I had only a limited number of specific comments to make on the details of the Reserve Bank’s Financial Stability Report released yesterday. But it is the last such report for the outgoing Governor Graeme Wheeler, and that itself prompts a few other thoughts.

The Bank continues to tout the line that monetary policy in much of the world is “very accommodative” – relative to what benchmark is never clear – and yesterday they claimed that

“a sustained period of very accommodative monetary policy has supported the long-awaited recovery in global economic activity”

That seems questionable on multiple counts. First, the recovery or growth phase has been underway since at least 2009/10. There have been setbacks and what felt a little like “growth pauses”, and the overall experience has been pretty underwhelming. But there also isn’t really much sign of that changing for the better.

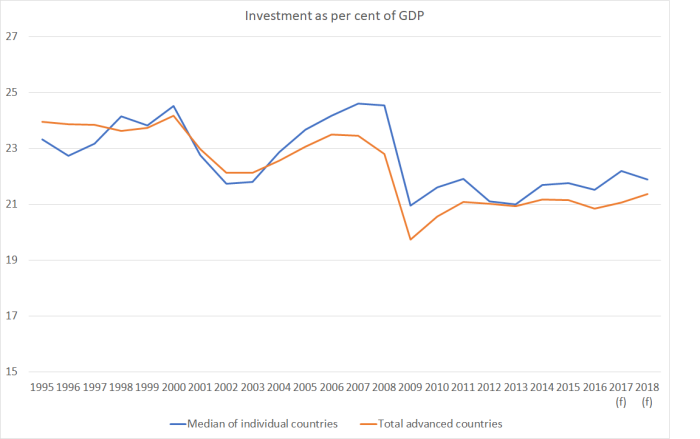

And since what the Bank calls “very accommodative monetary policy” has been concentrated in the advanced economies, one obvious place to look for upbeat news might be investment spending. Lower interest rates, all else equal, make investment today more attractive than otherwise. But here is the IMF data – and the IMF is the Bank’s standard reference point for comment on the wider world – for investment as a share of GDP in advanced economies.

The latest actual data – for 2016 – are still below the cyclical lows in the early 2000s. And if investment isn’t picking up strongly, neither is the IMF picking a slump in savings rates to support an acceleration of demand.

Across the advanced world, there just isn’t much consistent sign of anything very different in the next few years than we’ve had in the past few. That suggests interest rates are low for a good – if not fully-explained – reason, rather than just that monetary policy is “very accommodative”.

At one level, the terminology doesn’t matter very much, but coming from a central bank offering insights on financial stability, it doesn’t suggest that they really have a good sense of what is going on. They might be in good company on that score, but it isn’t exactly reasssuring. If you don’t have a good “model”, the prognostications might not be of much value.

I also found it rather surprising that there was almost nothing in the Financial Stability Report – the major statutory document on financial stability issues, including the Bank’s conduct of its various regulatory responsibilities – on the recently-released report on New Zealand under the IMF’s financial sector assessment programme (FSAP). It was a major independent report, which seems to have also involved a substantial commitment of resources by the New Zealand authorities (including the Reserve Bank), in some areas it reached conclusions quite different from current policy, and yet it is barely mentioned in the Bank’s own review. It isn’t because they didn’t have time – the papers were released to the public three weeks ago, and the Bank will have had them well before that. Perhaps it isn’t yet time for a definitive responses to all the points, and some of the issues the FSAP reports raise are really for the government rather than the Bank to decide, but…the silence was deafening. Perhaps the Bank thought the IMF report really wasn’t much use at all, and was simply being polite? (I would have some sympathy for such a view, and will before long have my own post on some aspects of the report.)

And there was something a little odd in the box the Bank included on “Vulnerability of owner-occupiers to higher mortgage rates“, clearly softening us up for the consultation paper on debt to income ratios. They argue that

New Zealand is particularly vulnerable to a sharp rise in mortgage rates as the banking system funds a large proportion of its mortgage credit from offshore wholesale markets. The cost of this funding can increase sharply if there is an unexpected increase in global interest rates or a change in investor risk appetite, and banks are likely to pass on the higher funding costs to customers through higher mortgage rates.

But mostly this is just untrue. The Reserve Bank sets the OCR in New Zealand based on overall inflation pressures in New Zealand. If funding spreads rise – as they did in 2008/09 – and domestic inflation pressures don’t the Reserve Bank can easily offset most or all of the potential impact on retail interest rates by lowering the OCR. That is what happened in 2008/09.

Of course, retail interest rates can rise, quite materially. As the Bank points out, new floating mortgages rose from “around 7 per cent to over 10 per cent between early 2004 and 2007”. Of course, as we used to stress at the time, fixed mortgage rates rose nowhere near that much. But, more importantly, interest rates here didn’t rise because foreign rates were rising, but because the economy was cyclically strong, unemployment was low and falling, and wage and price inflation were increasing. Wages rose roughly 20 per cent in that period.

It is fine and good for the Reserve Bank to do these sorts of stress-testing exercises, looking at what happens if interest rates rise to 7 per cent, or 9 per cent. But in any realistic assessment, those sorts of substantial increases are only remotely likely if the economy is doing really cyclically well. If jobs are readily available and wages are rising, not many people will be under that much stress even if interest rates rise quite a lot. And those that are should quite readily be able to sell their house and move on. It might be painful for them, but it simply isn’t a financial stability event.

There was some good news in the report. Previous stress tests conducted by the Reserve Bank with the major banks have used very severe adverse macroeconomic shocks (in some respects – notably the critical unemployment assumptions – beyond anything ever seen in a modern floating exchange rate country). Banks came through those tests largely unscathed. So this time, the Bank did something a bit different.

The most recent regulator-led exercise was a ‘reverse’ stress test completed in late 2016. This test required the largest four New Zealand banks to determine the most plausible scenario that would lead to a breach of a minimum capital requirement. The results highlight that severe risks would need to materialise before this would occur, beyond the sustained macroeconomic downturn assumed in a typical stress test.

It was another way of reaching the same conclusion the previous tests pointed to: our major banks appear to be strong, and well-managed. The Reserve Bank is quite explicit that the regulatory regime is not a “zero-failure” one – in a market economy, firms will fail sometimes, and that includes banks – but with the sorts of loans the banks had on their books late last year, the latest stress test suggests (again) that it would take something almost inconceivable for one of them to fail.

Which does leave one wondering, again, quite what all the fuss has been about in the last few years, with successive rounds of LVR controls, and the forthcoming consultative document in which the Bank tries to persuade us (and more importantly the Minister of Finance) that it should be able to impose debt-to-income limits too. When it discusses the world economy, the Bank is quite fond of invoking concerns about “policy uncertainty”, but what certainty and stability has it provided in the markets/institutions it regulates in recent years? And to what end has all the uncertainty been?

The Bank likes to claim that its successive interventions have ‘improved the resilience of the banking system”. In fact, they offer us no evidence on that score. No doubt, as their data show, the number and value of high LVR loans on the books of banks have both fallen. But high LVR loans require banks to hold higher amounts of capital, and loans that are just below some regulatory threshold, supplemented perhaps by other forms of credit (eg family support), may be only very slightly (if at all) less risky than the loans the banks would have made in an unconstrained world. The Bank’s claim would be more convincing if (a) they directly addressed the clear and simple point that lower risk lending also lowers the amount of capital banks have to hold (so that the risks might be lower, but so are the buffers if things do turn bad), and (b) if they ever addressed the question of what banks do instead of the high LVR housing lending they are now largely barred from. Banks’ own risk-appetite probably hasn’t changed, and neither (probably) have the return expectations of their shareholders, so have they pursued other types of risk. FSR after FSR the Bank never engages with this fairly straightforward point. It also never engages with the question of how direct controls, frequently revisited, better advance the efficiency of the financial system than indirect mechanisms (primarily the capital requirements for banks, which don’t interpose government regulators directly between banks and their customers).

Perhaps there are good and convincing responses to these sorts of points. The Wheeler Bank has never even attempted to provide them.

I’m also uneasy about the Bank’s treatment of the housing market. They have a long list of various factors that play a part at various times in influencing house prices. I’m pleased that they quite openly state the obvious point – well, it should be obvious if we didn’t have business think tanks and government-funded researchers arguing that opposite – that when housing and urban land supply is less than fully elastic, strong net migration inflows can and do boost house prices.

But, for an organisation that has chosen to intervene repeatedly, and which weighs in every six months with an assessment of the risks around the stock of housing lending, they don’t seem to have anything very authoritative to offer. They have never once noted that land use restrictions – not just here, but in a variety of similar countries – could make urban land prices permanently higher. Without major changes to those laws, other interventions – taxes, LVR restrictions, government housebuilding programmes, and even immigration restrictions – will typically only make a modest difference for a relatively short period of time. And there are no natural market forces that will undo those restrictions – they aren’t like a temporary credit bubble. When bank lending standards deteriorate rapidly, there is good reason for people who have lent to banks (and for the regulators) to worry. When governments enable pernicious land use restrictions, there are plenty of reasons for many to worry – notably the young, who might struggle to ever get a place of their own – but it isn’t much of an issue for financial stability regulators (in that climate, higher gross credit is mostly just an endogenous response). And yet, for all their interventions, the Reserve Bank has never been able to give us an authoritative story (“model”) on what role the various possible explanatory factors are playing now, and have played over the last 25 years.

I can imagine that the Reserve Bank is uneasy about wading into what can be a rather political debate. I can understand that. But if you are a government agency actively intervening in a market – itself a highly “political” choice, favouring some groups of potential buyers over others – you have an obligation to show us your robust supporting analysis. The Reserve Bank simply hasn’t done so thus far. Perhaps the robust cost-benefit analysis in the forthcoming consultative document will be different?

And, years on, there is still no robust analysis or research suggesting that the Reserve Bank has thought hard about what the important differences might be between countries where banks’ domestic loan books got into serious trouble and those where they did not? In 2008/09 for example, New Zealand, Australia, Canada and the UK saw quite different things than the United States and Ireland did (and even those two latter experiences were themselves quite different). It seems like a pretty elementary line of inquiry – and we do, as taxpayers, pay for a lot of researchers at the Reserve Bank – but there has been just nothing. In the meantime, people who are regulated out of credit markets pay the price.

If the Bank doesn’t know the answers to these sorts of questions, perhaps they need to be rather more agnostic about the outlook and the case for their own direct policy interventions in the market. Focus on stress tests and capital requirements, and eschew direct interventions which have little economic foundation, and are arguably ultra vires anyway.

These are now mostly challenges for the new Governor. Both Graeme Wheeler and his deputy (and Head of Financial Stability) Grant Spencer are leaving shortly – Wheeler in September, and Spencer next March. I hope the new guard takes more seriously some of these issues. If they do, writing FSRs will be harder, but there would be a great deal more value in the resulting documents even if, in many cases, the resulting analysis leaves as many questions as answers. That might simply reflect the limits of what we know about the world (and housing markets, housing finance, and banking risk).

Earlier in the year, the Minister of Finance intervened and instructed the Board of the Reserve Bank to stop their search for candidates for a new permanent Governor, and instead to recommend a candidate to be a temporary (acting) Governor. Doing so avoided trespassing on conventions which restrain governments from making major permanent appointments which would take effect around the time of general elections. Deputy Governor, Grant Spencer, was – with what still looks like little secure legal basis – appointed acting Governor for six months, allowing whichever government takes office after the election to make the appointment of a permanent new Governor.

You might have thought – I did – that such a temporary appointment was designed to leave the new government free, and also not to tie the hands of the new Governor. An acting Governor would make the decisions that really had to be made, keep a steady hand on the tiller, and otherwise leave substantive decisions until a permanent appointee was in place next year.

But it seems that Graeme Wheeler, and the Reserve Bank’s Board – the latter perhaps still smarting at having to end their earlier search process – didn’t quite see it that way.

With Spencer stepping up to acting Governor, and then retiring when that term ends, there was going to be a vacancy in his substantive roles. There were two of those. One was the fulltime day job as Head of Financial Stability (a role in which three departmental heads report to him, covering financial markets and financial stability/supervision. And the second was the statutory position of Deputy Chief Executive.

A month or so ago, there was a press release from the Reserve Bank filling both positions. The other current Deputy Governor, Geoff Bascand, was to transfer from his current role (oversight of the operations and admin sides of the Bank) to become Head of Financial Stability, and he was also promoted to become Deputy Chief Executive. In addition, a search process would get underway straightaway to fill Bascand’s role (adverts have subsequently appeared, and applications have already closed).

Frankly it all seems rather odd. For a start, even though Bascand has no background in banking, financial markets, or the regulation of those activities, there was no sign that any sort of competitive or contestible process was undertaken before he was appointed Head of Financial Stability.

But it also looks like an attempt to box in the new Governor, whoever he or she may be. Sure, it is common for a chief executive to inherit a senior management team – although often enough that is a prompt for a (often disruptive) restructuring etc to allow the new person to shape his or her own team. Moreover, the qualities one might want in other members of the top team surely depend, at least in part, on the skills, experience, and other qualities of the person at the top. A more obvious (and common elsewhere) solution would have been to have appointed an acting Head of Financial Stability and then let the new Governor make his or her own choice about the sort of structure and people they want in the roles. For example, it might be fine to have a macroeconomist as Head of Financial Stability – key point of contact with senior people in the financial sector and other regulatory agencies – if the new Governor has a strong banking background. If not, it might be a lot more problematic, especially given how large and prominent the Reserve Bank’s regulatory role now is. (Of course, if Bascand himself becomes Governor, that issue solves itself.)

These points are more important than usual given that talk of statutory reform of Reserve Bank decisionmaking is in the air. Labour and the Greens are committed to change, and the government has had Iain Rennie looking at the issue. Again, depending how those matters are resolved (including those around the Bank’s financial regulatory powers), it could easily influence the sort of person one wants in key senior management roles. (That includes the Assistant Governor position they are filling now. For all Graeme Wheeler’s talk of the key role of the Governing Committee in making key policy decisions in the Bank, the advert for that position, had hardly any mention of monetary policy and, from memory, none at all of financial regulation. In many respects that makes a lot of sense – while the Governor in law actually makes those decisions – but perhaps not if the Act was to be changed to make a holder of this position a statutory decisionmaker on major areas of public policy.)

And then, of course, there is question of whether all of this was even lawful. In the Reserve Bank Act, the role of deputy chief executive is filled by the Board on the recommendation of the Governor. But there is no vacancy in the role of deputy chief executive while Graeme Wheeler is Governor. And, even though the press release was worded as coming from both Wheeler and Spencer, the Act does not talk of an acting Governor being able to recommend a deputy chief executive appointment. Perhaps it is a small issue, but details matter, and the law matters.

All else equal, I happen to think that Geoff Bascand would normally be a sensible appointment for deputy chief executive. I’m less convinced he is right for the role of Head of Financial Stability, and generally think he would be better-suited (despite his fling with LUCI) for the role of Head of Economics (a role which should have become much more important as the Governor has had to focus increasingly on the Bank’s various regulatory roles).

There is a public sector culture of generalist managers. I’m not sure it serves particularly well. Of course, Grant Spencer also had a background in macroeconomics but had also served as the Bank’s Head of Financial Markets, and then had almost 10 years in various relatively senior roles at ANZ in New Zealand and Australia. It wasn’t doing credit – perhaps the essence of banking – but it was much more of an exposure than Bascand has had (and the Head of Financial Stability job is itself much bigger than it was when Spencer was first appointed to it). Sure, Bascand has sat around the internal committees on regulatory issues for the last three or four years, but it really isn’t that much depth of involvement. And I say this even though, when I also sat on those committees, Bascand’s was often more willing to challenge and questions the interventionist inclinations of staff than many of his colleagues were. I welcomed that.

Perhaps he is the single best person in the country (or abroad) for the role. And there is something to be said, in high-performing organisations, for promoting from within. But the appointment has an uncomfortable feel about it, including the dimensions of Wheeler either trying to box in his successors, or give Bascand another leg up in the succession stakes.

And there is also the uncomfortable fact that, for someone soon to be charged with oversight and regulation of much of our financial system – regulating in the interests of the wider economy, not that of the banks – Bascand doesn’t exactly have a spotless track record. Defensive behaviour and an attempt to close down issues, rather than open them up, seems to be his style. There was his attempt to tar the whistleblower – me – last year when I alerted the Bank to what turned out to be a leak of an OCR decision and a systematic weakness in their processes. There was the seeming inability to distinguish between his (and others) role as trustee and as Bank employee – particular worrying to the Bank I’d have thought if a financial sector employee had a similar cavalier attitude. There was the attempt to close down, without substantive inquiry, significant complaints from a member of the Reserve Bank superannuation fund, only to find later that a breach of the law had occurred (and various other – still ongoing – issues identified), for which breach trustees later had to apologise to members. And, meetings with fellow regulators might be interesting, given that there is an outstanding complaint with the Financial Markets Authority – regulatory body responsible for superannuation schemes – around the decisions and processes adopted by the superannuation scheme trustees under Geoff’s chairmanship.

I know we don’t have depositor protection as one of the statutory elements in New Zealand’s banking regulation, but whether as a depositor or citizen I’m not sure this sort of track record would fill me with confidence in Bascand’s ability to lead financial regulatory functions, with the drive and willingness to leave no stone unturned that, in some circumstances would surely be required. Bankers will often be keen to close things down quickly, and paper over problems. The last thing we need is officials who will be content, or perhaps even complicit, in letting that happen. At very least, this was a decision the new Governor should have been left to make.

It’s not a great time to be without strong leadership. The international market environment is feeling a bit like 2007, and my spidey-sense is tingling.

LikeLike

Blair

What are the areas of similarity as you see them? Geopolitics certainly feels increasingly risky. Perhaps Chinese credit, altho that seems increasingly like an issue somewhat cut off from the rest of the world’s financial system? I guess US corporate debt levels have been rising, without that much investment or productivity growth?

There don’t seem to be nasty house price booms in places – like Spain and Ireland – that couldn’t control their own macro conditions, on the upside or the downside. And is there anything like the housing finance distortions that fed the rapid growth of poor quality housing lending in the US?

Anyway, interested in any thoughts

LikeLike

Low VIX, high asset prices, low interest rates, high debt levels in China and Australia, SHIBOR, geopolitical risk, and lack of fiscal headroom. In 2007 it slowly dawned on me that Wall St was not hedged the right way (they were holding the AAA tranche of the CDO’s which turned out to be most exposed to a general rise in correlation). In 2017 it is slowly becoming apparent the Chinese banks may not be hedged in the right way (local government debt, dodgy collateral, apparently diversity but underlying exposure to 1 asset class, etc). And the debts are so large even the Chinese central govt can’t absorb them all. And in Australia/NZ we have substituted made-in-China house price gains for actual wage growth.

I also see NSW will soon have a 15% stamp duty on foreign buyers.I’m enough of an EMH-er to think it’s not possible to pick a crisis in advance, but there are warning signs of a possible change in Chinese liquidity conditions that would materially affect some of its closest trading partners.

LikeLike

Thanks. Lack of monetary headroom is what scares me if something really does go bad,

LikeLike

China does not rely on external debt. Its banks are all owned by the Chinese government. Recently all capital outflows have been banned by the government which means no more capital outflows to buy properties offshore. There won’t be extensive runs on banks. The government can stop all bank withdrawals or take client savings or cease any assets if they wanted to. We tend to forget that China is not a democracy subject to laws. The government makes all law as it pleases. There is no such thing as a private citizen with private loans or private savings with rights bestowed to ordinary private citizens.

LikeLike

And your final sentence is exactly why holders of wealth quickly get extremely jittery quite quickly.

But I agree that domestic runs can easily be staunched. the loss of wealth is real nonetheless, and the exchange rate remains a real source of risk too. Another commenter noted that China has lots of reserves. It did – relative to the size of the economy – but the current levels are nothing special.

LikeLike

When the Yuan was under threat of a devaluation, the Chinese government intervened with burning a trillion dollars worth of those foreign reserves to prop the Chinese yuan which equates to buying yuan. In the past it would have been happy with a lower Yuan to boost exports. It does mean that exports is now not its primary motivation but acquiring foreign infrastructure assets is. A higher Yuan points towards lowering the cost of building the Silk Road.

LikeLike

yes, they “burned” a trillion of reserves. And now they are less well-positioned for the next wave of pressure whenever it comes.

Politics plays quite a role in currency politics. Especially now that Trump is in power, any material Chinese devaluation – even tho it might actually help China in theory – would risk sparking very nasty retaliation, in a pretty unstable geopolitical environment. And if the US were to lead, the EU might well be not far behind – since the competitiveness loss for EU firms would be just as severe, and the deflationary threat greater.

LikeLike

Given financial instability is (almost) inevitable, yet, unpredictable, being the ‘Head of Financial Stability’ seems somewhat an unfortunate position….

LikeLike

And because the episodes of instability are typically so far apart, it is also typically impossible to know whether the incumbent (whatever the title) has really done a good job.

LikeLike

chaps, the thing I don’t get re China debt fears is that it is mostly internal: she is creditor nation after all. So perhaps it goes the way of Japan but hard to see a domestic run on the Yaun unless faith in ‘the Party’ dwindles??

LikeLike

I don’t think the workout is predictable in China or anywhere else. Debts can be written off, inflated away or reallocated. However, based on Japan I think zombification is quite a likely scenario – as you correctly identify, the CCP doesn’t want to take a big bath, so it takes a long cold shower instead.

LikeLike

I think there are two risks: first an external run (despite all the efforts to restrict capital outflows) eventually leading to a devaluation (potentially disorderly), and the second is probably a version of Blair’s zombiefication in which weak Chinese demand becames a material drag on world economic activity (in a climate with little global fiscal or monetary headroom)

Chance of a Western financial crisis remain low, but the risk of another recession that we can’t do much about – except perhaps in NZ with an OCR still at 1.75% – has to be taken seriously. Who knows when tho.

LikeLike

….indeed – if you know, pays to keep it quiet! sort of understand – would of thought $3trn in reserves is quite a bit of firepower to counter external pressure and China continues to churn out a current account surplus; seems some want to dare a devaluation (which would only boost said surplus) after protesting currency manipulation – all above my capacity….!!

LikeLike

Don’t forget that China also launched the Silk Road belt to reduce time and cost of product to European, Asian and African markets. It has enormous infrastructure projects spending hundreds of billions occurring around the globe, buying up ports, opening up sea entry points and building rail land routes and they are attempting to raise the living standards and to grow a middle class in poverty stricken nations along that Silk Road belt so that their products continue to have a channel to market. There is nothing similar to a Japanese inaction causing the sort of decades of dead Japanese economy. China’s leaders are taking aggressive global business action and iniatives for new channels to market.

LikeLike

Regarding the FSR. I think I observed comments that the RBNZ noted not enough houses were being built. I wondered if you thought that related back to any of the RBNZ decisions? An unintended consequence – hope to improve stability, but make it worse by unintentionally boosting houses prices?

LikeLike

The RBNZ team is rather useless and really have not done their research or they are dumb and stupid. When you have a tightening of credit by forcing a 40% Equity on LVR, you effectively dry up credit. No credit no development. Development finance is available only after a threshold pre-sale activity is triggered. But you can’t start presale until you incur the cost of Resource Consent. Resource consent requires, architect plans and illustrations, land surveyor and pegs put in, topographical engineer, drainage engineer. First of all you have to buy the land. That purchase can cost $1.5 million for a 4 site subdivision. A simple 4 site land subdivision Resource Consent can easily cost $100k. It takes around 2 years to get Resource Consent. All this has to be funded by residential investment loans or 2nd tier financing which can cost upwards from 10% per annum.

LikeLike

I don’t think it is likely to be a major factor. The LVR controls certainly act to restrict demand for some classes of buyer but (for better or worse; I opposed it at the time, since new properties are often the riskiest hosing loans) loans for purchases of brand new houses aren’t covered. There is an argument that letting demand rip would have increased the gap between the price of existing houses and the cost of supply new ones, but that argument mostly fails because the inflation has been mostly in land prices, so when existing house prices rise so do the cost of supplying new ones.

By the look of it, the bigger issue is developer finance, which isn’t directly affected by RB controls at all, and bank funding costs (which is mostly about cost of offshore funding). Again, by the look of it, banks themselves had been getting hesitant around developer risks, in Australia as well as here. Whether they are right to do so isn’t clear – the case looks stronger in Aus than here, because in Aus there has been a stronger supply response and hence some risk of temporary oversupply – but if there is regulator involvement it might be more the indirect impact of APRA scrutiny than the activities of the RBNZ.

LikeLike

Michael, that’s not correct. I am actually doing a 4 site subdivision. The problem does not lie with development finance. All the banks will readily and easily lend 100% of the development on development finance with a presales threshold trigger. That’s the easy part.

The problem lies with funding the land cost and the initial Resource Consent which will have to come out of Residential loans. Especially where developers have been buying on 20% equity now find that if they want to borrow to start the development the equity requirement is now 40%. That stops the development dead in its tracks.

I am fortunate that I have started as a property investor which means that my land was purchased at $395k 12 years ago. Now it is valued at $1.5 million. The 40% LVR rule does not apply to me but if a developer is buying land today for a 4 site subdivision he would be paying $1.5 million. The bank in the past would have loaned based on 20% equity if there is a house to tenant. Land without a house will always require 50% equity.

Now the requirement is 40% equity which means to buy that land for development with a house, a developer will require $600k compared to $300k previously. Not many small developers have $600k lying around to even buy the land and start a subdivision.

My problem funding the $100k to get to Resource Consent to even start a presales process is because my income is not sufficient as I have 11 investment properties. Even though they are all positively geared as rents have risen over the years banks do want principle and interest paid. The principle repayments on 11 investment properties can be a hefty $60k a year.

When banks lend on a residential loan, it is on a 30 year repayment. This means that your income must be able to carry interest plus principle repayments.

LikeLike

Thanks for those very interesting and useful comments. I presume the pullback in finance for developers is more concentrated on (a) those looking to build big apartment blocks, and (b) urban periphery developers?

I’m still a bit puzzled as to how the RBNZ LVR limits impinge on a case like your own. Potential developers buying land aren’t directly affected at all, and neither are people looking to buy a new house/apartment. If anything, this bias in the LVR rules seems to favour people trying to sell new places over people selling existing houses/apartments. I fully appreciate that banks themselves have tightened their overall risk profile, but the bit I’d be grateful for clarification on is how you see the direct role of the RB controls.

LikeLike

On a 4 site subdivision in Mt Roskill where I already own the property it does not impinge on me. But it does impinge on me on my other development in Otahuhu where the new zoning allows for terrace housing and apartment development.

The otahuhu site allows 5 terrace units to be built on its own. However if I were to purchase the adjoining site the development allowed would be 15 units on the 2 sites. However, the vendor wants $1milllion to sell.in order to buy that land I would have to borrow on a residential loan. The RBNZ with 40% equity intervention means that I have to find $400k to buy that property on a residential loan. Previously all I needed was to source $200k to buy the adjoining property. So instead of building 15, I can only now build 5 units.

LikeLike