical project evaluation exercise will use some sort of hurdle required rate of return, and typical cost of capital calculations will start from a risk-free interest rate (which for NZ based investors is materially higher than for investors in most other advanced countries).

My own read of the data is probably that the more important interest rates channel is indirect: the effect on the exchange rate, and hence on expected returns from investment in the tradables sector. That is certainly consistent with the data I’ve shown before – and will update next week when the GDP numbers come out – showing no growth in real per capita tradables sector GDP since around 2000.

And of course that brings us back to your “investable propositions” point. There would be more of them if the real exchange rate was materially lower, and the real exchange rate would be materially lower if the population growth were not, on average, so rapid. In such a world fewer real resources would need to be devoted to eg housebuilding, and more would probably be used in more outward-oriented industries.

I’m not optimistic on change after the election, whichever side wins. If anything, if the left wins the risk is more downward pressure on exports/GDP, because of the impact of increased environmental regulation and pricing agricultural emissions. Those might be in some sense good things to do, but when the price of agricultural products is set globally, regulatory changes locally can only undermine the competitiveness of the ag. sector unless they are offset by a sustained reduction in the real exchange rate. That is partly why I’ve argued that both environemental and economic aspirations would both be materially helped by markedly slowing the average rate of non-citizen immigration. Getting the real exchange rate down is a critical element in dealing effectively with those challenges. The NZD will no doubt fall a bit if the left wins, but it is a 20% fall, not a 2% one, that is really needed.

LikeLike

Other evidence that the pool of investible funds in NZ is too small includes: chronic current account deficit over decades, the small number and tiny size of NZ institutional investors, the deficit on investment income and (anecdotally) higher hurdle rates relative to European and Asian investors.

LikeLike

playing devil’s advocate just briefly, the counter would be that the ratio of NIIP/GDP has been going sideways for 25 years now, so the average current deficits are just consistent with a stable net (external) debt position.

LikeLike