I’ve been pondering a post on land taxes for some time, but was prompted to jot something down today by a couple of recent pieces, including in today’s Herald by two lecturers in politics at AUT, Nicholas Smith and Zbigniew Dumienski. Sub-editors present their arguments under the headline “Land tax best fit for housing crisis”, and the authors’ own conclusion is only a little more nuanced.

Given the multiple problems stemming from Auckland’s housing crisis, an LVT stands out as the best-rounded of the policy options on the table. Not only would it address house price inflation, it could also result in a more efficient use of land, mitigate urban sprawl, lower the burden on the natural environment and reduce the risk of real estate bubbles; all without undermining the foundations of economic growth.

I’m not a land tax expert, but I’m no longer so convinced.

Which doesn’t mean that I’m inherently unsympathetic to the argument for a land tax. In fact, I once wrote a Treasury paper on overall economic policy direction, that ended up on Bill English’s desk, and which was, with hindsight, rather too readily enthusiastic about a land tax.

In principle, taxing things that are in fixed supply has some theoretical and practical appeal. Collection is pretty easy – every piece of land has an identifiable owner. And whereas if one taxes business profits (say) heavily there will be less investment taking place, taxing land won’t make much difference to how much land there is (it will make some difference because the value of land is partly about work done to it (drainage etc).

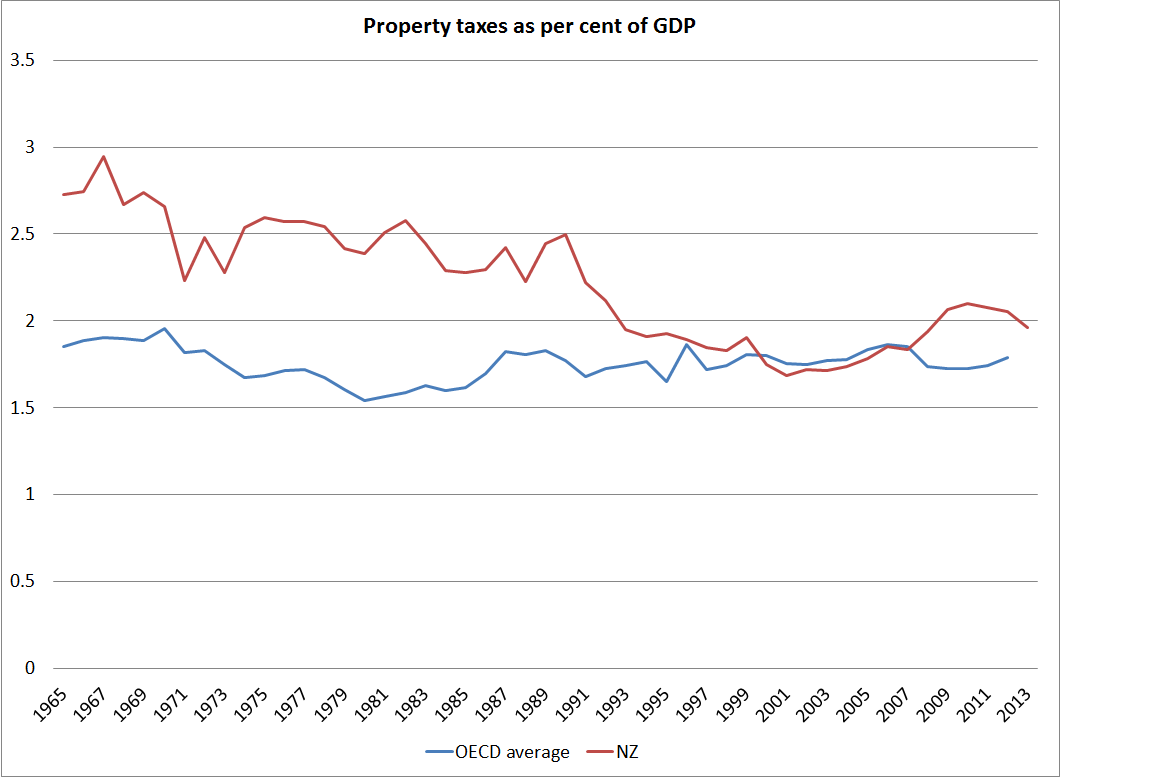

And, of course, as the authors point out we’ve had a land tax previously – it finally disappeared in the early 1990s, by when it apparently applied mainly to land under urban business districts. And we still have, in effect, some partial land taxes: in some areas, local authority rates are levied on the basis of land values, and in many places (especially Auckland) even the capital value rating system have come a lot closer to a land tax as the land share of a typical “house + land” has climbed sharply. And OECD data show the New Zealand property taxes, as a share of GDP, are already a bit above the OECD average.

Had we put a land tax on in 1840, and kept it in place ever since, I’m not sure I’d be arguing for abolition now. But the historical track record of the tax we had was not that good. Apart from anything else, the rules kept changing (and changing), with the base being progressively whittled down. Smith and Dumienski note that “it was arguably an important factor contributing to New Zealand’s once-famed egalitarian character”. I’d be keen to see the evidence for that claim. New Zealand economic historians, at least those I’ve read, don’t seem to have seen the land tax in quite those terms.

Any material change in the tax system involves significant redistributive consequences (or big compensation packages). No doubt there isn’t much public sympathy for “land bankers” in and around our cities (and since these people are mainly profiting from other regulatory distortions, I wouldn’t have much sympathy either). But what, say, about the sheep farmer, in an area where values haven’t been much affected by dairy conversion opportunities?

I’m also not quite sure what sort of tax rate the advocates of a land tax have in mind. People often glibly talk (and I have in the past) of a 1 per cent annual land tax as if this is a pretty small amount. But real risk-free returns are not what they were. New Zealand has probably the highest real interest rates among advanced economies and a long-term real interest rate here (20 year inflation indexed bond) is still just under 2.5 per cent. The comparable US yield when I checked this morning was 1.1 per cent, and that is now quite a common sort of rate internationally. People (especially central bankers) keep talking about interest rates “normalising”, but real interest rates have been trending down now for decades, and no one really knows with any confidence whether the process has ended, let alone whether it will be materially reversed. In this climate, a land tax of anywhere 1 per cent would seem quite incredibly burdensome (in a way that it might not have seemed in New Zealand in the 1990s when real risk-free interest rates were touching 6 per cent). Even if one could make a theoretical case for such an onerous tax, the political economy suggests that it could not be sustained (and would not be expected to be sustained).

Perhaps we could have a rather lower rate of land tax? Perhaps a half or a quarter of a per cent land tax could be politically sustained? But then one is left asking whether it is really all worth it. Bearing in mind that urban land is already taxed, would it make that much difference to the cost of urban land – the issue Smith and Dumienski are driving at – or allow a material gain in economic efficiency from shifting away from more distortionary taxes (eg lowering our high taxes on capital income)? After all, most people now agree that the real issues around urban land prices are not ultimately the tax system, but the regulatory restrictions on land use that central and local governments facilitate. To some small extent, those restrictions seem endogenous to land prices – ie when land prices get sky high (or least rise rapidly) there is pressure to ease the land use restrictions. If so, perhaps a land tax would just allow Councils to keep tighter restrictions in place for longer, undermining any possible efficiency gains from a land tax.

But let’s get back, in conclusion, to the Smith/Dumienski list of benefits. They argue that a land tax would

- address house price inflation,

- result in a more efficient use of land,

- mitigate urban sprawl,

- lower the burden on the natural environment and

- reduce the risk of real estate bubbles;

All without undermining the foundations of economic growth.

What’s not to like? Well, first, in principle a land tax should lower the value of land (ie a one-off shift in the price). But it is not obvious that it will have much impact on either house price cycles, or trend pressures resulting from, say, the interaction of population pressures and land use restrictions. Perhaps the authors have in mind some more sophisticated land tax that would effectively be a capital gains tax, but they don’t suggest so in their article. And as we know, real world capital gains taxes don’t appear to have done much to improve the functioning of housing and urban land markets

Would it result in a more efficient use of land? I suppose that depends on one’s model, but I’d have thought that taxing an asset will result in a more intensive use of that asset, with no necessary presumption that the more intensive use is more efficient. Of course, it might be less inefficient than the alternative possible taxes, but that is a different issue surely?

Relatedly, if land (across the country, not just in cities) is used more intensively, why is there a “lower burden on the natural environment”? Land in its natural state poses no such burden, but if (say) farmers need to use marginal land more intensively, to maximise profit subject to a land tax, I’m not sure why this is an environmental gain.

And I simply don’t see the argument made that to “mitigate urban sprawl” is an appropriate public policy objective. As is well known, urban areas in New Zealand make up a very small proportion of New Zealand’s total land area, and I’d have thought that revealed preference (reflected in prices) suggested that the most valuable use of land on the fringes of cities was typically for housing, rather than for agriculture. “Sprawl” is just the pejorative term for “space” – most people seem to want some (and historically as cities get richer they have gotten less dense) much though the planners might disapprove of their preferences.

To repeat, I’m not in principle opposed to a land tax, but I’m:

- sceptical that it could be imposed, in an efficient way, on an enduring basis

- sceptical that it would allow much effective tax system rebalancing

- and doubtful that, on the scale at which it could be imposed, it would really make much sustained difference to urban land prices, and trends in them over time.

There is no great secret to why New Zealand urban land prices are high. It is largely down to the impact of the central and local government regulatory restrictions on land use. Far better to tackle those at source, and give freedom back to landowners. Competitive market processes could then be expected to produce affordable houses, as they have in much of the United States (which doesn’t mean Mt Eden prices will ever be the same as Invercargill ones). Of course, one can reasonably argue that such reforms themselves might not prove durable, and if reform were totally “open slather” that would probably be true, but whether or not we have a land tax is simply not at the heart of the urban land price issues.

I’d welcome comments and thoughts on this issue, and if (for example) Andrew Coleman, at Otago, felt inclined to add one of his occasional, typically very insightful, comments drawing on his own past work (eg here) in the area I’d be very interested to read it.

If land banking/inefficient use of land is the problem, it would be easier in my opinion to counter that with a targeted rate which would be designed not to tax land across the board based on its value (which is essentially what a general rate based on land value does) but rather to tax land that is not being put to its most efficient use (in economic terms). I’m not saying get rid of the general rate (which I prefer seeing based on capital value anyway) but rather add a new targeted rate based on most efficient use – some properties would pay nothing (as the land would be deemed to have been put to its most efficient use) and others would pay the tax (as a sort of penalty for not putting the land to its most efficient use).

LikeLike

Interesting idea, but who is to determine whether land was being used in the most economically efficient way, and against what criteria? The risk is that it opens the door to lots of lobbying, and corruption of one form or another.

LikeLike

Proximity to centres of employment, in most cases a CBD (the bigger the centre of employment, the larger the factor for the tax to be applied). The rate would be applicable to residential zoned land only. The formula would include already existing measurable things – distance to CBD, number employed in the CBD, number of individual unit dwellings per square metre of land in the property title. Those wishing to sit on large plots of land near centres of employment pay the targeted rate – those moving to green field sub-division further out from the centre don’t – multi-unit dwellings near the CBD don’t.

LikeLike

So you suggest cutting down all the Kauri trees in the Waitakere Ranges because it is not the most economic use of land? Plenty of land there to build on.

LikeLike

A lot of land is zoned residential in the Waitakere Ranges. With the recent changes to tree protection council has to physically tag a tree if it is intended for preservation. The recent saga with a developer that tried to build 2 houses and had to remove a single Kauri. What happened there? Council approved the tree felling but the community objected with Helen Clarke joining the fray.

So now you are saying that any land that has a tree will get a land tax reduction? Sounds like a nightmare land tax policy?

LikeLike

The big assumption is that investors land bank because they want to make more money in the future. That is a fallacy.

I have a plot in Otahuhu. It has been rezoned for highrise under the Housing Accord as a Special Housing Area. I got a letter in the mail from Council notifying me of the rezoning.

Problem

1. Road frontage requirement of 25 meters. Most residential properties have only 15 to 18 meters road frontage

2. Viewshaft height limits. The area is zoned for 6 level of building but because it is sited close to a sacred mount, the height has been chopped to 4 levels.

3. 3 metre distance from boundaries for level 1 and level 2, 5 metre distance from boundaries on level 3 and level 4 to preserve neighbours BBQ patch of sunlight.

4. Minimum carpark requirements. Every apartment requires a single carpark Every 2 bedroom apartment requires 2 carparks.

Suddenly it is very uneconomic to build and you want to slap a land tax on top because it has been rezoned for apartments that can’t be built??

LikeLike

ggs, no, if you are referring to the open space zones/reserves of the Waitakere Ranges – as they are not part of the residential zone such a targeted rate would not apply. If a regulatory impediment to further unit title development (in a RZ property) exists for a particular parcel of land/title (say a tree(s) is protected by a plan) then the planning GIS database (from which the data for the targeted rate is calculated) would be able to pick that up and apply an exemption. GIS is a really powerful tool.

LikeLike

A lot of land is zoned residential in the Waitakere Ranges. With the recent changes to tree protection council has to physically tag a tree if it is intended for preservation. The recent saga with a developer that tried to build 2 houses and had to remove a single Kauri. What happened there? Council approved the tree felling but the community objected with Helen Clarke joining the fray.

So now you are saying that any land that has a tree will get a land tax reduction? Sounds like a nightmare land tax policy?

LikeLike

ggs, is Otahuhu a large centre of employment? How big in comparison to the Auckland CBD? Such a tax is a matter of degree – in some cases there would be little or no tax. The tax has nothing to do with whether or not a property has been re-zoned for apartments/multi-story dwellings or not. In fact, all that type of consideration would become unnecessary. Proximity to the CDB (i.e., centre of employment), m2 of the property and number of dwellings on the property are the factors associated with the formula – also recognising any impediments to development imposed by planning.

LikeLike

Yes, its proximity to Slyvia park shopping mall and the industrial estates of Highbrook, Mt Wellington, Penrose also Otahuhu has its share of light and heavy industry including the 500 staff employed on a single state of the art factory site owned by Wilson Hellaby Proteins.

LikeLike

PS. IMO the Auckland house price situation has to be viewed and treated as an asset bubble – fueled by immigration policy combined with hot money coming in from offshore combined with local government funding issues (i.e. the reason you set an urban limit so that you can manage the targeting/concentration of infrastructure/costs). I don’t know whether taxation should be used to remedy an asset bubble as I think throughout history the market eventually sorts that out. I’ve also thought that one thing central government has done in terms of interfering with market price in housing (and to a degree the containment of wages as well) is the accommodation supplement – and it just keeps growing ($2 billion annually at this stage).

LikeLike

The accommodation supplement is to the benefit of tenants and not a landlord subsidy. The government makes a choice with that $2 billion. They can buy and own more properties and face the regular annual maintenance costs but the bigger problem is the political fallout from the removal of these social welfare tenants once they have lived there for a number of years it gets more and more difficult for the government to administer as tenants start to believe that they have a right to be housed in the same house until the grave.

That is why we have million dollar state houses on 1000sqm with a single tenant because it is not so easy to move them to make the land higher density once they have lived there for a number of years. Private landowners can and will remove tenants and scale the economics of that land accordingly. You do not need property taxes as profit is a bigger motivator. Taxes just punishes and makes it more difficult to create supply.

LikeLike

Given the land use restrictions, I think all the factors you list have contributed. Not sure I’d call it an asset bubble, or at least not a credit-driven one. After all, few of the cities with tight land constraints have ever seen prices fall back sustainably. But the US cities show there are ways of coping with rapid population growth without the house price pressures – and, in many cases, ensuring the infrastructure costs fall on those who generate them.

I’ve stayed clear of commenting on the AS because I don’t know enough of the detail about it. Given that real rents have not been rising very strongly, I’ve been wondering how much of the AS expenditure is just because the govt has chosen to reduce the size of the state housing stock (relative to population). If so, it is just transferring cost from one bucket to another (and it would be much clearer if we went back to market rents for all state housing, with accommodation supplement based on need regardless of whether one was in a state house or a private rental).

LikeLike

The one thing that you can rely on is that if there is a margin, developers will build. Land tax unnecessarily places a cost burden on uneconomic or marginal land. Valuers do not separate flat land where the build cost is lower and sloping land where the build cost is significantly higher. Therefore in order for development to occur on marginal land prices must rise. The higher prices rise the more development will likely take place.

Usually, the more expensive the land the economics is to build more and to build higher ie you get economies of scale.

The problem with Auckland is that you have height limits due to viewshafts on 57 sacred mounts. Viewshafts cover extensive areas of Auckland which limit highrise and therefore limit economies of scale.

LikeLike

Aha, the Georgist argument. I’ve never been entirely convinced by it. It seems to me it’s more about the banking rules relating to using land value as collateral. Presently the marginal loan reserve on a $100,000 residential loan from the Aussie banks is something like $2800, maybe less. Rising lending causes rising land prices which creates more collateral in a bank management friendly runaway feedback loop until the income stream of the population can no longer afford the payments.

To me the solution is to adjust the reserve requirements upwards, I mean 2.8% is a joke, but that apparently is what the risk adjusted weighting gives you. The present level of house prices in NZ does rather resemble a Ponzi scheme as the loan to income ratios mean that the interest can be paid but not the principal without finding a greater fool to buy the house off you.

As you know I think the high level of household debt rather makes the RBNZ the pet poodle of the Aussie banks – forced to modulate interest rates to a level kiwis can afford to be miked at.

I’m trying to charicaturise the situation here but it’s unfortunately not entirely untrue.

LikeLike

This seems to rather reinforce my argument:

http://www.smh.com.au/business/banking-and-finance/committee-hears-of-commonwealth-banks-82-billion-fraud-20151113-gky7df.html#ixzz3raempcmc

The Aussie banks are quite happy to bankrupt viable SME businesses because the Basel rules make it worthwhile for them.

LikeLike

“As a result of a combination of the “risk-weighted assets” system and the credit crisis, banks have basically withdrawn from the thing they were set up to do: facilitate commerce.

For the big four banks, only 16 per cent, on average, of a real estate mortgage is counted when measuring the bank’s capital ratio. This is rising to 25 per cent next year.

But every dollar of an unsecured personal and business loans counts against capital and in some cases the risk weighting is 150 per cent.

Capital — that is, the bank owners’ money — has to be 8 per cent of assets, although mostly it’s around 10 per cent. That is, the ratio of owners money to other peoples’ money has to be no greater than 12.5 to 1 and is usually 10 to 1. The result is that for every dollar of capital, the big four banks can choose to lend $62.50 secured against real estate or $10 unsecured.”

https://www.thincats.com.au/news/

LikeLike

We don’t need a separate land tax on top of rates.

Just adopt a land value based rating system as recommended by the productivity commission.

This incentivizes land developers to develop rather than land bank which tightens the land supply further.

If the land is marginal developers can appeal against a new urban zoning a Council tries to impose. If they want to bring the development forward they can seek a private plan change.

LikeLike

Indeed, we already have a land tax. It is called rates.

LikeLike

And the increment is 10% this year but has not led to any more houses. Why? because a tax does not lead to more houses, it just leads to higher rents.

LikeLike

I’m a fan of flipping from overall capital rates to land taxes, but I’m not delusional about how much good they can do. At the margin, they reduce the cost of putting up taller buildings downtown because you won’t face a big rates increase for having intensified your land use. It would hardly fix everything in the world, but it helps at the margin.

The more fun tweak would be council assessing land taxes on Crown-owned land, and vice versa, so that governments might be a bit less likely to let valuable downtown land sit as underused surface parking lots.

LikeLike

Yes, generally I favour land value rating, altho in some ways I think the case might be less compelling for tall buildings (after all, local authority rates are partly about paying for service provision, and the 30 storey building probably [but I’m open to evidence] uses more services than a two storey one does.

Certainly agree that Crown land should face local authority rates – both on “equity” grounds (why should a local council suffer if the Crown owns land rather than rents it) and efficiency.

LikeLike

It’s important to note that the use of land value versus capital value as the basis for setting the General Rate for residential properties is almost a moot argument (if the objective of a “land tax” is to encourage efficiency of land-use and/or land-use intensification), as I believe the General Rate is becoming over time a much smaller proportion of the overall rates on a residential property given the trend toward greater use of targeted rates (i.e. including fixed costs for some services), UAGCs and user-pays funding models.

For example, where my rates are concerned, the General Rate component is only 60% of my total rates bill (I live on a full – that is, able to be in-filled – section, in the most expensive land-value residential area and the rating basis is a land value one).

If capital value were instead used as the basis for calculation of the General Rate on my property, that percentage of the overall total would likely go down but only a bit (about $200 on a $3,400 total) for me. Meaning, if this Council were using capital value and proposed to introduce land value as the basis for calculating the General Rate – and they wanted to target my neighbourhood for more intensive development, the extra $200 pa I might be faced with paying under a land value General Rate, wouldn’t likely incentivise me enough to either move off of and/or subdivide this land.

LikeLike

Thanks

Curiously a shift from capital to land value rating would make much more difference if we ever actually had a housing market like Houston or Atlanta, in which land value were a much smaller share of the typical house plus land price (I think Demographia talk of something around 20% as a normal benchmark level). In that world, land value rating would impinge quite heavily on those with unoccupied, or relatively lightly utilised, land.

LikeLike

Indeed. Actually, I’ve always been against dollar value being used as any part of the basis for calculating rates – as I think the public re-valuation of all property on a three-yearly basis is a large part of the rising cost of housing. In other words, if the only way to get an idea of the market value of a property was to obtain a private valuation when you are either a seller or a buyer, we’d have had a lot less price inflation. The problem is RVs (to my mind) largely set/fix the “bottom-line” expectation of most sellers. And with rapid house price inflation – that “bottom-line” expectation seems to have moved to a RV+x% type equation. This is not a good thing in terms of a properly functioning market.

LikeLike

I cringe everytime someone brings up Houston and compares with Auckland. Houston has an area of 26,000skm with 3 major international airports, a population of 6.3 million and a museum district that receives 8 million visitors a year. The whole of NZ receives only 3 million tourist visitors a year.

LikeLike

Auckland sits on 5000skm and includes Manukau, Northshore, Waitakere

LikeLike

But I’m not sure what your point is. Sure there are differences, but I’m not sure what the airport and museum and visitor numbers have to do with land taxes or house prices. And as I’ve noted before geography might mean central Akld land prices might be legitimately higher than those in a flat city of 1.5m, but peripheral properties would reasonably be less expensive.

LikeLike

If you are trying to compare like with like then you would have to look at Auckland in the context of 26,000 skm which means for an apples to apples comparative with Houston we need to take in cities from Kaitaia down to Hamilton for 26,000 skm in area. In that context peripheral properties would be far cheaper. Afterall city boundaries are artificial and trying to compare a city on 5000skm with a city on 26,000skm and wonder why one city is so much cheaper is just nonsense statistics, what is real is the actual area.

LikeLike

yes, I agree local municipality boundaries are artificial, which is why I like the US approach which typically looks at things by metropolitan statistical areas. However, as the super-city Auckland boundaries already reach beyond the effective urban limit, if anything using NZ stats based on municipal boundaries probably makes “urban Auckland” prices look a bit lower than they are (only a bit, since the turnover is mostly where most of the people are).

And recall that Houston has 4 times the population of Auckland – again, if anything, that might be expected to raise Houston prices relative to those in a small city (US or NZ)

LikeLike

4 times the population but 5 times the land area.

LikeLike